@iuladvocate @mbontrager5 Oh ok well you misunderstood then. I just want to see the historical performance of this uncapped index with 0.75% floor. Please share!

English

Nicholas VanGeest, CFP®, CPFA

3.2K posts

@vangeestguy

https://t.co/JjC51kYdkf

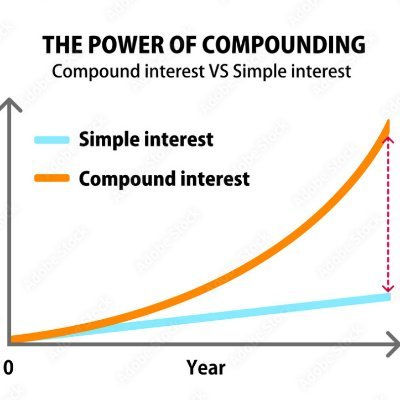

In October 2007 a 64 year old had $2.5 million set aside for retirement. By November 2008 it was $1.2 million. Thirteen months. Cut nearly in half. He did nothing reckless. The market fell 37 percent and took his retirement down with it. Now run that same $2.5 million inside a properly structured max funded IUL. 2008 credits zero. Not negative. Zero. The 0% floor means a down year doesn't subtract. The index drops 37 percent and the cash value just sits there and waits. 2009 the index recovers and his money compounds forward from $2.5 million. Not from $1.2 million. That is the whole thing. He never had to climb back from a loss he never took. Sequence of returns is what quietly wrecks a retirement. A zero you can retire on.

Day 3 of 15. IUL Reality Check. IRC §72(e) lets cash value inside a properly structured IUL compound with zero annual tax drag. No 1099 showing up every spring to take a bite. $200,000 of cash value crediting 8% keeps the full $16,000 that year. Nothing skims off the top while it sits inside the wrapper. Run untaxed compounding like that across 40 years and the gap runs into six figures. Tomorrow Day 4: the 0% floor. Quick gut check before then, what did the S&P do in 2022 and what would a 0% floor have done sitting next to it?