@d4ytrad3 Or the exit liquidity value of $SPCX is lower and the market isnt dumb...

English

harfangcap

12.2K posts

@harfangcap

I pick up pennies in front of a steamroller.

$SATS owns about 53m shares of $SPCX. If you do the math, this is an insane discount now that we see a stable market on size for SpaceX . Strong Buy

With SpaceX getting priced at $135 today, Bloomberg estimates Musk's net worth is now $970.5B Tomorrow, any pop above the IPO price (or a Tesla rally) could make him the first Trillionaire!

S&P 500 is up 9 days in a row and 9 weeks in a row. One of the strongest, most unrelenting rallies in history.

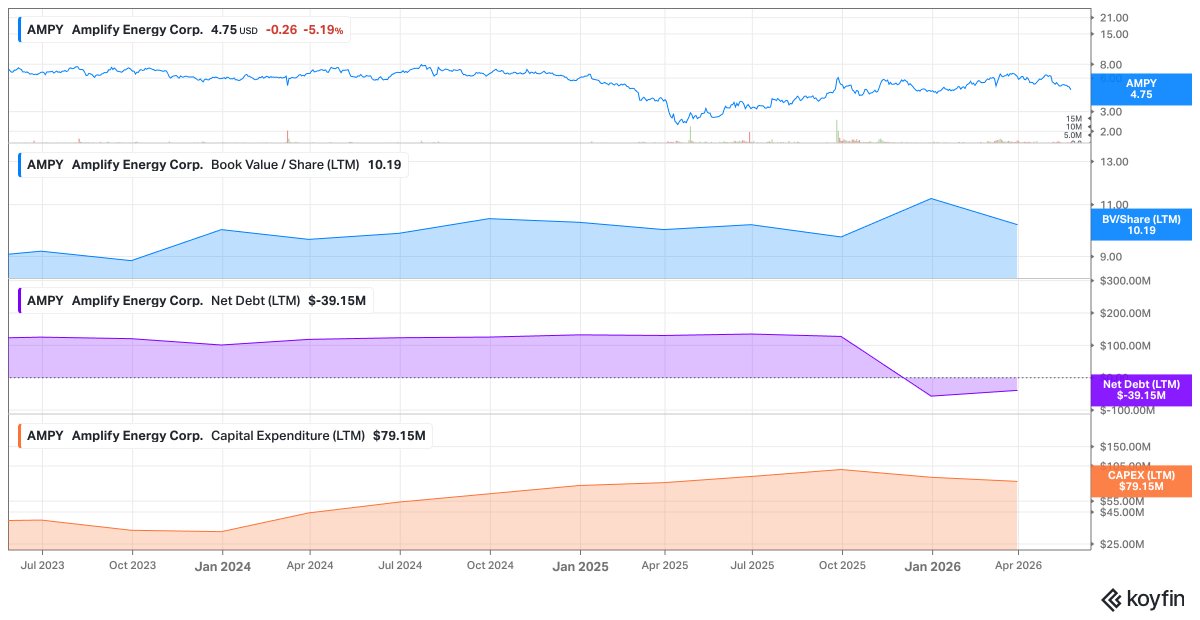

I think the bear replies are annualizing the wrong quarter. Q1 looked ugly: $3.8M EBITDA / -$18M FCF. But 2026 guidance is 6.7–7.9k bopd, $20–45M EBITDA and $45–65M capex. That is clearly a build year, not normalized earnings. Production should ramp through the year as Beta wells come online. Royalty relief started May 1 and adds 600+ net bopd / $1M+ monthly revenue. New barrels also dilute the hedge book, so incremental production should be much more exposed to current oil prices. If $AMPY exits 2026 with a higher oil base and capex drops to maintenance levels in 2027, I think this can do $40–50M FCF next year. With the balance sheet now debt-free, the historical reason they could not return capital is gone. If execution is even decent, capital return should follow. This is new AMPY: new management, new board, directors actually owning stock, same too-cheap assets. Bairoil already has ~$10M/year LOE savings and free CCUS / power optionality that the market is valuing at basically zero. There were specific reasons Q1 production and EBITDA were low that should reverse or improve in Q2/Q3. Those will be the first cleaner quarters for the new structure. By the time it is obvious, the stock likely will not be here. At ~$4.50–5, I think downside is limited absent real execution failure/black swan tail risk at Beta, while upside to $7–10+ is very plausible. Frustrating name in this market, but extremely asymmetric if there are still investors willing to look past one ugly transition quarter. This is not really an oil bet, it's about cash flow and rerating through shareholder returns. Either the market will figure it out or the stock will be forced higher as it is being run like a private company now.

Anyone following $AMPY? To summarize the last 12 months at this small-cap E&P... 1) Terminated merger 2) CEO replaced 3) Sold assets 4) Now have a net cash balance sheet, 5) Doubling down on remaining 2 assets (capex) 6) Trades at ~0.4x book value

I'm fine with this $sei.v raise 41 cents. Considering there are no warrants, the 17–21% discount to the recent trading range is not too bad. Raising gross US$11.5(CA$15.6) . Share count increases 9.7%. I'm seeing an angry reaction in the discussion forums, but what is the argument? "The discount is too big" In this sector, with no warrants, you can't get a smaller discount. "The stock is too cheap now; raise money later at a higher valuation" The valuation is based on the drilling outcomes, farm-out negotiations and the oil price; they can't predict any of those, so they can't predict the future valuation, and can't rely on that for capital allocation decisions. If PEL 90 is happening, and it seems to be happening, which is good, and adding PEL-37 and KON-16 expenses(both acquisitions aligned with the business model), they were going to have to raise eventually, and it's always better to raise before the cash starts running low and the market starts front-running it. The CEO and President are indicated to invest CA$500k. Cash sources and use of proceeds:

Oil price, Sintana, Eco Atlantic, Deltic, EOG. And finally… malcysblog.com/2026/05/oil-pr…