ทวีตที่ปักหมุด

Miserable🧈Fly

19K posts

@MiserableFly4

GME squeeze Jan 2021, Reddit is a controlled psyop. Self made Shillionaire! 🛌🛁🚀 $TEDDY 🦋 Not Financial Advice

The most radicalizing videos on the internet are from about 40 years ago when malls were packed

Did You Know: The 28 Pages show that two 9/11 hijackers tied to Saudi intelligence rented a room from an FBI informant in California before the 2001 attacks The Director of the FBI kept this covered up for years His name? Robert Mueller

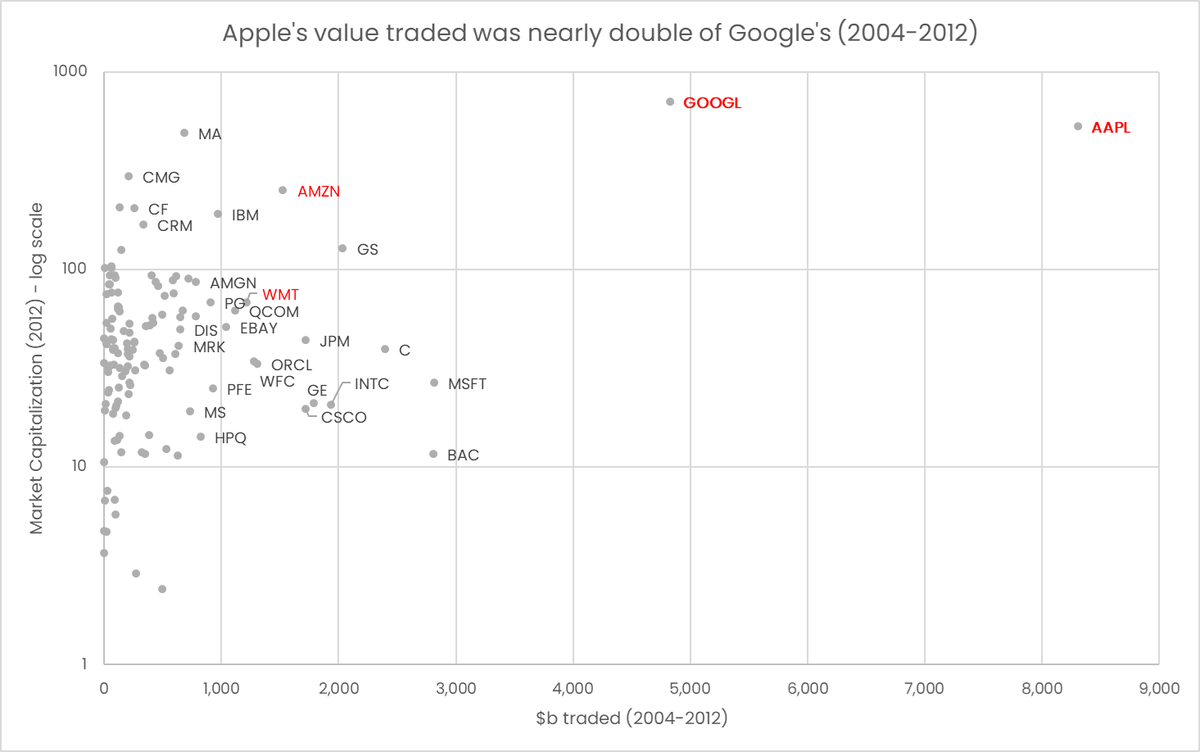

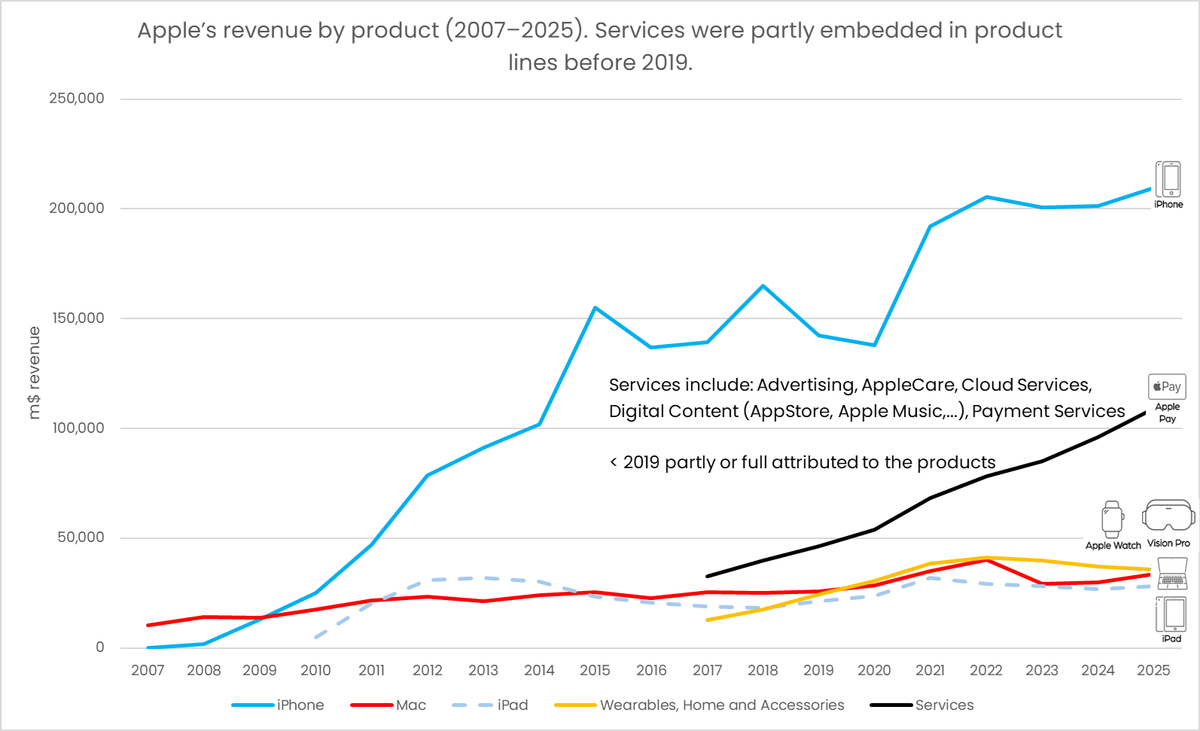

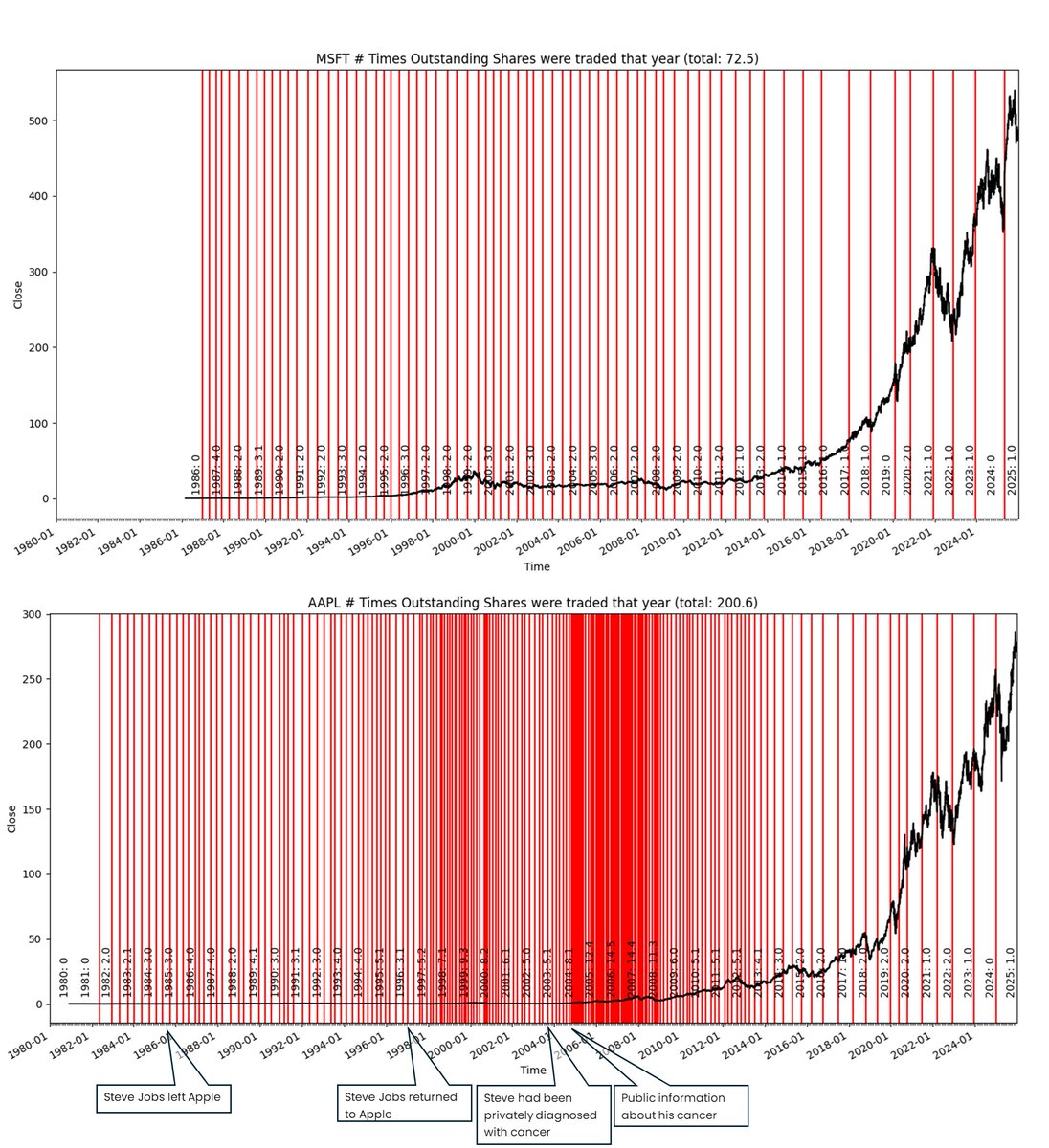

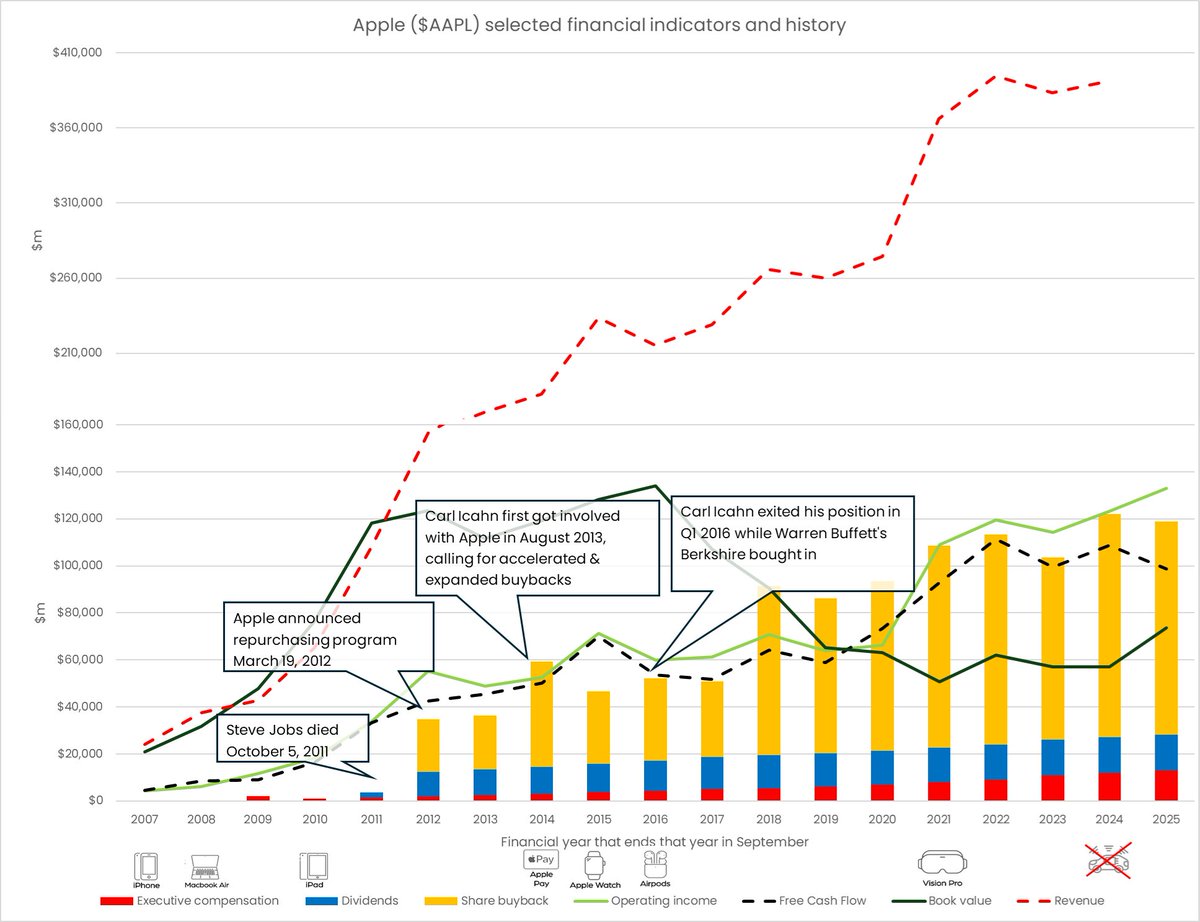

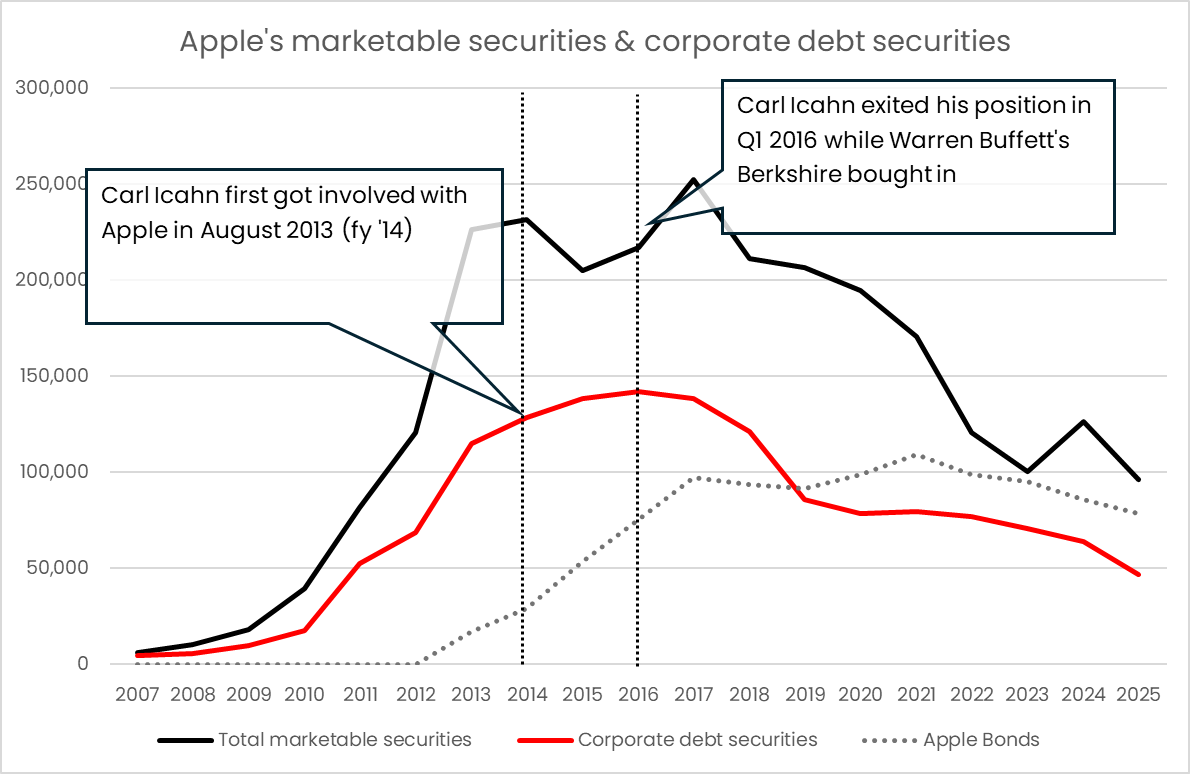

A discussion and deeper dive into Michael Burry's "Foundations: The Big Short Squeeze" from 12/16/25 This is not financial advice; do your own research; I am actually retarded This post is only for a very few. This is for those who want to understand the legends of activist investing like Carl Icahn (@Carl_C_Icahn), Ryan Cohen (@RyanCohen), Michael J. Burry (@michaeljburry) or godlike analysists like Morgen Hatton (@MorgenHatton). For those who are interested in discussing market and accounting mechanics, for putting first principal thinking over mainstream believe and who are willing to work hard (and read through my mess). Further this post will not be as easy to digest as Jake's posts or even charmingly inviting to repost in a britisch slang, nor will I ever charge a penny for it like Burry. The real value comes from applied knowledge. From actual usefulness. TL;DR: We'll propose a model to evaluate morals based on financial metrics and more clearly define overpaid executives, overpaid activists et cetera; we'll counterargue Burry's view on naked shorts, short interest, big sneeze to show the nature of $GME as nuclear bomb rather than table lighter; we'll evaluate every action activists proposed for $GME and its outcome; we'll define a set of actions as bullshit and as thought experiment adjust the company's financials, introducing "operating income bs adjusted"; we'll suggest the application on scale --- Topics --- * Acknowledgement * grouping activist investors and executives * outside perspective (short interest, big sneeze, naked shorts) * inside perspective (activist investors) * inside perspective (operating income bs adjusted) * wrapping up --- Acknowledgement --- I really enjoyed Burry posting about his days with $GME. I love thinking back at the time and I am grateful that he invested. I am also grateful for what Keith Gill did back then. I most probably wouldn't be here without both of them. If it wasn't for