sinus rhythm

227 posts

$kta significantly frustrates me more than the other scams. At least scams like $KNX make it obvious they're a scam with any basic research. Keeta is far more elaborate and pulled a lot of people in. It's ran by a malicious team with rogue OTC deals, rogue advisors, and no use.

English

@Tesitfy178672 @Syno_0x And how do you know that? You jump and down about evidence … where is yours.. or you just spewing verbiage yet again

English

This was back in November of last year. What are the chances $KTA Keeta is involved here?

It fits the criteria almost perfectly, and with recent announcements, the overlap is becoming harder to dismiss.

They are always happy to smear their name on Tempo and other ''flashy'' chains but all of sudden dont want to disclose partners. Kinda weird.

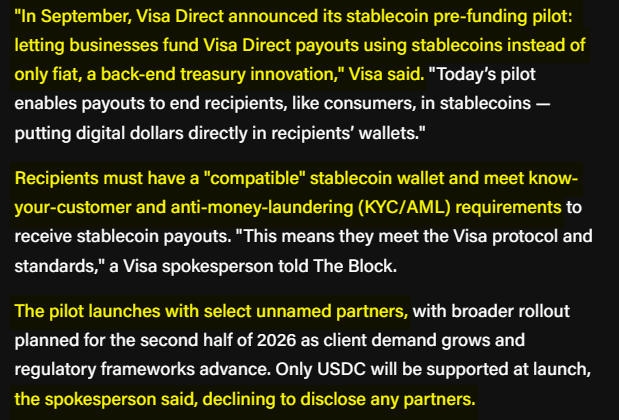

One of the pilot members was BVNK, but from what I’ve read, there are multiple.

Probably nothing?

Keeta@KeetaNetwork

(3/8) Keeta will support Visa Direct rails for outbound payments. This enables: • Payouts to 190+ countries over 90+ rails • Near-instant settlement • Instant funding/withdraw via linked debit cards Users no longer need to wait on legacy banking rails for funding and payouts.

English

You’re reducing this to “you don’t need a token,” but that ignores the key issue neutrality vs control. Without a native asset, someone owns and governs the rails, which isn’t true shared.

Saying “they did it before KTA” actually supports my argument point as early systems are often centralised, then evolve into shared, tokenised scalable decentralised infrastructure. The basis of KTA architectural evolution.

And comparing it to other chains misses the nuance. Most are building features, not full-stack financial infrastructure with compliance, fiat rails, and settlement integrated. Name one other L1 that is competitive in architecture and design.

As far as utility and usage is concerned, judging it purely on current usage is IMO short-sighted. Infrastructure isn’t proven on day one, it’s proven when institutions plug in. Your point is like judging an airport once the tarmac is laid and complain about the lack of air traffic. The real question is whether Keeta is being built to support institutional usage once they plug in. This is a resounding YES

—————

Yeah, and that's what it is, and I gave many issues that would restrict its decentralization. Ok ive not seen them .. enlighten me!

Ok? Join the club, a lot of chains are doing that and institutions seem far more interested in the others. And at some point we can't use the "they need more time" excuse, the chain is live, so it is judged as a live product. Otherwise why launch it? Well firstly .. when people hear “mainnet” they think, finished, polished, complete. In reality it means, that core systems are live and stable allowing for further development and integrations in the live arena. If they waited until everything was perfect, no one could build on it, no integrations could start and an operational feedback loop wouldnt exist. There are too many limitations in the test environment and feature testing can’t be replicated unless a live operational network exists.

English

"Making a statement like “ you can to do what Keeta is doing without a token “ is only true if one is comfortable with a fully centralised system."

Yeah, and that's what it is, and I gave many issues that would restrict its decentralization.

"The moment you want shared infrastructure across institutions, neutral settlement between competing parties one is going to need a native asset."

You could just as easily use any medium of exchange rather than one that is arbitrarily created. Like I said, they operated this prior to KTA existing as a cross-border payments app.

