Being Bull ♉ รีทวีตแล้ว

25 High-Potential SME Stocks With Long-Term Growth to Study & Research 🔥🔥🔥

FlySBS Aviation

Viviana Power

Yash Highvoltage

Oriana Power

Asarfi Hospital

Sathlokhar Synergys

Aimtron Electronics

Alpex Solar

Danish Power

Rajesh Power

Supreme Power

Neetu Yoshi

Exhicon Events Media

Afcom Holdings

Maxvolt Energy

Airfloa Rail

Unihealth Hospitals

L. T. Elevator

Prizor Viztech

Vilas Transcore

Monolithisch

OSEL Devices

OBSC Perfection

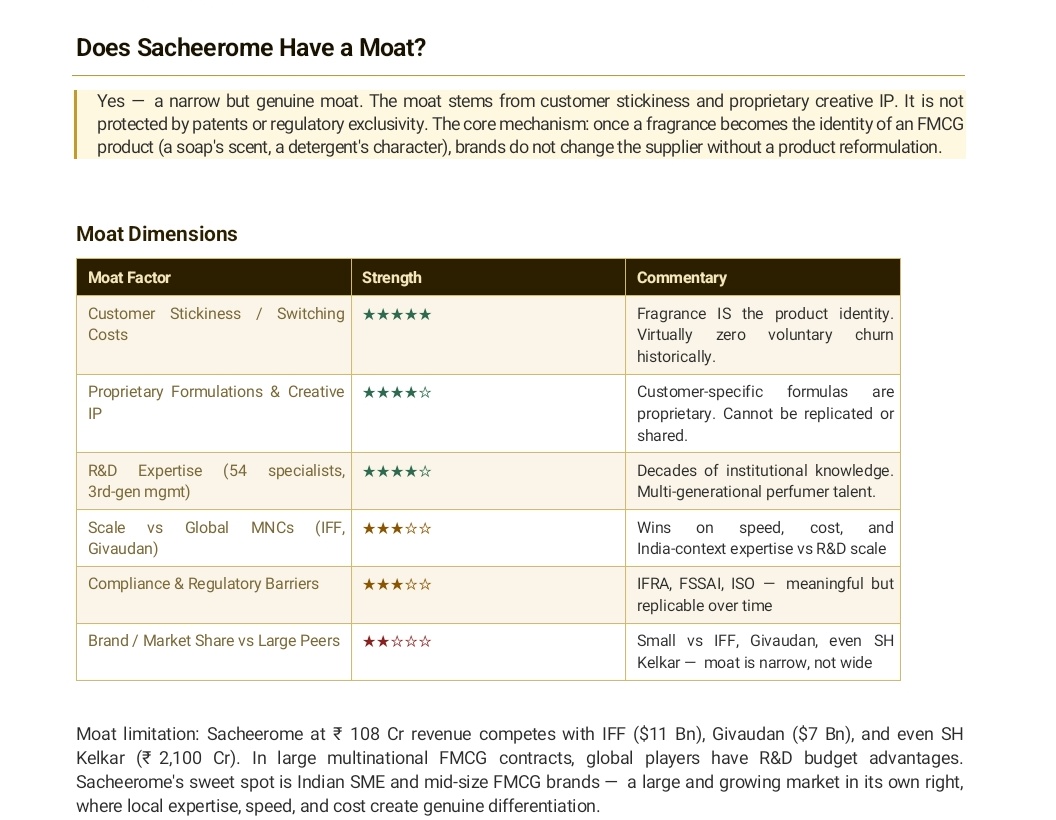

Sacheerome

Long-term valuation will be determined by execution and management quality - if the management delivers on its guidance and the company executes efficiently while operating in a favorable industry environment, these businesses can perform exceptionally well.

Therefore, when the market corrects and stocks are available at attractive valuations, it becomes the ideal time to study, track, and research such companies to gain an early mover advantage for the next bull run.

Disclaimer: This content is for educational and informational purposes only and should not be considered as financial or investment advice. The stocks mentioned are for study and tracking purposes, not recommendations to buy or sell.

English