those two guys, I probably wouldn't have invested into GameStop, wouldn't have learned about Ryan Cohen, Bill Pulte, Ramez Khan Hussain LongDong Jamali, the team, all you amazing people and I never would have invested this much work (and money) into understanding financial markets, price discovery, dark pools, naked shorting, financial instruments, activist investment, asset displacement by overpaid consultants and overpaid executives. I would have been unaware what really happens to companies right in my neighborhood, at the scale of things, at least to the extend I am now and partly trying to share with you. I would probably not have collected first hand experience watching overpaid consultants and executives retarded work, going unnoticed for so many. There were many along the way I am grateful to have met, but without Burry, without Keith and of curse without Ryan Cohen, this would not have happened. Thank you guys from the bottom of my heart. I also want to thank your wife who has a handsome, charming boyfriend with a well trained body. First we'll take a quick detour into morals and ethics before we discuss Burry's points. --- grouping activist investors and executives --- A way to group activist investors, executives and maybe people in general maybe by their morals, derived by their financial track record. While this will not be a black or white relationship, with the length of the track record observable, we can put someone in a group someone with more or less certainty. I suggest the following three groups: 1. Strong morals: profits of the individual equals relativ to all long-term shareholders (and society) * E.g. Ryan Cohen who doesn't even takes a salary, invested his own money and thus profits %-age wise the same as every other shareholder. * E.g. Elon Musk who's pay package is totally related to company combined with stock performance, he doesn't earn something if shareholders don't but will earn %-wise more than all other shareholders (not in absolut terms though). 2. Average morals: profits of the individual are (far) above all long-term shareholders (and society) * E.g. Activist investors greenmailing a company * E.g. The average CEO of a long-term good or medium performing company 3. No morals: profits of the individual are inversely correlated to losses of shareholders * E.g. Overpaid executives earning a lot of money, directly or indirectly via 3rd party deals, while running the company into the ground, tunneling out assets, tricking financial statements and communicating not in an open and honest way * E.g. Macellum with a track record of at least 6 companies (x.com/beyond_mythos/…) * E.g. Mithaq with