ทวีตที่ปักหมุด

tranquille

1.6K posts

tranquille รีทวีตแล้ว

@aleabitoreddit @Sofigoodboy I owe all Protean funds and I’m really happy with them, and Richard Bråse isn’t stupid, but if any of his funds short $SIVE I’m selling all of my assets in the funds

English

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

看来大多数人都是选择不借,我个人也是会选择不借

理由很简单,股票上涨带来的收益会比借 $sive 来的多得多

有可能空军就差你这一股 扭转局势😏

mark@cherryPayment

其实我会收到ib的offer,说要借 $sive的股票 我个人是不会借的,借了只赚那么几千利息,但我不借的话,迎接我的将会是他们平仓止损, $sive 股价3-4x的涨幅 😏😏 支持你的选择!

中文

tranquille รีทวีตแล้ว

今天来看看他们的最新持仓变化,我真心觉得有一家机构对待 $sive的态度就和普通散户一样,不断的试仓,不断的止损,那么现在开始吧:

1. 我们首先谈论的还是 Two sigma,我们会发现通过昨天的下跌,他们小幅度回补了仓位从6月3号的 2.18% 补到了 2.20%,这意味着他们的数据模型认为110 SEK价位是阶段性高点,触发了做空信号,同时这也属于属于对冲再平衡,维持相对稳定的风险敞口。

2. Voleon 继续减仓,和我们上次谈论的一样,他们正在慢慢的减仓从而换取尽可能少的亏损,他们从2.02%进一步降至1.95%,继续有序撤退,减幅0.07%,比上一轮(-0.25%)明显放缓。说明从侧面说明了可用的流动性越来越紧,每天能平仓的量越来越少。

这和我们之前谈论的一样,他们不可能直接全部退出,全部退出无异于用流动性砸死自己。

3. 我们的老朋友三进三出的 Qube!这是非常戏剧性的变化。Qube从 <0.5% 重新加仓至0.56%,这已经是他们第三次开仓了。

我们从时间线就能知道他们的想法:

他们的第一次止损0.80% → <0.5%

这是第二次开仓 <0.5% → 0.79%

第二次又止损0.79% → <0.5%

现在是第三次开仓!<0.5% → 0.56%

从他这个加仓逻辑就能知道所谓的做空机构并没有什么内幕消息,也不可能会有,因为他们在110 SEK历史新高附近再次入场做空,这说明他们的量化模型在极端高波动+RSI超买环境下,会机械性地反复触发信号,完全无视前两次亏损的”历史教训”。这正是量化基金的特性没有情绪记忆,只有信号。

我认为Voleon会持续减仓知道没有,而Qube这次开仓价格比较好,所以还是盈利状态,Two sigma今天过后估计也是加仓状态。

这或许是他们借到了股票,也可能是空军新闻有了效果,还可能是因为大盘的拖累。

但目前来看他们是做好了持久战的准备。

做出自己判断!

mark@cherryPayment

今天继续跟进他们的持仓变化,和我们昨天谈论的几乎一样,也就是说量化基金通常对单一小盘股空头头寸有内部规定,一般不超过基金净资产的0.05%——0.1% aum 1. 首先two sigma 从昨天的2.45%下降到 2.18%。减仓部分是0. 27%,所带来的已实现亏损为(97.75 - 31.5) × 863,874 ÷ 9.32 = 613万美元。 现在所有的浮亏还是在4951万美金 2. Voleon 也继续减仓从2.27% 下降到2.02%,减少了0.25%,其带来的实际亏损为537万美金。 现在他的浮亏为4330万美金。 3. 我们的老朋友 Qube又止损离场了,这一次净亏损约在200-400万美金之间,我认为他可能是觉得股票涨太多,手痒想开仓。Qube两进两出,说明他们内部对这个标的存在分歧,也说明量化模型在高波动环境下会反复触发信号。 从这三家的操作我们可以判断出机构不是神,他们也有判断失误的时候。 另外我想你们会有疑惑:为什么他们不直接止损离场,那么现在的情况是市场没有那么多股票能让他们进行平仓,他们现在只能一点点的减仓来拉低自己的仓位,如果他们一下子进行全部平仓,那么股价突破200sek 也是有可能的。 那么从减仓来看,我们能知道的是: 1. 他们平仓了2783596股 $sive, 所带来的买盘为1219万美金。 2.如果这1219万美金能够带动69%的上涨,那么剩下的1344万股的平仓会带来怎样的涨幅呢? 那么我是不是可以这样猜想:278万股的买盘推动了+60%,剩余1,344万股是前者的4.8倍,流动性不是线性的而是指数级的 我认为上涨还未结束,拿好自己的筹码等待起飞!

