CHILANG-X รีทวีตแล้ว

CHILANG-X

564 posts

CHILANG-X

@xechilang

Bitcoin hodler🚀 & TSLA investor🚀

Macau เข้าร่วม Mayıs 2021

752 กำลังติดตาม71 ผู้ติดตาม

CHILANG-X รีทวีตแล้ว

AI + Crypto = Machine Economy!

我一直在强调一个话题,也坚定的认为本轮牛市开启的开始就是 AI AGENT 和加密货币的天然结合:

就像 Coinbase CEO @Brian_Armstrong 所说的可能机器经济(Machine Economy)时代已经开始出现。

人类支付是消费属性、公司支付在于贸易属性、未来的 AI 支付,是系统的自动协作属性,机器可以自己赚钱,自己花钱,自己雇佣别的机器,这就是这就是所谓的 Agentic Commerce。

未来不是人和人之间使用稳定币,更多是 AI 和 AI 之间的稳定币使用。

我有几个未来可能会影响行情和行业的几个观点:

1️⃣稳定币可能不是为人准备的,而是为机器准备的,几个现在几乎还不存在,但未来很可能会出现的:

稳定币 = 机器世界的货币;

ETH / SOL = 机器世界的清算层;

GAS = 机器世界的“电费”;

钱包 = AI 的银行账户;

私钥 = AI 的财产权。

2️⃣DeFi 不是金融创新,而是机器金融的雏形;

3️⃣真正会把稳定币交易量推到 100 倍的,不是散户,不是机构,而是 AI 的使用数量。

来算一笔账,假设未来有:50 亿人,每个人10个 AI ,那么就是500 亿 AI Agent,如果每个 AI 每天产生 20 次支付行为,那么 500 亿 × 20 = 1 万亿笔交易 / 天。

对比下,现在 Visa 一天大概处理:~7 亿笔 / 天

4️⃣如果这个方向成立,那未来 crypto 最大的赛道可能不是交易所,不是公链,不是 DeFi,

而是类似于这些场景:

AI Agent 钱包、AI 支付协议、AI → API → 自动结算系统、稳定币清算网络、机器身份系统(AI identity)、自动做市 / 自动交易 / 自动结算 Agent。

这是一整套新经济系统,这才是 crypto 接下来真正的大叙事:AI + Crypto = Machine Economy!

Etherealize@Etherealize_io

Coinbase CEO: Stablecoins transactions will grow by more than 100x as AI agents outnumber human beings “The most interesting thing we see now is that AI agents are increasingly transacting using stablecoins. There’s this emerging area called ‘agentic commerce’, and if you believe as I do that eventually there will be more AI agents than human beings . . . and because stablecoin payments are so fast, cheap, and global, I think there will actually be several orders of magnitude more transactions every day — maybe smaller dollar values — as machine-to-machine payments really start to take off.” Source: @NorgesBank (Mar 2026)

中文

$BTC 行情分析 2026.04.03

今天是耶稣受难日,美股和黄金都不开盘,所以我今天只更新比特币这一篇推文,详细展开来说。

图1为BTC周线图。老朋友应该都知道,我在BTC跌至80600时就说过:我们处于熊市周期,且80600无法做底。随后在97900、91200以及下跌过程中的85000,我也都多次建仓做空。近期我也反复强调,6万不会是BTC的底部,核心逻辑就两个字——周期。

我们目前处于熊市中期。假设76000是6万反弹的终点,后续再走一波与97900→60000同级别的下跌,那么熊市中最猛的一波下跌就基本完成了,届时从126000起的总跌幅也将完成80%-90%。

但熊市不能只看跌幅和价格,另一个重要维度是时间。假设2026年第三季度BTC跌至52000甚至48000,届时我们会进入熊市中后期。这一时期可能以多种形式呈现:黄金坑、宽幅震荡、窄幅震荡,甚至极端横盘。