a track record of at least 4 companies (x.com/beyond_mythos/…) Adding an ethical layer, for "no morals" this aligns pretty well with Ryan's thoughts that "[i]n general, when an executive gets paid millions of dollars and leaves a company in shambles, they should be forced to return the money" (x.com/ryancohen/stat…). While we could use this at scale and apply measurable criteria, we have to keep in mind that we can only evaluate what we are able to see. Profits sometimes may not come as direct related payment but come as gratitude, like someone giving you free, lifetime, unlimited Mayo-supply in return for a favor. Also true long-term shareholder value and societal impact, like equity on a balance sheet, may over time and with other information change or turn out to be off by a big factor. For better or for worse. Thus a person fitting seemingly into one group, might actually not, if we had full information. However, I'll leave you with some thoughts about criteria and might add to this later. 1. Strong morals: Personal profits ≤ 1-2% of total shareholder returns (TSR) over 5+ years, with compensation fully performance-tied (e.g., no base salary > industry median unless offset by equity grants vesting on long-term goals 2. Average morals: Personal profits 2-5x median shareholder returns, with some alignment (e.g., stock options) but clear extraction via high fixed pay or perks. 3. No Morals: High personal profits while total shareholder return is negative over 3+ years, or evidence of tunneling (e.g., Buybacks at peaks, board cronyism, illogical massive impairments, off-priced M&A or asset buys/sells, massive dilution, accounting tricks). For example, some time back I brought forward thoughts about when a share buyback could be viewed as rather good or bad: x.com/beyond_mythos/… That said, wouldn't it be interesting to estimate the probability of activist investors like Tiger, Hestia, Permit and Burry (Scion) being in one group or the other? --- outside perspective (short interest, big sneeze, naked shorts) --- We'll start with the outside from Burry's post (michaeljburry.substack.com/p/foundations-…), meaning statements about the short interest, the big sneeze and naked shorts. Interestingly, those who followed the journey at least since January 2021 will know how easy it is to disprove most of Burry's claims. Let us look at them one by one: 1. Naked Shorting in GME SI (140%) * Burry's view: Downplays; mostly legal layering (borrowing/relending). Naked not prime factor. States: "no shorts had to be naked for this to happen, and I am sure there were some, but naked short selling was not a prime factor." * Counter arguments: Massive naked shorts via synthetics/counterfeits for price suppression; fits cellar boxing (mechanics: x.com/beyond_mythos/…, $GME volume turnover graph: x.com/beyond_mythos/…). High FTDs/volume suggest naked over layering (statistical overview, sorted by buybacks: x.com/beyond_mythos/…). 