"The real question isn’t “ is it busy now” it should be “ are they building something that institutions can use” and the answer to that question is yes."

Ok? Join the club, a lot of chains are doing that and institutions seem far more interested in the others. And at some point we can't use the "they need more time" excuse, the chain is live, so it is judged as a live product. Otherwise why launch it?

":Have you read in any detail the keeta white paper?."

I've been over literally all of the Keeta docs. If there is something I missed, maybe just reference it specifically.

English

Keeta Network | Is a Visa Direct partnership that bullish?

Keeta → Connects → Visa Direct → reaches bank/card users.

On paper, that closes a gap, crypto plugging into real-world payout rails. But acces to Visa Direct is not unique, thousands of players already operate on that layer, so the integration itself doesn't create much of an edge.

The more ambitious angle is the idea of becoming the default settlement hub betwaan all rails. But you are competing with 2800+ platform integrations..

If anything, a slower market over 4 to 6 months is actually useful here. it gives time to observe whether Keeta can translate integrations into real activity, development progress, implementation, and actual volume flowing through the network.

Until that shows up, this looks more like incremental progress than something that materially shifts their position.

English

This is my view as I’m no expert. The real question is and what a lot of people fail to ask them themselves before criticising is what problem is KTA trying solve. Making a statement like “ you can to do what Keeta is doing without a token “ is only true if one is comfortable with a fully centralised system. The moment you want shared infrastructure across institutions, neutral settlement between competing parties one is going to need a native asset. The question shows lack of appreciation of the Keeta bigger picture.

As far as current usage, utility and liquidity concerns you’re judging a network at the infrastructure stage like it’s already at the usage stage. no network starts profitable for validators on day one. Infrastructure development comes first, usage follows. The real question isn’t “ is it busy now” it should be “ are they building something that institutions can use” and the answer to that question is yes.

As for the bank acquisition.. it was not “ oh let’s buy a bank” it’s an essential puzzle piece in the overall infrastructure … it’s what enables control over fiat rails, compliance and settlement which are the exact constraints that stop most blockchains from being used in real financial systems. Without that, you’re just another to use your words a “glorified database.” With it, you can actually provide bridging on and off chain in a compliant way.

Have you read in any detail the keeta white paper?.

English

Why they are acquiring a bank is obvious, but how Keeta the network fits in, and especially KTA the token, is not as clear. That's what I'm asking you about.

Right now the network is still a glorified database and it has zero liquidity for anything and zero utility for anything besides trading for shitcoins that no one wants. Keeta holds a shit ton of KTA so governance is moot even if the network decentralized. No one uses the network either, so there is little incentive for independent teams to run what are likely expensive validators because they aren't going to be profitable without heavily diluting KTA with inflation.

Seems like they're positioning themselves like a fintech and then saying "oh yeah here is this token too" and then trying to create demand in ways that only work if you actually offer qualities that are at odds with their current

You can do what Keeta is doing without a token, in fact, that's what they were originally doing (LFG?), which I'm sure you know about with your very deep research.

Sorry for the "late" response 3.5 hours later on this Easter Sunday... I can't believe I'd keep a rando on X waiting so long just because I had holiday plans.

English

@YOjawnZiLLA @ReddBanksss So do you want answer my question?

English

@YOjawnZiLLA @ReddBanksss You made the comment “ Seems like Keeta is more concerned with becoming another bank compared to becoming a crypto project.” Let me ask you this. Why do you think KTA has a focus on acquiring a bank and what importance has it in the overall KTA infrastructure.

English

@SinusRhythmPlus @ReddBanksss Well, do you want to push back against my assertion or are you just another KTA bull who feigns indignation and argues semantics in order to avoid actually talking about the project itself?

English

$KTA

Everyone who says the project is next level never truly used it. The web wallet & explorer are atrociously slow. You need to KYC for things you shouldn't need to (e.g.transfer tokens from eth). The TPS is all in a staged env. Anchors are also very slow. Nobody is using this

English

@YOjawnZiLLA @ReddBanksss If anyone’s making an assertion, it’s you. You might want to sharpen your grasp of English before throwing it around. I don’t need to spell it out—do a bit of research instead of making weak claims and embarrassing yourself.

