@fxckpgmol Bitch why would Mavropanos be invited to Man City’s PL winners parade?

English

Neel KashCarry’s Biggest Fan 💯🖨💵

20.9K posts

@DitheringWenger

Oil, ex Arsenal fan & E&Ps. Great looking and smart, a true Stable Genius! Tweets are my own and should never be taken seriously, like never ever.. Master Troll

VP Vance left Friday for Pakistan: Axios

After considering all events in the region, and attitude towards negotiations past 48h, it appears that ceasefire is not taken seriously and that military operation is likely being prepared to take control of Hormuz (islands, and possibly Kharg), likely very soon.

*MICHAEL BURRY SAYS HE ADDED TO NVIDIA PUT CONTRACTS

Two of the measures mutually agreed upon between the parties have yet to be implemented: a ceasefire in Lebanon and the release of Iran’s blocked assets prior to the commencement of negotiations. These two matters must be fulfilled before negotiations begin.

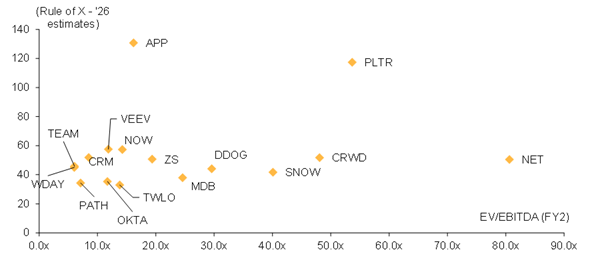

Just got off a call with a sell-side analyst that recently picked up coverage on $APP... he has a buy rating with $700+ price target He said channel checks remain positive with some companies increasing ad spend from low single digits a year ago to high single digits in Q1... he said it's the fastest he's ever seen ad spenders ramp up on a single platform although that includes gaming and non-gaming (ie ecommerce). He's looking for 50% revenue growth in CY2026 but says his numbers might be too low because $APP still hasn't launched their ecommerce product out of beta (should be GA by end of Q2)... which means they only have 7k ecommerce customers versus 3M shopify stores... sounds like ad spenders are very excited for the new GenAI products because its helping them create better targeted ads in less time so they can test and iterate faster than ever before which should lead to better CTR, lower CAC and higher ROAS. $APP now trading at 20x NTM GAAP-EPS which is insane for a company growing GAAP-EPS at a 40% CAGR for the next 2-3 years $APP down -50% from December highs makes no sense to me because the ecommerce TAM is massive and they've barely scratched the surface. It doesn't help that $APP is a top 7 holding in $IGV which is down -35% in the past 5 months... $APP has a beta of 2.5x which also explains some of the extra downside pain... I also think investors are worried that OpenAI, Claude, Gemini and others will absorb some of the ad dollars which might be true or it's possible those platforms partner with $APP NFA. DYOR. *I own $APP personally and so does @FirstWaveFund