2. 2021 Squeeze Cause/Nature: * Burry's view: Legal corner via retail call buying causing gamma squeeze; dealers hedged, layering broke. Not mainly short covering. * Counter arguments: No short covering/closing as seen with point 1. My opinion: price control via dark pools and naked shorts allowed an orchestrated squeeze after the 2021 inauguration of the Biden administration, taking away the buy button to discourage investors and a house hearing which lead to nothing (other than still giving me laughs thinking about that young boy from Bulgaria - the clips having been thoroughly deleted from Reddit - Kudos guys). 3. Post-2021 Short Status (Closed?) Burry's view: Exited pre-squeeze; implies unwound via covering (now GME SI at 16%) and warns of meme risks. * Counter arguments: Not closed; MuckeryMeter: 122%+ unclosed shorts since 2022 (x.com/beyond_mythos/…). SEC report notes unexplained SI drops (same source as MuckeryMeter). The sheer stunning change of the S3 SI (short interest) formular in coincidence with he short interest drop: * "Every short sale creates a "synthetic long" so the traditional float number in the SI % Float calc is wrong. It should include "synthetic longs", therefore there is never any stock with over 100% SI % Float which makes sense as you can't get 5 quarts of milk out of a gallon jug!" (January 28, 2021: x.com/ihors3/status/…) * "The SI % Float is the traditional calculation, the S3 SI % Float includes shares shorted in the denominator as every short sale creates a synthetic long that is also tradable in the market. Both the lender and buyer of the short sale can sell their stock at any time." (x.com/ihors3/status/…) @ihors3 is the first person I called "them" and "outstandingly retarded". 4. Key Problems in the Market/System Related to GME * Burry's view: Fragility from layering/synthetics; SEC ignores corners; GME as singularity ("There really can’t be another GME", January 29, 2021). * Counter arguments: Systemic corruption via naked shorts enabling "cellar boxing" (profiting from bankruptcies at expense of companies/employees); unfair design where individuals hold only "beneficial rights" (no true ownership/voting), brokers pocket 100% from counterfeits; widespread wrong prices in 100s of stocks due to FTDs/volume (x.com/beyond_mythos/…); interference (buy halts, FUD). Attic Boxing extends this to high-priced