每一个阶段都会有人怀疑周期:跌到80600时不愿意相信牛市结束、熊市开启;跌到6万时幻想熊市结束;后续跌到四五万,又会有人怀疑比特币要归零、加密完蛋。我在这个市场已经8年了,每一轮都有人幻想“这次不一样”,但最终结果次次都一样——周期从来没有改变过。

现货建仓现在还未到时间。今年第一季度我主要操作是合约趋势空单 + 部分波段多单(比如上一波80600起的多和这一波在6万、62500、63000博弈反弹),但我从未幻想熊市结束、牛市提前。

从小级别看图2,我把昨天提到的两种走势进一步细化:

红色路线保持不变:近期直接跌破65000,在62000-63000获得支撑后会有一个反弹,反弹结束后继续下跌,最终跌破6万。

蓝色路线细化了近期不跌破65000的情况:先走一波反弹,找到反弹终点后仍会继续下跌,最终同样破6万。

总之,4月份我们大概率会看到与97900→6万同级别的下跌。126000起的这一波下跌结构完成后转入震荡期时,我或许会开始建现货底仓。

比特TWO@BTCTW0

$BTC $ETH 又要选择方向了?直接跌还是先涨后跌? $XAU 黄金明天开盘怎么走? 一条视频告诉你:

中文

Sounds like Saylor is bullish on $TSLA

Michael Saylor@saylor

Three perfect products: A car that drives you. A robot that serves you. An asset that pays you.

English

CHILANG-X รีทวีตแล้ว

No internet? No problem.

Bala just dropped the ultimate cypherpunk demo at the BOSS Summit: From Off-Grid to On-Chain

He literally broadcasted a live Bitcoin transaction using Mesh Radio.

No ISPs, no Wi-Fi, no cellular data.

Just pure radio waves bypassing the traditional internet layer to hit the mempool.

When we say we are building unconfiscatable money for uncertain times, this is exactly what we mean. Mind blown.

Here is the repo used to connect meshtastic to bitcoin core:github.com/BTCtoolshed/Me…

English

CHILANG-X รีทวีตแล้ว

彻底炸裂!宏观大神杰夫·布斯直接抛出了宏观经济的终极底牌🔥

他当着全世界的面无情撕下了全球 900 万亿美元资产的遮羞布

在这看似繁荣的数字下面全都是高达 600 万亿的破产烂账

传统的法币债务体系早就已经在实质上灰飞烟灭了

各国政府为了苟延残喘只能通过无限印钞来强行续命

但布斯极其冷酷地指出大饼根本不属于这个腐朽的旧系统

它是人类历史上唯一被纯粹物理能量锚定的去中心化协议

当这套无懈可击的系统对全球 900 万亿资产重新定价时会怎样?

