@anne_tyler77178 Especially when the nasdaq is appreciating at a pace that will have it doubling every 3 months...for me at least!

English

George Coyle

4.6K posts

@gfc4

Co-author with Jack Schwager of forthcoming Market Wizards book due out 6/9/26. Pre order at link below. Post about trading, markets, etc.

Learned an important lesson from my sales team today: investors care less about portfolio volatility or max drawdown and more about time spent underwater. I've spent a lot of time making the case that return stacking can reduce portfolio downside and add diversification benefits on top of a 60/40. Both true. But I think I've been missing the mark. The variable that really matters is less about the absolute reduction in the peak to trough loss, and more about how quickly you get back to breakeven after a major bear market. The images show a return stacked portfolio comprised of the following (𝗯𝘁𝘄, 𝘆𝗼𝘂 𝗰𝗮𝗻 𝗽𝗹𝗮𝘆 𝘄𝗶𝘁𝗵 𝘁𝗵𝗲𝘀𝗲 𝘆𝗼𝘂𝗿𝘀𝗲𝗹𝗳 𝘄𝗶𝘁𝗵 𝗼𝘂𝗿 𝗮𝗻𝗮𝗹𝘆𝘇𝗲𝗿 𝗵𝗲𝗿𝗲 𝗵𝘁𝘁𝗽𝘀://𝘄𝘄𝘄.𝗿𝗲𝘁𝘂𝗿𝗻𝘀𝘁𝗮𝗰𝗸𝗲𝗱.𝗰𝗼𝗺/𝗽𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼-𝘃𝗶𝘀𝘂𝗮𝗹𝗶𝘇𝗲𝗿-𝘄𝗶𝗱𝗴𝗲𝘁/) : → 60% equities → 40% bonds → 5% gold → 5% merger arbitrage → 5% managed futures trend → 5% managed futures carry The stacked 60/40/20 portfolio compared to a plain 60/40 had the following outcomes: • the GFC drawdown -32.5% vs-30.8%. Nice, but not life changing. • The bigger story: the dot-com recovery for 60/40 took 49 months • The stacked version took 39 months • Nearly a year less time to start compounding again! A year of clients not capitulating. A year of advisors not getting fired. Less time underwater may be the most underrated benefit of stacking truly uncorrelated diversifiers on top of your portfolio. 🥞

@Investor_NICK_ why only 28.5T, space is infinite

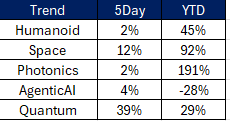

Trading HEAT? I’d suggest you study the HEAT from the past👇