stocks (P/B >4) for bigger profits (x.com/beyond_mythos/…). I personally think there was and is naked shorting in $GME and in nearly all other securities as shown in my research, the number of new naked shorts for $GME is far bigger than the closed ones, the sneeze had nothing to do with shorts closing and the problem is not about layering, it is about systemic widespread fraud. Counter measures in my opinion are enforcing a naked shorting ban and ensuring fair price discovery by restricting dark pools. I am happy to discuss all the points, let me know what you think. Now that we have discussed the outside perspective and brought counter arguments, let us have a look at the inside perspective. --- inside perspective (activist investors) --- We will first look at what $GME activist proposed, discuss the results of their suggestions, then at what I found was going wrong inside of $GME and finally propose a new financial metric, called operating income bullshit adjusted (bs adjusted) which should be incorporated in the next IFRS. What was suggested (sec.gov/Archives/edgar… p. 31): 1. Tiger Management: Sell the noncore Tech Brands division 2. Hestia: Implement significant SG&A cost savings 3. Hestia, Burry: Repurchase shares 4. Permit and Hestia: Sell the 22-seat luxury Bombardier CL-604 private jet 5. Permit and Hestia: Add new directors with the ability to lead a turnaround effort 6. Permit and Hestia: Individual members of the Board should personally purchase shares Burry further focused on (from his latest post): 7. Sale of hard assets such as real estate, thinking of sale-leasebacks 8. He shows an email from 9/6/2019 where he says the company jet needs to go, this was already targeted under 4 on 7/22/2019 9. Burry shows a lot of items are on sale roughly 7/12/2019 10. Share volume to justify and see when a buyback is happening Let us go through those one by one: 1. Sale of Tech Brands division: GameStop did sell its second most profitable segment by profit margin and by absolute profits inflation adjusted for less than they had accumulated it as well as for 1.2x gross profit (and probably 3.7x operating income), which is unusually cheap by itself. This deal is clearly against the long-term or even short-term value for shareholders (x.com/beyond_mythos/…). 2. Nothing against cost savings, but probably they were the wrong thing here. We'll see why later. 