English

@SinusRhythmPlus @ReddBanksss That's not elaboration, that's just stretching out the same vague assertion into more words.

English

@YOjawnZiLLA @ReddBanksss Once you understand how financial compliance works in crypto, it becomes clear why acquiring a bank is essential—and how it creates second- and third-order effects that ultimately strengthen the value of $KTA within its broader strategy.

English

@SinusRhythmPlus @ReddBanksss ???

Knowing banking compliance explains how a crypto asset has value accrual?

Can you elaborate?

English

@YOjawnZiLLA @ReddBanksss Then you need to research financial compliance for the bank

English

@ReddBanksss Seems like Keeta is more concerned with becoming another bank compared to becoming a crypto project.

Not sure how any of this drives value or even relates to the chain itself or KTA the asset. Still struggling to understand who Keeta is supposed to be for.

English

@nottellingyou73 @luboss302 @KeetaNetwork From what you’ve just written it’s clear you have little understanding of what’s being built… this is not another pumpfun nor is it just another L1 blockchain.

English

I think his focus is wrong. Adding more features isn’t what makes a crypto successful. He needs to get people to adopt the network before adding more features. All sounds cool to me but I have no idea how easy it is to access and use all these features.

Pump fun was successful because they made creating a meme token extremely easy and simple.

English

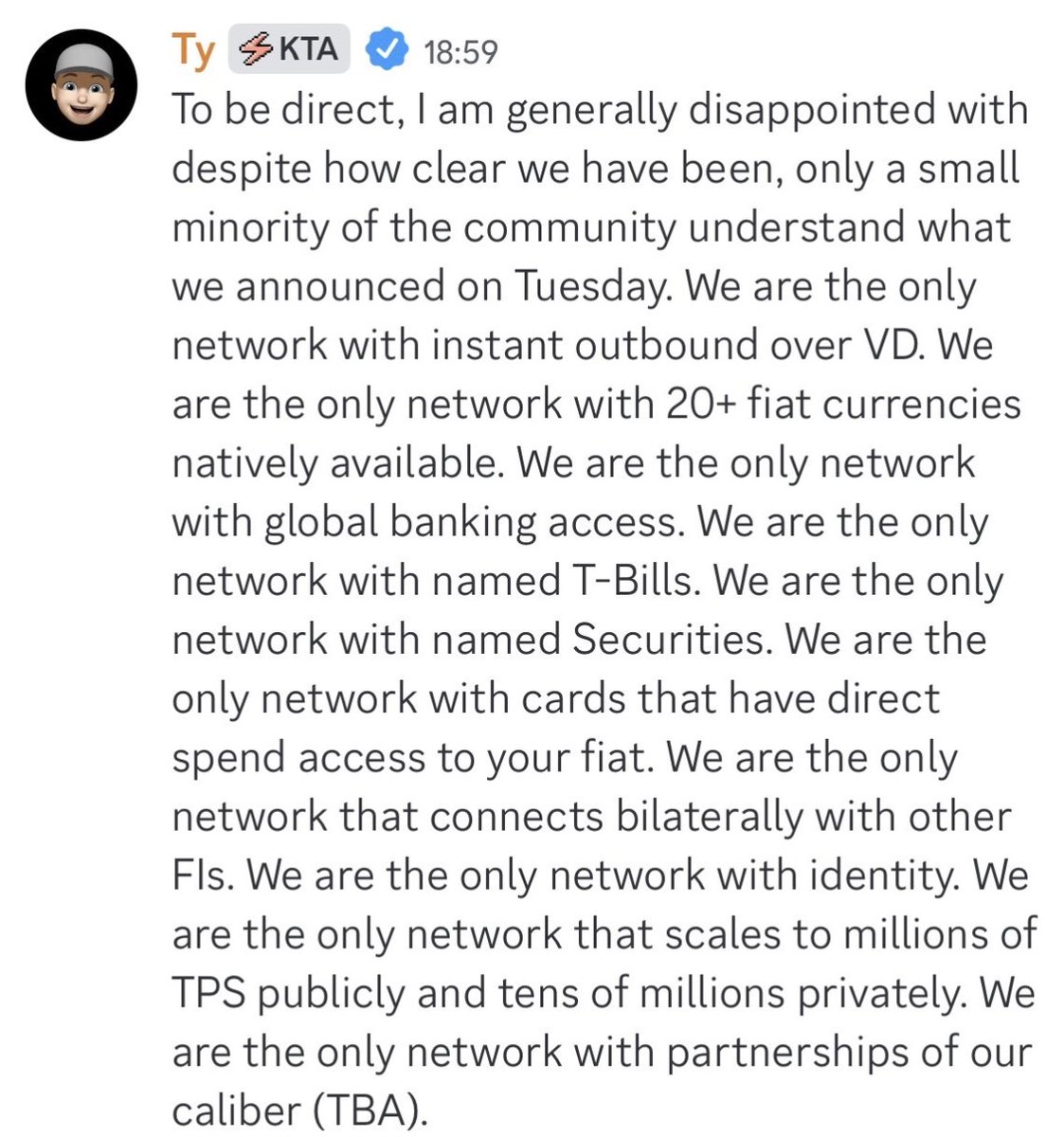

@KeetaNetwork is UNIQUE in many ways.

Keeta is THE ONLY blockchain network

1⃣ with 20+ fiat currencies natively available

2⃣ with global banking access

3⃣ with named T-Bills

4⃣ with named Securities

5⃣ with cards that have direct spend access to your fiat

6⃣ that connects bilaterally with other FIs

7⃣ with identity

8⃣that scales to millions of TPS publicly and tens of millions privately

9⃣with partnerships of our caliber (TBA)

$KTA is the ticker

English

@flordasunset Hahaha … post shit like this like bro has influence and a truck load of followers…

English