中文

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

@Sofigoodboy A 15% dilution $SIVE is just standard operating procedure for scaling capacity at this stage—the shorts are overplaying their hand if they think a routine AGM vote justifies their thesis.

x.com/Dmytro_Lebid/s…

Dmytro Lebid@Dmytro_Lebid

My latest analysis on Seeking Alpha is now live! This time, I’m breaking down Sivers Semiconductors ( $SIVE ), a company that has recently completely flipped the script on the CPO supercycle. Achieving operational breakeven, coupled with the anticipated direct listing on the NASDAQ US, could revalue the company with the potential for share price appreciation of up to 100%. The thesis behind this deep dive started brewing after tracking some phenomenal research by @aleabitoreddit and working Seeking Alpha colleague @DanilSer33. Their insights into the AI data center infrastructure and qualification cycles effectively validated what the numbers are now showing. SIVE’s latest explosion in their opportunity pipeline isn't just a random earnings spike; it's a structural inflection point. We are moving away from the R&D narrative straight into mass volume production for photonics and lasers. While backward-looking metrics might confuse legacy investors, the forward-looking compounding growth here is what truly matters. Is the market still mispricing this crucial piece of the AI infrastructure stack, or is the exponential run already baked in? I’ve mapped out the full fundamental breakdown, revenue ramp projections, and potential margin of safety. The full breakdown is waiting for your view below this post in the pinned comment👇

English

tranquille รีทวีตแล้ว

Jag har senaste tiden märkt att fler och fler ställer frågor och vill prata om Sivers, men många inte riktigt vet eller förstår vilken teknik Sivers ($SIVE) faktiskt arbetar med. Det är fullt förståeligt för en vanlig lekman – jag är själv civilingenjör inom datateknik men fick även jag lägga en del tid på att sätta mig in i området när jag 2021 upptäckte bolaget.

Det som frustrerar mig är att stora delar av svensk finansmedia verkar välja den enkla vägen. Istället för att försöka förstå tekniken, marknaden och varför globala teknikjättar investerar miljardbelopp i området, fokuserar man på att vilseleda sina läsare med sociala medieprofiler, kursrusningar, enskilda insiderförsäljningar eller att avfärda allt som en “memeaktie”.

Problemet är att verkligheten är betydligt mer komplex än så.

