Nexus Studio

114 posts

DOW Rapid Response@DOWResponse

.@SECWAR “In the Indian Ocean—an American submarine sunk an Iranian warship, that thought it was safe in international waters. Instead, it was sunk by a torpedo—Quiet Death. The first sinking of an enemy ship by a torpedo since World War 2. Like in that war—back when we were still the War Department—we are fighting to win."

ZXX

President Donald J. Trump on the United States military combat operations in Iran:

English

There's currently a massive online war raging in South Korea against Indonesians in particular, and against ASEAN countries in general, including Malaysia, the Philippines, Thailand, and Vietnam.

The conflict began after Koreans broke the law at a party in Malaysia, and it has escalated dramatically in the last two days.

In the tweet in question, a Korean posted a picture of monkeys and claimed it was an Indonesian family.

The bullying has reached incredibly vile levels, with Koreans using unimaginable vulgar language and engaging in unspeakable bullying.

Indonesians, however, have not remained silent.

The original story began after repeated complaints about the perceived arrogance of Koreans at parties in Indonesia. Koreans travel to Indonesia, attend parties, break the law, and look down on Indonesians, which finally pushed Indonesians to their breaking point and sparked the conflict.

The dispute is so significant that it has made headlines in both countries, but so far, there has been no official diplomatic intervention between the governments.

English

Indonesia

$GORO $GOLD $SILVER

Investment Thesis

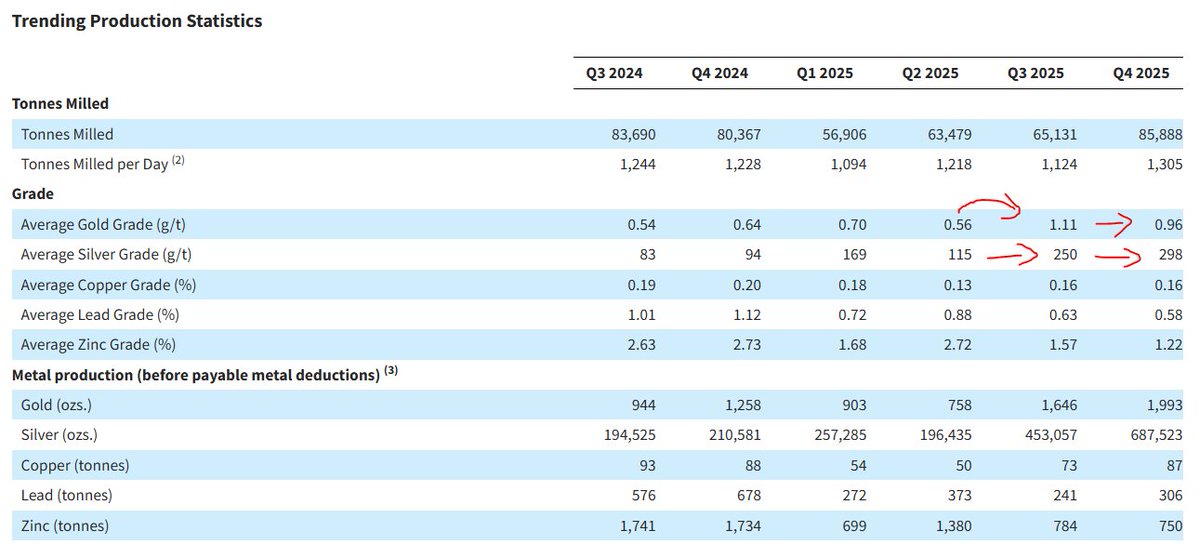

1. Gold Resource Corporation is a mining company producing gold and silver from the Don David Gold Mine (DDGM) in Mexico. Since 2022, revenue deteriorated and the company drifted into financial distress.

2. For a gold/silver miner, revenue is basically driven by three things.

3. First: grade — how much gold/silver is in the ore for the same mining effort.

4. Second: production volume — how much you actually mine/process.

5. Third: realized price — the spot price you sell into.

6. That’s essentially the whole revenue engine.

7. Once you know revenue, you need to know costs. Globally, miners use AISC ($/AuEq oz sold) as a standard so production costs are comparable across companies. In simple terms: cost per gold-equivalent ounce sold.

8. Looking at the AISC line in the table, you can see that during 2019–2022 the cost base was roughly $600–$1,200 per AuEq oz.

9. Multiply that by quarterly gold/silver sold (converted to AuEq) and you can estimate Total AISC (my shorthand for total sustaining cost burden).

10. The chart shows that from 2021 through 2024 Q4, a mix of declining production and declining recoveries led to a steady downtrend in revenue.

11. Market cap obviously collapsed too, and in 2024 revenue fell below Total AISC, so deficits piled up. The stock went all the way down to around $0.20.

12. To survive, in 2025 they diluted hard: a big ATM program with HCW plus other financing to cover losses and fund investment (see the quarterly share count at the bottom of the table).

13. Then the “holy shit” moment: they were originally planning to open up the Three Sisters vein in 2025 Q3. I have no idea if they “anticipated” today’s silver price when they made that plan.

14. But they used the financing to buy equipment, hire a specialized contractor for Three Sisters, and apparently improve mining methods/practices.

15. Right as they started mining it, silver prices took off hard. In the table’s realized-price section, you can see silver suddenly hitting $41/oz (quarterly realized).

16. Three Sisters also turned out to be a high-recovery/high-grade area for gold and silver. Yes, early quarters after opening a new zone can look better and then normalize later — but they’ve only been mining it for 1–2 quarters so far.