他直接甩出了一笔足以让所有宏观交易员头皮发麻的数学账

单枚大饼的终极购买力将极其恐怖地狂飙至 4300 万美元

更让人窒息的是在这个史诗级的财富转移过程中

伴随着 AI 大爆炸以及开源机器人技术的全面狂暴普及

当智能机械臂等自动化工具彻底接管自由市场和廉价生产力

人类世界所有的商品和服务价格都将被永远且疯狂地打下去

到那个时候你手里哪怕只握着极其微小的一点点比特币碎片

都绝对足以让你在这场维度的技术大爆发中永远实现财富自由

这不是会不会发生的科幻狂想而是已经进入读秒阶段的历史必然

死死拿住手里的数字黄金准备迎接这场史诗级的阶层大跃迁吧🚀

比特币橙子Trader@oragnes

以太坊终于不装了:L1 守老巢,L2 去抢天下! 以太坊这次把话说得很明白。 L1 和 L2 不是谁替代谁。 也不是 L2 只是给 L1 打工的扩容工具。 现在的新分工就是: L1 守核心。 L2 抢增量。 这不是技术细节更新。 这是路线重写。 1、L2 早就不是“便宜版以太坊”了。 前几年,L2 的任务很简单: 帮以太坊扩容。 但现在早就不是这回事了。 很多 L2 要的,不只是更便宜。 它们要自己的用户。 自己的经济系统。 自己的排序权。 自己的商业模式。 自己的市场打法。 所以这次等于正式承认: L2 现在不只是扩容工具。 L2 本身就是增长引擎。 它们要负责创新。 负责差异化。 负责把以太坊带去 L1 做不了的地方。 2、L1 的定位:别什么都想做,你就老老实实当核心。 以太坊这次最清醒的一点,就是不再做“一条链包打天下”的梦。 就算未来 L1 再扩 1000 倍, 一条链也不可能吃下全球所有链上需求。 因为很多东西,L1 天生就不适合做。 更低延迟。 更强定制。 更重隐私。 非 EVM。 特定业务的合规框架。 特定市场的打法。 这些东西,全塞进 L1,没必要,也做不好。 所以 L1 的角色很清楚: 全球结算。 共享流动性。 DeFi 核心。 最强安全。 最强去中心化。 最强抗审查。 一句话: L1 不负责花活。 L1 负责当根。 3、最关键的变化,是 L2 各自做大这件事,被正式合法化了。 以前很多人总觉得, 你既然是以太坊 L2, 那你是不是就该尽量像以太坊? 越像越正统。 现在答案很清楚:不是。 想和 L1 绑得最紧的,可以继续往那个方向走。 同步可组合性、完全互操作、共享流动性、原生 Rollup,这些都可以追。 但这不是唯一答案。 有的 L2 就是要走自己的路。 有自己的商业模式。 有自己的技术强项。 有自己的控制需求。 也行。 前提就一个: 把自己的安全属性讲清楚。 继承了以太坊什么。 没继承什么。 别装。 这其实就是在说: 你们尽管去卷。 卷产品,卷体验,卷市场。 但别脱离以太坊这个中心。 4、说穿了,以太坊现在已经接受现实了:多链时代赢不了,那就去当多链时代的中心。 以前很多公链都想做唯一。 做终局。 做全部。 以太坊现在不这么想了。 它接受了多链会长期存在。 接受了不同链有不同需求。 接受了你不可能把所有执行、所有产品、所有规则都塞进一条链。 那怎么办? 不去做唯一。 去做中心。 让 ETH 继续是最重要的资产锚。 让 L1 继续是最重要的结算层。 让流动性、资产、安全性、开发者心智,继续往这个中心聚。 所以现在真正要保住的,不是“所有东西都回到 L1”。 而是: 不管生态怎么分化,重心必须还在以太坊。 5、这才是以太坊现在最清醒的地方。 不是靠一条 L1 把所有事情都做完。 不是靠压死 L2。 不是靠让所有人都乖乖当附庸。 而是: L1 把安全、结算、流动性、去中心化做到极致。 L2 把产品、创新、控制权狠狠干到极致。 最后让价值继续往以太坊这个中心回流。 如果这条路走通, 以太坊最后赢的方式,可能不是“所有人都在 L1 上”。 而是: 所有人都绕不开以太坊。 这才像终局。

中文

CHILANG-X รีทวีตแล้ว

🚨 深度警告:比特币的下一个周期底部,看价格没用!

请听好:现在唯一重要的事情不是价格,而是“时间”。

1. 扩张与收缩的周期律

比特币的每个周期都遵循相同的结构:35 个周期的扩张 + 12 个周期的收缩。

2015–2017/2018-2021: 扩张阶段(上涨)。

2018/2022: 收缩阶段(回调)。

现状: 扩张阶段已正式结束,收缩阶段才刚刚开始。

2. 时间窗口:底部在 2026 年下半年

从历史顶部到底部的时间跨度通常在 360 到 400 天 之间。

预测: 真正的历史级底部概率最高出现在 2026 年 7 月至 11 月。

3. 两个“买入准则”(满足其一即扣动扳机):

价格触发: 只要价格跌破 $50,000,无论何时,无脑买入。

时间触发: 到达 2026 年 7 月-11 月 窗口期,无论价格,无脑买入。

4. 缺失的终极信号:NUPL(净未实现盈亏)

