@Noahpinion Interesting juxtaposition in that first photo - very beatnick looking room but that looks like a $5000 Sonor Vintage drum kit!

English

Andy Glover

726 posts

@andyecon

Research and Policy Advisor @KansasCityFed doing macro and labor; Minnesota PhD; Views and tweets are my own. Retweets ≠ endorsement. https://t.co/gHcXdyyG5O

🇯🇵 Le Foyer Yoshida de la prestigieuse Université de Kyoto est autogéré par les étudiants. Malgré les signes évidents d'insalubrité, ils le chérissent comme un bastion de la libre pensée, face à la hiérarchie stricte qui domine la société japonaise. ➡️ u.afp.com/SLgi

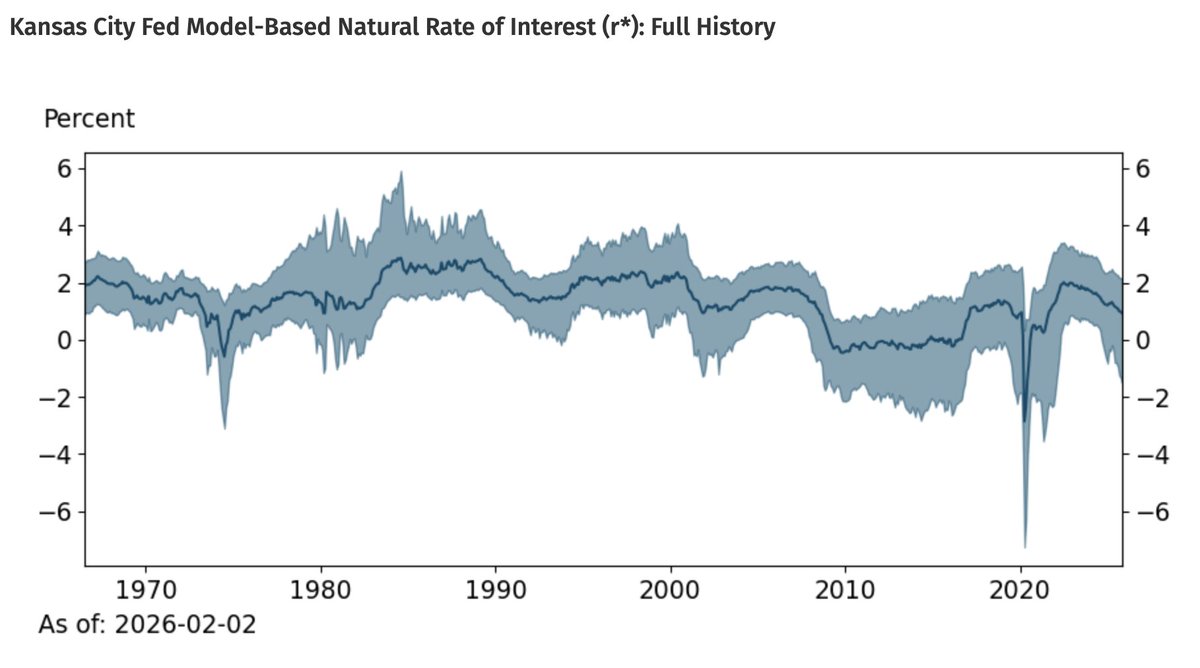

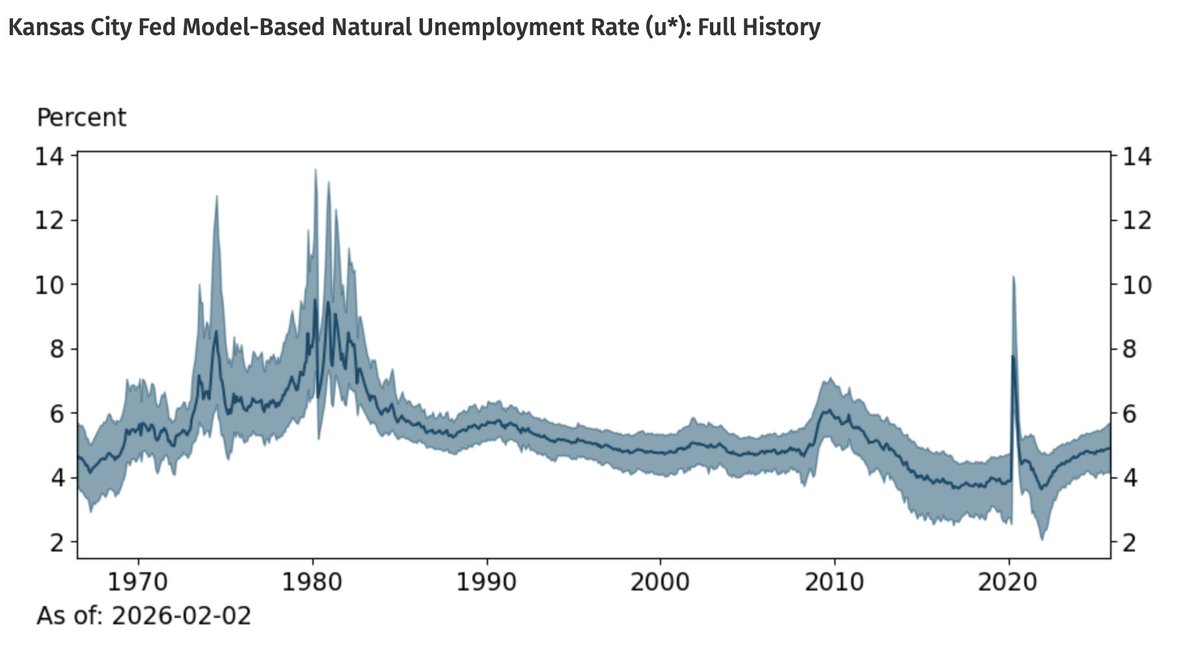

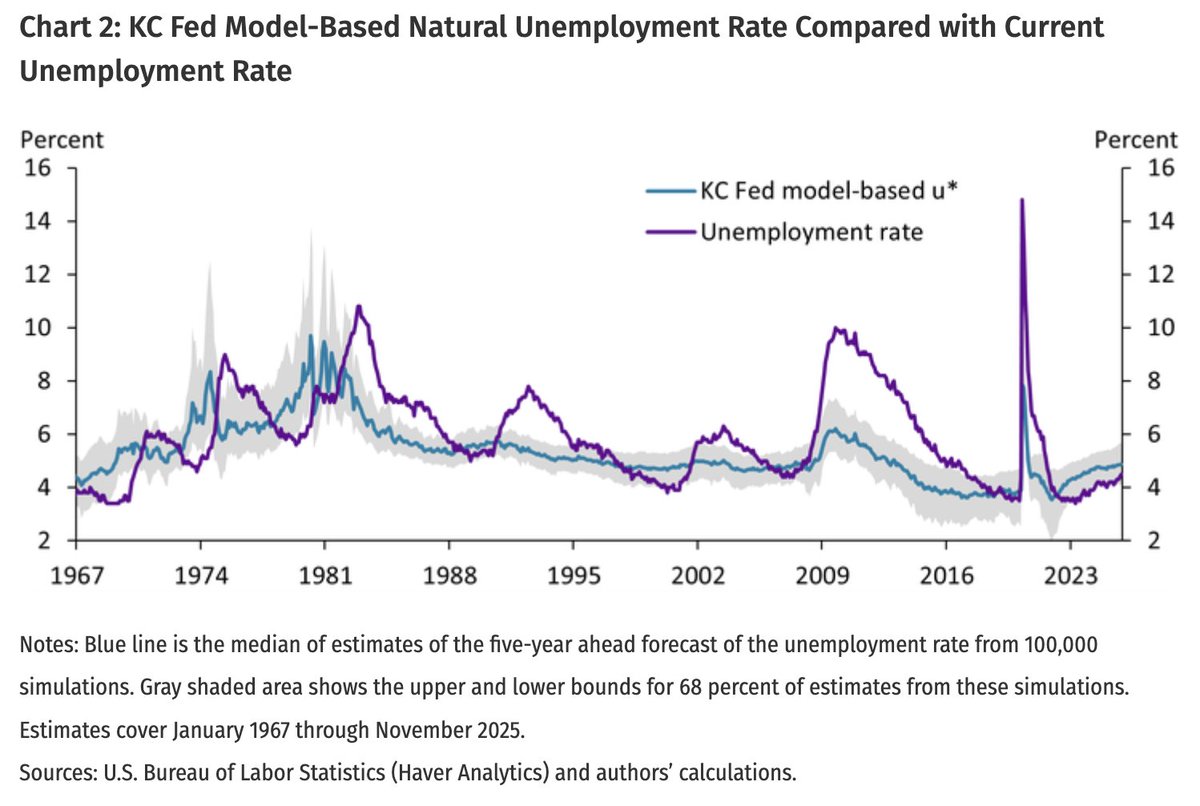

We have introduced the KC Fed Model-Based u* and r*, monthly estimates of these two vital objects. We use the methodology of Lubik and @cmatthes_econ on monthly data and unemployment rather than output growth. So what do the data look like?

Relatedly, the KC Fed Model-Based u* indicates that labor markets were slack for most of the 2010's even with inflation below 2% and policy rates near zero. Labor markets became balanced a few years before the pandemic, became tight in 2022, and are now roughly balanced again.

Today I worked through the arithmetic of how I came to my policy projections for appropriate monetary policy. There's a lot of numbers in the speech, but given the divergence between my views and other FOMC members, I felt it necessary to be meticulous and transparent.