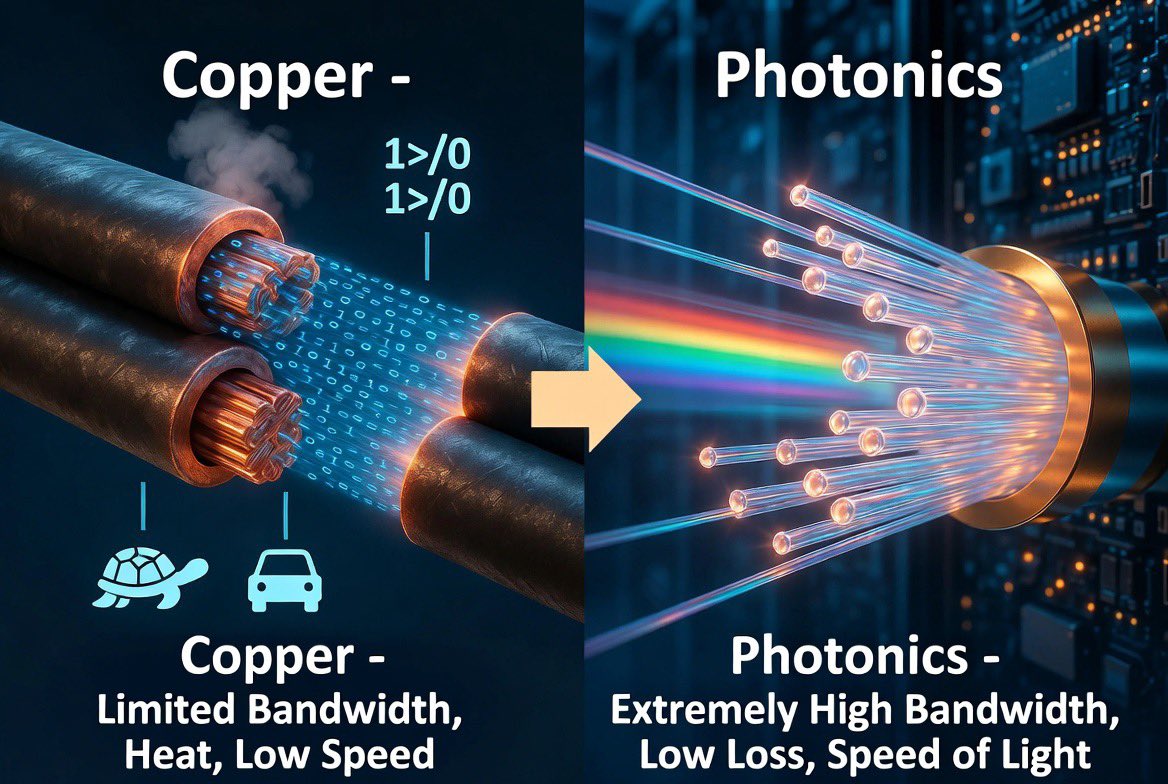

Sivers verkar bland annat inom ett område som många aldrig hört talas om, men som kommer vara avgörande för framtidens AI, datacenter och kommunikationsnät. För att förklara det enkelt för min familj och vänner brukar jag jämföra det med övergången från internet via telefonjacket (koppar) till fiber (ljus/photonics). Skillnaden är att Sivers utvecklar teknik som hjälper till att flytta enorma mängder data på extremt små ytor och i hastigheter som morgondagens AI-infrastruktur kräver.

Detta är inte en debatt om vilken teknik som ska vinna. Inom datakommunikation håller koppar på att nå sina fysiska begränsningar. Behovet av att använda ljus för att transportera data är inte en trend, det är en konsekvens av fysikens lagar.

Därför ser vi idag Nvidia, AMD, Intel, Microsoft, Google och andra investera enorma summor i denna utveckling.

Sivers kommer inte att få monopol på marknaden. De är fortfarande en liten aktör. Men de har lyckats ta plats vid samma bord som några av världens största teknikbolag inom en marknad som fortfarande knappt har börjat växa.

Därför lägger jag mindre vikt vid om aktien gått +100 %, +500 % eller +2 000 %. Det intressanta är marknaden bolaget adresserar och hur stor del av den Sivers mäktar med att leverera till och lyfter min blick mot 2028-2030.

Detta är inte en köp- eller säljrekommendation. Det är bara ett försök att lyfta diskussionen från dramatiska rubriker, memes och förenklingar – till den teknik och marknad som faktiskt driver utvecklingen och ge alla en rättvis chans att förstå branschen. $SIVE

Svenska

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

标普九连阳终结,多个信号同时出现,这次回调值得认真对待

今天标普500收盘下跌56点,跌幅0.74%,终结了九连阳。

本周周线已经变成阴线。更值得注意的是今天的K线形态——高开低走阴线,全天没有任何下影线支撑,说明从开盘到收盘一直在卖,没有抄底盘进场。这是近期以来最难看的一根K线。

今天大跌的原因不止一个

有人问我是不是因为日本央行鹰派导致的。

是其中一个原因,但不是全部。今天是几件事同时发生:

第一,日本央行植田和男发表鹰派讲话,明确表示将继续推进加息,并预计通胀将在2026年显著加速。

第二,美元/日元跌破160警戒线,Yen Carry Trade的风险再次被激活。逻辑很简单——借日元买美股的资金,一旦日元升值,就需要被迫平仓还钱,美股跟着被砸。上次这个逻辑触发是去年8月,日经单日暴跌12%。

第三,ADP小非农数据超预期,5月新增就业12.2万人,创16个月最强表现。就业市场强劲,意味着美联储降息窗口被无限期推迟,利率higher for longer重新压制估值。