目前 NUPL 指标尚未进入“蓝色区域”(深度恐惧/价值区)。历史上的每一次大底(2018、新冠、2022)都必须在这个信号出现后才成型。

中文

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

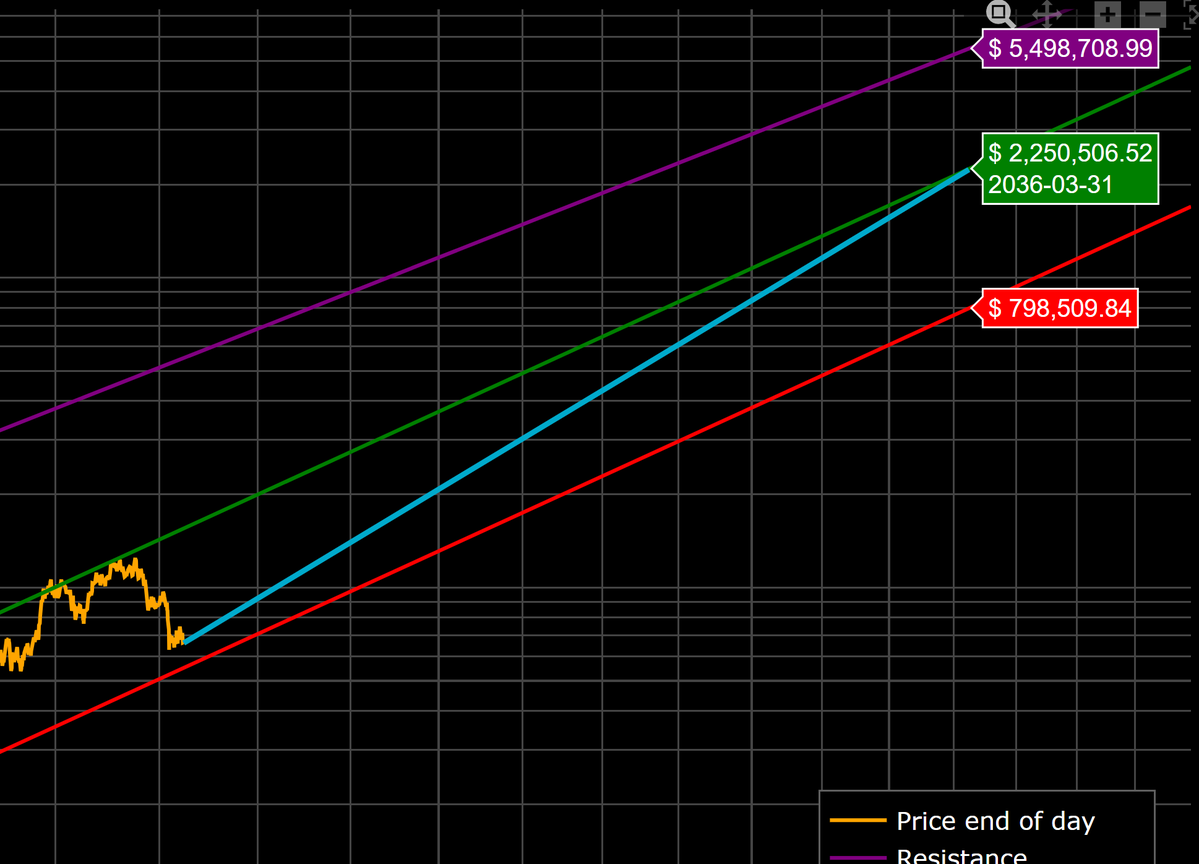

MSTR 10 Years from Now = $5,000 per share... with zero additional Bitcoin purchases?

...and ZERO blow-off top Bitcoin bull runs?

Bitcoin price is converging to power law.

And Strategy under a Bitcoin power law future looks like a financial crime scene for anyone still pretending this is “just leverage.”

Run the CEBE math.