@Tesitfy178672 And neither can you … you pull shit out of your ass all day long.. when your mum rolled over this morning she told me you are gay

English

$kta

Just about nobody is using the network. Visa isn't interested in Keeta. Keeta is interested in Visa. Big difference. There is no "partnership", Keeta is supposedly going to use their services (still has yet to happen).

Any claims made by Ty the liar cannot be trusted.

English

@Tesitfy178672 Explain to me hthen why not one of the named integration / partnerships that KTA have announced have publicly denounced any such association . Surely if this is such a dodgy project they would want to protect their name/business.

English

@Tesitfy178672 Based upon what? How are you justifying your numbers besides ass plucking

English

@TraderTurtle69 @KeetaNetwork Name one of the millions of projects that you claim successfully did what KTA is doing? Just one … surely you can do yhat?

English

@KeetaNetwork Wow it’s not like a million other projects already did this weeks ago

English

English

Saying they’re competitors misses the mark entirely.. Tempo is getting early usage because it’s solving a narrow, immediate problem, but that doesn’t mean it’s “leagues ahead”—it just means it’s earlier in its adoption curve. KTA is tackling a far more complex, institutional-grade system, and that kind of infrastructure doesn’t show instant usage; it takes time to build, integrate, and scale properly.

Judging KTA purely on current usage is short-sighted—early traction doesn’t equal long-term dominance. The real difference isn’t who has more users today, it’s who’s building something that actually holds up when the broader financial ecosystem moves on-chain.

English

@Tesitfy178672 Blah blah blah .. what you say is BS… you’re gay … you have a small Weiner … but you take your BFs like a trooper

English

$kta

Today was bad. Let me break it down:

- Ty already discussed most of those features

- None of what they announced is actually out right now, still in "WIP"

- Visa partner is BS. Keeta is just using their service

None of this will bring users or cain activity.

English