3. In general I showed that of those companies buying back shares 60% had a negative return on those buy backs and half of all buy backs yielded -21% or worse (x.com/beyond_mythos/…). Thus, I am very skeptic when it comes to buy back, especially when they happen at highs. GameStop bought back shares for ~$200m in 2019, $2bn between 2009 and 2019. In January/February 2020 the market capitalization for GameStop was under $250m, showing a negative effect of the buyback from 2019. When Ryan wrote the $GME board in November 2020 the yield on all buy backs was -90% or losing $1.8bn cash, not adjusted for inflation. Not as bad as a deal compared to the Tech Brands division, because of lost cumulative profits, but resulting in a loss for the company and shareholders. 4. and 8. the jet was sold June 5, 2020, for net $8.6 million (sec.gov/Archives/edgar…). A really minor thing compared to 1 and 3. 5. Hestia elected Raul Fernandez, who now works with Larry Cheng at Volition Capital and Liz Dunn. I mean if Larry employs Raul that stands for itself, right? Further track record is Broadcom board from 2020-2024 (+303.32% $AVGO) and DXC Technology from 2020-present ( -20.71% $DXC). Liz works at Teneo from 2020-present which is private and 2024–present at Caleres (-65.28% $CAL). 03/19/20 three new directors were added which left when Ryan got elected. Thereafter, Fils-Aimé has a negative track record, Simon a mixed and Symancyk also a negative to mixed track record (x.com/beyond_mythos/…). Overall I am skeptical besides probably Raul. 6. Valid point that the board should have skin in the game. However, I always thought the owner should go or send a trusted person on a board, not someone on a board become an owner. 7. Yet, I am not convinced a long-term owner would ever use real estate sale-and-leaseback. Rather it seems to be a short term measure to boost current cash in exchange for future costs. 8. see 4. 9. GameStop was having fire-sales in August (see x.com/beyond_mythos/…) which led to massively declined inventory. If shelves are empty (see old Bed Bath and Beyond at the time) customers cannot shop and will probably visit the store less often because of bad experience. In my opinion the ridiculous fire-sale should have been evident by a simple search on X/Twitter at the time and should have been called out. 10. While it is good to keep track of the volume (see also my Volume Turnover research), Burry's focus on short term stock price and volume movement doesn't add to the long-term success of the company. However, he found one of the biggest diamonds out there. Thank you Michael Burry. From here we can summarize that the company would have been better off: * without the sale of Tech Brands at a "inflation adjusted" loss or at least a sale for fair value, * without the share buybacks, * long-term without any sale-and-leaseback, * without the fire-sales and inventory cuts and * without the massive impairments