17. On top of that, productivity jumped due to operational changes. The production section shows that while it’s not back to 2019–2022 levels, production exploded from early-2025 into 2025 Q3–Q4.

18. So: grade up + volume up + price up → margins begin to explode.

19. Revenue was about $25M in 2025 Q3 and around $48M in 2025 Q4. At that time, average realized prices were roughly $4,200/oz gold and $55/oz silver. Where are prices now? As you know, roughly $4,900/oz and $100/oz.

20. The company has stated they plan to keep Three Sisters at 40%+ of total production in 2026 — i.e., they’re saying they’ll mine even more from it.

21. If you assume similar production + grade as 2025 Q4 and plug in today’s metal prices, my rough 2026 Q1 revenue estimate lands around $72M.

22. For commodity producers, in a rising price environment PSR (Price-to-Sales) matters a lot because when price lifts revenue, margins can re-rate fast.

23. They didn’t give a fully detailed Q4 disclosure yet, but they did disclose production/sales/recoveries and said they ended with about $25M cash — implying they successfully swung back toward profitability.

24. If gold/silver stay anywhere near current levels, cash generation vs market cap could look extremely attractive.

25. So is it actually “cheap”? At the bottom of the table I computed quarterly PSR using average share price + share count (market cap) vs revenue.

26. Before the balance sheet got wrecked, PSR was around 6x in 2021. In the 2024 worst period it fell to around 1.3x. Using the 2026 Q1 revenue estimate, it’s about 3.1x.

27. Taking the inverse of PSR gives a sense of “sales yield.” On my 2026 Q1 numbers, the company could be generating around 32% of its current market cap in quarterly sales.

28. If financial stability returns and they regain durable cash generation, a reversion closer to the historically stable 6x PSR (2019–2021) wouldn’t be crazy.

29. Now compare to a major: $NEM (Newmont) is a roughly $129B mega-cap with roughly $21B annual revenue, trading around 6x PSR (annual basis).

30. If you set $GORO’s PSR using recent revenue (2025 Q2 through my 2026 Q1 estimate), it’s around 1.06x. And if gold/silver prices hold through 2026 Q2–Q4, PSR could compress even further (i.e., look even cheaper).

31. I’m not saying a small-cap like GORO deserves the same multiple as NEM. It probably doesn’t.

32. My point is: the more reasonable “anchor” might simply be GORO’s own historical PSR range if the balance sheet and cash flow normalize.

33. Net: at current levels, by almost any comparison, the stock looks cheap relative to the cash-flow potential implied by recent operating momentum. After the latest results, it went +50% pre-market and then closed -15% on a nasty sell-the-news move. I bought — I see it as an opportunity.

34. Biggest risk is gold/silver price drawdown — e.g., geopolitics easing, Fed tightening, or a more hawkish successor to Powell, etc.

35. Also, per a release on Jan 22, about 20 contractor employees (from a contractor whose agreement ended) reportedly blocked the mine access road and are on strike. That might be part of why the stock sold off on earnings. Hard to know.

36. If this disruption drags on, it can clearly hit production/revenue — so it’s a real risk.

37. Regarding the images: the first shows how gold/silver grades jumped sharply after Three Sisters came online in Q3 (from company disclosures).

38. The second compares quarterly revenue vs AISC vs market cap — that spread is essentially your margin picture, and it makes it easy to visualize how margins could expand into 2026 Q1 under my assumptions.

39. The third table summarizes quarterly data from 2019–2025: production, grade, realized prices, revenue, AuEq ounces sold, AISC, OCF, average share price, share count, market cap, and PSR.

40. I don’t know where gold and silver go from here. It feels like we’ve entered an overbought zone — not something a retail investor can forecast cleanly.

41. But even if gold/silver simply hold $4,500 and $50, I expect GORO to generate strong cash flow. If current prices persist, even better — but that’s the happy path.

42. Finally: this is NOT a recommendation to buy. I’m just laying out my thesis. This is a small-cap miner — risk is high, so size/position accordingly.

English

Nexus Studio รีทวีตแล้ว

🐶 Team $DOGE: Hit the Like button

🐸 Team $PEPE: Hit the Retweet button

May the best memecoin win!

English

Nexus Studio รีทวีตแล้ว

Nexus Studio รีทวีตแล้ว

$PEPE has been consolidating and coiling up for the past 570+ days preparing for the massive parabolic run that is about to begin

2 years of waiting for 3 months of GLORY

I have been a $PEPE bull since a week after it's inception, and all of that patience is about to pay off.

English

Nexus Studio รีทวีตแล้ว

#Iran has been deceived for a long time! Can you believe the "good intentions" of the White House?

English

Nexus Studio รีทวีตแล้ว

Nexus Studio รีทวีตแล้ว

🚨BREAKING: Google will soon install an app called #AndroidSystemSafetyCore

They say it's a "safety measure" to protect your #privacy, but in fact it's client-side scanning.

Yet, we all know that client-side scanning is bad: tuta.com/blog/eu-client…

Deinstall the app #Android: System -> Apps

English

Why do we even have alarm clocks? If my responsibilities are that important, they should naturally wake me up out of fear.

English

Our BOME-PERP and NOT-PERP markets are now in full-trading mode on Coinbase International Exchange and Coinbase Advanced. Limit, market, stop, and stop limit orders are all now available. $BOME $NOT

English

Nexus Studio รีทวีตแล้ว

@MantaNetwork Anyone from support team available to Help Please..

My Metamask been drained all STONE is gone!!!

Please give some support🙏🙏🙏

English