Alex Gregory

10.3K posts

Alex Gregory

@DjAlexGregory

Snapchat - DjAlexGregory Instagram - @DjAlexGregory

West Palm Beach เข้าร่วม Eylül 2010

685 กำลังติดตาม887 ผู้ติดตาม

Shift4's $FOUR Warning Signs

$FOUR's Q4 earnings were a mixed bag, to be generous. In reality, there were several red flags that warrant greater scrutiny. Yes, shares are exceedingly cheap, and I am STILL long, but if anything is certain in payments it’s that valuation alone is not a reason for a stock to move higher.

Appreciable slowing of organic revenue growth. The biggie. After increasing 26% in 2024, $FOUR's organic revenue growth is expected to slow to 10% in 2026, inclusive of Global Blue. While low double-digit organic revenue growth is good, especially for a company trading at $FOUR's valuation, the trend is not our friend. More importantly, the slowdown adds validity to a key bear argument for $FOUR that acquisitions fuel an unsustainable burst of ‘organic’ growth, requiring continual M&A to sustain attractive ‘organic’ growth.

2026 guidance does not appear conservative, calling into question a return to beat-and-raise cadence. Even before the Iranian conflict, which may eat into discretionary spending and slow global travel in certain corridors ( $FOUR called out the Middle East and Saudi Arabia as increasingly important strategic markets), it does not appear $FOUR was being overly conservative by assuming recent SSS trends continue through 2026, calling into question a return to a beat-and-raise cadence.

Falling blended spreads in Q4. On a year-over-year basis, $FOUR's blended spreads fell 3-bps in Q4, and probably closer to 4-bps excluding Global Blue. While I’m willing to give $FOUR the benefit of the doubt, if it was indeed a mix issue, it implies meaningful slowing in $FOUR's SMB volume, calling into question the quality of the merchant base and how it would hold up in a more significant economic downturn.

The lack of a clear handle on how FX and geopolitics will impact Global Blue. While I don’t blame $FOUR for things that are clearly outside of their control (FX movements and geopolitical tension), I do believe $FOUR was overly optimistic about the underlying growth potential of Global Blue. As I noted back in October, Global Blue’s revenue grew only at a 4% compound annual rate from 2019 to 2025 (fiscal year ending March), falling to about 2% after excluding acquisitions that created the Post-Purchase Solutions segment in 2020 and 2021.

Shrinking backlog. At the end of 2025, $FOUR's volume backlog was $32 billion, representing only 15% of 2025’s E2E volume. It was also down from more than $35 billion at the end of Q1, Q2 and Q3. While I’m in no way dismissing the opportunity from the cross-sell funnel, recent backlog performance suggests this volume may be more adjacent than captive, requiring more effort by $FOUR to convert it to actual end-to-end volume.

Adjusted free cash flow flat in 2026. After saying it was on pace to exceed its $1B FCF exit rate target in 2027, $FOUR guided to just $500M of FCF in 2026, flat with 2025. Even if I assume FCF grows by one-third in 2027, which may be aggressive, $665 million is a far cry from a $1 billion annualized exit rate. $FOUR now prefers to look at this metric on a per-share basis given its preference for buybacks over debt paydown. Fair, but if I assume $FOUR buys back the entire $1B authorization, the forfeited interest expense savings would only be about $50 million ($1 billion at 7% and a 25% tax rate), making the $720 million pro-forma FCF number still notably shy of the $1 billion target.

Changing and inconsistent disclosure. Underpinning most of my concerns and the red flags I’ve outlined above is $FOUR's changing and inconsistent disclosure. Changing and inconsistent disclosure strikes at the heart of management’s credibility, a precious resource for companies.

English

Added $SGOV as a way to generate some revenue in order to offset some fees.

English

Now that I am sharing the amounts for this specific account I should plan something for when it hits 2m

Any ideas?

Lasse@lasse108

You gotta miss the 40’s

English

@PurpleDrink_LLC The fart coin all in environment you’ve been talking about ?!

English

The environment I’ve waited MONTHS for can be shaping up here

English

My account is about to hit ATHs since I am in LEAPs since upper 20s/low 30s. $lqda

English

@jakebrowatzke Idk any broker that gives more portfolio margin than IBKR

English

I am transferring my portfolio out of Interactive Brokers after 3 great years on the platform and wanted to share my performance history for the record.

Despite being in a -80% TYD drawdown currently I've had a 584% returns from 2023 to 2026, for an annualized return of 88.31%.

I originally left M1 for IBKR during a huge drawdown to get access to more margin. Now I'm leaving IBKR during a huge drawdown for the same reason.

English

I told you private equity would want in

x.com/FirstSquawk/st…

First Squawk@FirstSquawk

DONALD TRUMP SAYS MAY BE JOINT US-IRAN VENTURE FOR HORMUZ TOLLS: ABC NEWS

English

Could this be the biggest Taco Tuesday of all time?

English

@tembelvitesi We top ticked that little squeeze when we were high fiving each other.

English

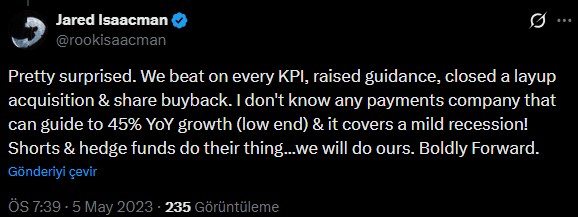

today i added Jan'28 $FOUR leaps with 60c, 70c, 75c.

Today we bottomed at $40.25.

This price does not make sense and has nothing to do with fundamentals. I will be adding to my position as long as it says around here.

But for the fellow $FOUR holders who has doubt or feeling a bit nervous, i start Jared Tweets.

As i have said, this price movement is not fundamentals driven and they have done this before as Jared said back then.

"Shorts & hedge funds do their thing... we will do ours."

English

This is why citirni is the king of substack. I’m hiring a bulltards analyst to fly to Saudi Arabia with a jet ski ready to hit the strait for intel

Hunterbrook@hntrbrkmedia

Exclusive from @citrini x @hntrbrkmedia: A fishing vessel is ablaze in the Persian Gulf just off the Strait of Hormuz.

English

@mvn1cgat0 Raised on rock and metal, I wanted to put more in but had to make it predominantly house.

I do have a full rock playlist though

English

@jbulltard1 Usually when they flag my trades they say “ some pussy “ so it must be nice being called a whale.

English

I like reading the crappy options services posting about an $INTC "whale" buying 4000 of the $60 calls in November. No dipshits, it was me, and they're part of a trade I put on with puts sold lower for a credit rolling down my 43 short puts to 38 in December. Carry on plebes

English

Cool video but that fucking flip phone is insane 😂

reyama tucci (iCarly)@toomuchtosee__

AVB PULLED UP TO GO B2B W SUMMIT

English

The short interest on $four is still very high at 60% as of half an hour ago. ANY good news on war front and this will continue up parabolic. Still cheap and zero reason to exit.

English