reasoned by projected sales declines (for Tech Brands) or by declining share price (see x.com/beyond_mythos/… and 10-Ks) --- inside perspective (operating income bs adjusted) --- As we have just identified a lot of things the company would have been better off without, now let us just pretend they didn't happen. As we are working with projections and assumptions, the actual results will not be exact, but the direction will give us an indication and we can argue from there. I call all of the things that happened above *bullshit*, therefore we will adjust the operating income as if the bullshit didn't happen. We get the "operating income (or EBIT) bs adjusted" which we will compare to the actual "operating income (or EBIT)", measured in absolute $ and as operating earnings yield. Operating earnings yield means how much $ operating income a company generates for each $ stock price. The higher the operating earnings yield the better. An operating earnings yield of 1 would mean that the company generates $1 operating income per $1 stock price. It is calculated with "operating earnings yield = operating income / market cap (*100 as percent)". Here come the assumptions: * Tech Brands never got sold and $199m operating income in 2018 and 2019 (in 2017 they generated $594m gross profit and GME SG&A dropped by 395 in 2018 reasoned by exactly this sale; 594-395 = 199) * Share buybacks didn't happen and their expenses are added to the operating income, while in return we assume no reduction in total shares outstanding to calculate the operating earnings yield * The price per share would still be the same, if we assume a lower share price and thus equal market capitalization, the operating earnings yield would be even higher (and better) * We remove the, in my opinion, not substantiated massive impairments and add them to the operating income Charting this looks like: (raw data in the replies) As an example here the calculation for 2019: * Operating income bs adjusted (383.70) = reported EBIT ($-399.60) + Tech Brands EBIT from 2017 [Tech Brands gross profit 2017 ($594m) - SG&A Tech Brands 2018 ($395m)] + impairments ($385.6m) + buyback expenditures ($198.7m) * The Tech Brands have some discrepancies in their reporting, 2017 figures where in my opinion worsened to make it look bad for an undervalued sales (e.g. 2017 shows $594m in gross profit see sec.gov/Archives/edgar…, while adjustment showed only $555.2m adding impairment which make it even appear loss-making, see sec.gov/Archives/edgar…), that's why I took SG&A from 2018 (which aligns with 2016). This might be wrong, but wouldn't change the outcome significantly (~$110m less