第四,美伊双方昨夜再次互相袭击,伊朗导弹击中科威特机场,美军对伊朗格什姆岛发动反击。霍尔木兹海峡封锁可能持续到9月劳动节,油价继续上行,通胀压力重新积聚。

这几件事撞在一起,大跌是有逻辑的。

今天这波跌的性质——多头踩踏,不是空头进攻

这个区别很重要。

从量价剖面来看,今天是开盘直接向下清算然后横盘。这种形态说明:在高位被套的追多资金因为跌破成本价被迫割肉离场,是多头踩踏引起的清算,不是新的主力空头主动发动进攻。

如果是新空头主动进攻,后续下跌动能会更持久。如果只是高位多头的被动清算,跌到关键支撑就会止住。

目前来看更像后者。

技术面:到处都是假突破

今天最值得警惕的信号是假突破的普遍性。

工业板块:Caterpillar在前期高点直接被压下来,Cummins日内冲高后留下极长上影线,Honeywell被空头碾压,GE在头顶套牢盘压制下毫无突破能力。

七大科技板块:特斯拉和亚马逊过去三天把好看的反转信号逆转成了双顶压制。微软,上周五突破,周一跳空高开,今天直接假突破回落,200日均线没守不住,430美元的突破点彻底失败,现在看是假跌破430还是真跌破了。英伟达:218.35美元下方已经形成更低的高点,下方等高双底如果被击穿,直接看50日均线206。

Spacex上市前估计会持续对七大科技吸血,是坏事也是好事,会创造一些更好的买入七大科技的机会。

SPY关键点位

今天SPY正式跌破了前一日的日线低点,技术性回调正式启动。

1小时图上正在构筑一个潜在的头肩顶形态,颈线在754美元。跌破754,第一目标751.75,第二目标748。

748是本次回调最关键的入场位置,有三条线同时汇聚:斐波那契38.2%回撤位、锚定VWAP、以及正在向上爬的20日均线。三线共振意味着这里的支撑非常厚实。

如果价格能在748附近企稳,是非常好的加仓机会。即使短暂下穿,下方还有更多支撑托底。

守住748,回调结束逻辑成立。跌破这里且没有迅速收回,等更低的位置再说。

纳指比标普抗跌,内存股是关键

今天标普跌了0.74%,但纳指只跌了0.29%,盘中还一度创了历史新高,尾盘收出了一根锤子线。

原因很直接:英伟达今天跌了3.14%,但AMD涨了1.64%,闪迪等内存股下午走出了创历史新高行情。内存板块的强势直接托住了半导体指数和纳指。

纳指没有跌破前一日低点,这是和标普最大的区别。纳指可能会先于标普反弹。

IWM小盘股结构

IWM目前仍然处于一个大的横盘牛旗结构中。

小盘股的风格一向恶劣,在最终向上突破之前,总喜欢先往下洗盘,把牛旗下轨砸穿,回补下方缺口285(也是日线ema 20的位置),然后主力才会反手拉升。目前IWM的走法完全符合这个逻辑。

小盘股对利率非常敏感,今天ADP超预期加上美债收益率上行,是IWM今天跌幅最大的直接原因。等利率压力边际减弱,IWM的反弹力度可能比大盘更强。

如果大盘在748.75附近企稳,IWM的牛旗结构依然完好,后续补涨空间是存在的。

私信贷市场出现新裂缝

Cliffwater称旗下私信贷基金面临超过17%的赎回请求,规模比Q1更大。黑石、KKR、Blue Owl、阿波罗全球管理今天集体大跌。

软件股占私信贷基金投资组合约20%。这个压力会双向传导——软件跌影响私信贷,私信贷赎回压力也会反过来砸软件股。这是一个负反馈循环,目前还没有被市场充分定价。

SpaceX IPO定价135美元,6月12日上市

发行5.556亿股,融资规模750亿,估值约1.75万亿,成为美股第九大市值公司。这是有史以来最大的IPO。

流动性虹吸效应下周开始会越来越明显。市场资金已经在从比特币、太空概念股中撤退,但不是说这两个板块就一路跌,在中间也会有超跌反弹,反弹完后再派发,预备着等SpaceX上市后抢购。这个抽血效应接下来一周会加速。

期权结构和市场情绪的几个信号

今天11大板块里能源领涨,这个信号值得记录。历史规律显示,当能源板块持续跑赢标普时,通常对大盘的绝对价格走势不是好兆头。这是典型的防御性资金轮动,说明部分机构在主动降低风险敞口。

