Vinoth Jayakumar ретвитнул

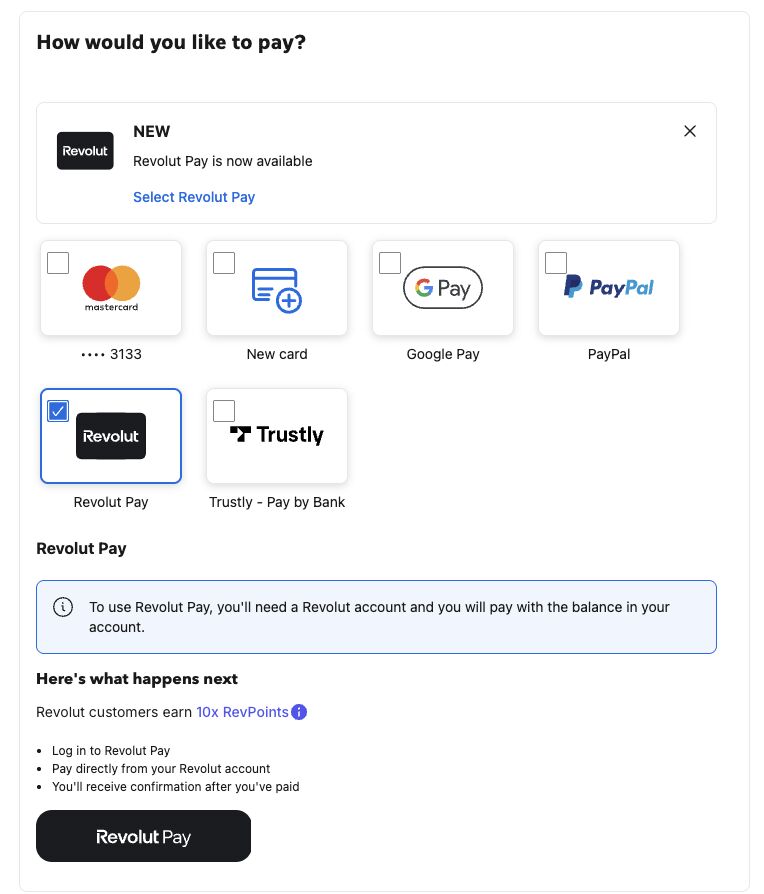

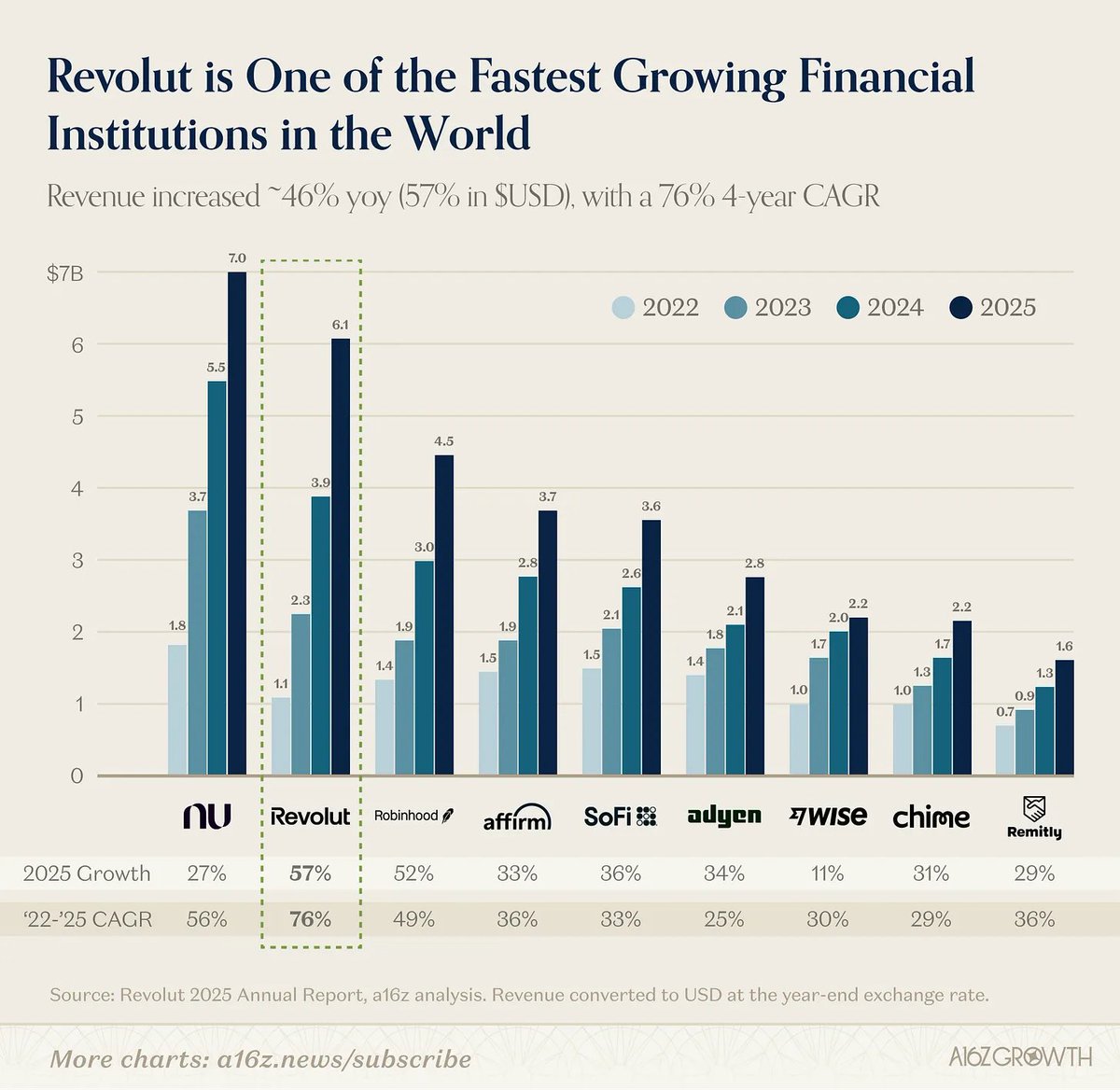

.@Revolut is one of the fastest growing financial institutions in the world

@aleximm and @santiago__rdz on the outlier numbers in Revolut's 2025 Annual Report:

- Revenue grew 46% to £4.5 billion

- Profit before tax grew 57% to £1.7 billion, realizing a 38% margin

- Retail customers grew 30%, having added 16 million in 2025 alone

- 11 different product lines exceeded £100 million revenue

- Return on equity (ROE) is a category-breaking 35% (despite over capitalization)

Read more: a16z.news/p/the-algorith…

Alex Immerman@aleximm

English