in operating income over the whole period) Wow, the green bars and lines do look very much better than the red ones, right? Still the bar in 2019 is dropping and since we lost profit transparency per segment in 2019, we have to trust what they tell us, that is "[t]he increase in gross profit as a percentage of net sales was primarily due to a shift in product mix to higher margin products, driven by the decline in lower margin video game hardware sales, as well as lower promotional activity in the fiscal 2019 holiday season compared to the fiscal 2018 holiday season" (sec.gov/Archives/edgar…). Adding that the Tech Brands were technically sold at a loss when adding inflation and neglecting former impairments which led to the sales "profit", we could sum up the 2013 to 2019 operating income and subtract from the operating income bs adjusted, which gives us a difference of roughly $3.3bn (operating income of $1.3bn vs $4.6bn; ~$1.4-1.9bn from impairments, ~$0.4bn from Tech adj, ~$1.5bn from buybacks 2013-2019). Removing impairments the difference is $1.5bn - $1.9bn. That's the amount shareholders would have been better off with our bs adjusted actions. Not bad right? Should executives be liable for this amount? Hm. Okay, we didn't prove that our approach would have been definitely better, but we got a pretty strong feeling and basis for discussion at this point. Why did none of the activist investors bring those points? --- wrapping up --- If you were an owner, board member or executives how strong would you want your morals to be and what would it mean for your actions? Its easy to lose the path when big money comes your way. Stay in power, on the path of love, help others, be useful. For Michael Burry's post we can pretty much disprove or at least have pretty strong arguments why his outside view on naked shorts, the sneeze and the current short interest are rather wrong than right. We also see that the approach from Tiger, Hestia, Permit and Burry (Scion) on an inside perspective were rather harmful for long-term investors than not. I am not talking about morals at this point. Maybe they just didn't know any better and everyone should be given a chance to right their wrongs. Besides the discussion about the outside and inside perspective of $GME this post should be seen as guidepost, showing how to apply strong morals, how to spot short-termisn and evaluate damage done by overpaid consultants and executives. How to spot such behavior and counterargue. Today, I am sure only very, very few will read this post. But maybe, at some point in time, it can help to improve future long-term shareholder value, at scale. God bless you.