有一个细节值得注意:今天大盘跌了将近1%,VIX却几乎没有动,只是小幅上升。个股风声鹤唳,但大盘指数整体维持得相当好。这说明市场目前的恐慌程度并不高,没有出现系统性的抛盘。

期权层面有几个指标在同时发出信号。个股期权的Put/Call Ratio目前处于极低水平,历史上每次这个比率掉头向上,往往伴随着大盘进入横盘或回调。

同时成长股对价值股的相对强弱指标开始向下穿透零轴,意味着资金开始从成长股流向价值股,历史上对应市场进入震荡修整期。

这些信号单独看都不是大问题,但当它们同时堆积在一起,说明市场需要时间消化。不是崩盘的信号,是需要谨慎的信号。

SPY目前已经跌破5日均线。好消息是5日均线依然保持向上的斜率,所以目前只是一个警示,不是趋势破坏。如果能迅速站回均线上方,多头结构完好。如果继续下行,日线隐含波动下限在750到748美元,跌破这里会进一步向周线隐含波动下限746.35到744区域测试。

盘后期指已经跌到了日线隐含波动下限附近。明天白天的常规交易时段能否守住748附近,是关键的观察点。

最重要的一个数字:Gamma翻转线在7480

这是目前最需要盯住的点位。

我们过去一段时间一直处于正Gamma环境,这个环境下做市商充当缓冲器,价格跌了买入托底,涨了卖出压制,波动率被天然压制。这也是为什么大盘在高位可以这么平静。

一旦跌破7480进入负Gamma区域,机制完全反转——做市商被迫越跌越卖,越涨越买,顺势放大波动而不是抑制波动。历史上每次切入负Gamma区间,市场都会迎来波动率的显著飙升。

所以748到750这个区间的重要性,不只是斐波那契和VWAP的共振,更是正负Gamma的分界线。守住这里,波动率继续被压制,市场有序消化。跌破这里,游戏规则改变,需要切换到适合高波动率环境的策略,不能继续用正常环境下的突破做多逻辑。

未来一两周的节点

6月18日OpEx之前,任何下跌大概率都会被磁吸回7600附近。做市商在7600堆积的大量Gamma敞口,正Gamma环境下他们会在价格下跌时买入托底,这个机制在OpEx结算之前不会消失。

但六月中旬有几件事同时撞在一起:6月10日CPI数据、6月12日SpaceX上市、6月17日新美联储主席沃实首次面对记者发言、6月18日FOMC加OpEx。

warsh在外界看来是鹰派官员,这是他上台后第一次公开讲话,市场极度敏感。点阵图可能整体上调一格,体现一次加息预期。这几件事集中在六月中旬,是整个六月风险最高的时间窗口。

调整窗口大概率在6月底到七月初,幅度预计5-10%,这不是大崩盘,是高位正常的获利了结加板块轮动。调整完之后方向还是向上,七月中旬之后继续看多,Labor Day前有机会刷新历史新高。

一个值得记住的历史数据

有一个历史规律值得单独说一下。

从历史数据来看,当标普出现这种级别的9周连续大涨时,后续的远期回报其实非常出色。3个月后的平均回报率达到9.2%,是其他所有时期平均值2.6%的三倍多。6个月后的平均回报率跳升至12%,而普通时期只有5%。

也就是说,历史上每次出现这种强势连涨之后,市场往往会继续走高,不是就此见顶。

这不意味着短期不会回调。但它说明了一件事中长期趋势没有改变,现在发生的只是正常的高位获利了结,不是趋势反转。

短期的noise是洗盘,不是上涨的终点。

怎么应对

不要在明天开盘恐慌卖出。今天的跌是多头清算不是空头主攻,性质不一样。

等748.75到750这个区间。如果价格在这里企稳出现买入信号,这是本次回调最好的入场机会。如果跌破748.75且没有迅速收回,那就等更低的位置比如746和744。这个时候可以用金字塔加仓法,假设明天开盘752,那就752 10%,748 20%,746 30%,744 40%,底线是在743这个缺口这里也是日线ema 20的位置。我不觉得在6月18号opex周之前会跌破因为做市商在7600堆积的大量Gamma敞口,正Gamma环境下他们会在价格下跌时买入托底,这个机制在OpEx结算之前不会消失。大概率这周再调整两天,下周开始可以在高位买些put (我计划10%的仓位)或减仓持有现金来对冲风险。

六月中旬这个回调窗口我之前就说过了,现在只是在验证时间表。

中文

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

作为一个拥有上万粉丝的博主,发布这样的内容之前是否做过基本核实?

1.首先Harish,你对于他的职位你只提到了他是runs the Wireless segment,但你却丝毫不提及他是 MixComm 的联合创始人兼前CTO,MixComm于2022年2月被Sivers收购后,他以MD身份加入Sivers Wireless管理层。

所以当你只提起他runs the wireless segment的时候会给读者误导:”高管抛售=看空公司”的错误印象。

当我们知道他职位的前因后果后,你就会明白他持有的股票来自2022年收购时的股权兑换,不是普通员工薪酬期权,这是创始人套现,完全正常的退出行为,不是”看空公司抛售”。

2. 你金额也多算了3%,这也说明你没再三核实。

3. 另外Disposal并不能等同于主动抛售

瑞典监管披露中”Disposal”包含多种情况,收购方创始人在锁定期结束后的计划性减持是最常见的情形之一。

并且如果你真的认真去做了研究,你会发现MixComm 收购是发生在2022年,而锁定期通常是2-3年,2026年5月正好是锁定期届满窗口,所以完全就是正常锁定期到了。

4. 并且他卖出的价格是71.3633 sek,而空头们的建仓均价是19-35 SEK。

那么问题来了 谁才是真正看空公司的人呢?

如果创始人在71 SEK套现离场,空头在20 SEK建仓做空,四年后创始人笑着走了,空头还被困在里面。

NINGI RESEARCH@NingiResearch

$SIVE exec who runs the Wireless segment (69% of revenue) casually dumped 1.4M shares for SEK 100M ($10.4M) on the same day $SIVEF released earnings. Let's see how the pumpers & the company spin this one. Probably: "Wireless doesn't matter, Photonics is the growth story." LOL

中文

tranquille รีทวีตแล้ว

$SIVE - FOUNDRY-STACK CAPACITY OPTION IN AI OPTICS REPORT SENT TO CLIENTS AND SUBSTACK.

We note $SIVE as a designed‑in light‑source layer inside a tier‑one SiPh/CPO foundry stack.

$SIVE is not just a standalone InP fab: the GlobalFoundries SCALE collaboration, plus Ayar, O‑Net/Enablence, POET, Jabil 1.6T and a USD ~799M pipeline, together create an option on GF‑scale AI‑optics volume without $SIVE carrying foundry capex,

Our capacity‑option model and EV/Sales cross‑check both triangulate to a platform value around SEK 150 versus SEK 86 spot.

Access full report at the bottom of substack article below.

seqhresearch.com/p/sivers-semic…

English

tranquille รีทวีตแล้ว

tranquille รีทวีตแล้ว

Sorry Markos, but you seem to connect two facts that may not actually be connected, please review your DD to make sure the conclusion are correct. "Apperently people hate it when you just inform." Are you informing or misinforming?

Please check below and see if you still can claim that you are correct?

Fact #1: Ayar's next-generation optical I/O roadmap is increasingly tied to TSMC COUPE and advanced heterogeneous integration. (true)

Fact #2: Sivers supplies laser technology into Ayar's ecosystem and was publicly described as a strategic partner in Ayar's move toward volume production. (true)

sivers-semiconductors.com/press/sivers-s…

The leap you are making is:

"Ayar moves from GF to TSMC, therefore Sivers InP lasers is no longer used."

But you are wrong, TSMC COUPE is primarily sillcon/PIC/package layer for TeraPHY.

Sivers sits in SuperNova, i.e. the external light source (ELS). They are NOT the same thing.

TeraPHY and SuperNova (remote light source) are separate parts of the stack.

Even Ayar's latest rack-scale AI announcements continue to reference SuperNova as the remote light source powering the architecture. SuperNova has never ever been produced by GF, that has only been the TeraPHY chip.

As far as I know GF nor TSMC makes External light source, that is done by other suppliers.

Hence from my understanding, you are making a false claim.

On the GF SCALE CPO standars OCI platform and Sivers being chosen for reference design for this industry first new hyperscaler standard, has nothing to do with Ayar, this is an new open CPO standard for hyperscalers to use if they want supported by NVIDIA and AMD. Being placed in the GF platform is not a negative, but it is also not a automatic exclusion for use in the SuperNova even if TSMC does the TeraPHY chiplet.

English