Using roughly 762,099 BTC, about $8.254B of debt, about $10.009B of preferreds, and $2.25B of cash, then dropping that into a March 2036 Bitcoin price of about $2.245M, senior claims barely even register in BTC terms.

You are talking about roughly 0.002205 BTC of CEBE per share, which translates to about $4,951 per share of common equity Bitcoin exposure.

That is before the market adds any premium for the fact that this thing would be the largest publicly traded Bitcoin war machine on earth.

Now zoom out and enjoy the absurdity.

At $2.245M per BTC, Bitcoin’s network value would be about $47.15 trillion.

Against a $900 trillion global wealth base, that implies Bitcoin would have captured roughly 5.24% of all global wealth.

Strategy’s own Bitcoin pile alone would be worth about $1.71 trillion, or roughly 0.19% of global wealth parked inside one corporate treasury. One company. One balance sheet.

One giant orange vacuum cleaner pointed directly at the monetary order.

So yes, the bear case in this scenario is basically: “I understand exponential monetization, I just prefer poverty with a CFA vocabulary.”

People still analyzing Strategy like it is a normal equity are studying the blast radius while standing at ground zero.

If Bitcoin keeps climbing the power law channel, Strategy common stock is a claim on a machine that is slowly converting boardroom cowardice into shareholder thermonuclear upside.

At some point the conversation stops being “is MSTR overvalued?”

At some point the conversation becomes:

“How did one deranged software company end up custodying a meaningful fraction of human wealth while the experts were on television discussing valuation discipline?”

Bull markets make people rich.

Bitcoin treasury companies make accountants look like civilians.

And Strategy, in this future, is what happens when capital markets accidentally summon a sovereign black hole with an investor relations page.

English

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

超级干货!这绝对是有史以来对微策略(MSTR)运行机制最精彩的解读!

这是一份来自Mark Moss 的长达10分钟的深度解析,强烈建议收藏起来慢慢看!

如果你到现在还认为迈克尔·塞勒(Michael Saylor)只是个“靠借钱炒币的疯子”,那你正在错过这个时代最大的财富认知差!华尔街那些拿着传统市盈率(PE)去给微策略估值的精英,简直错得离谱。

这段视频直接把微策略底层的“无限循环”逻辑扒得干干净净。这根本不是什么炒股,这是一台吞噬全球流动性的“合法印钞机”!核心底牌就三张:

1️⃣ 拥有“不死之身”的债务护城河外面天天有人意淫大饼跌破3万塞勒就会爆仓?

纯属外行瞎操心!视频里一针见血:他的巨额债务没有抵押任何比特币,而且债主无权要求提前还款。只要比特币不彻底归零,他光靠账上的现金就能稳如老狗,绝不可能被迫平仓!

2️⃣ 左脚踩右脚的“飞升阳谋”买 MSTR 股票,买的根本不是公司业绩,而是它不断膨胀的“每股含币量”。

只要市场愿意给哪怕 1.2 倍的市净率(PB)溢价,塞勒就敢反手增发股票去疯狂扫货大饼。只要顶着溢价买入,股东的价值就在被无限增厚!这就是完全摆在台面上的无解阳谋。

3️⃣ 向 350 万亿传统老钱“终极吸血”这是全片最让人头皮发麻的王炸!

他们竟然推出了年化高达 11.5%、净值死死锚定的固收产品(STRC)。塞勒直接化身“加密银行”,用极高的稳健利息,把全球 350 万亿固收市场(尤其是那些承受不起股市崩盘的婴儿潮老钱)疯狂吸进大饼的池子里!他拿大饼的高波动去赚取超额暴利,付给老钱固定利息,剩下的天量差价全进自己腰包!

当传统金融还在嘲笑加密货币没有基本面时,微策略早就跳出三界外,变成了一个深不见底的“流动性黑洞”。

比特币橙子Trader@oragnes

AI 下一波最赚钱的方向,居然藏在最难用的企业软件里! AI 最大的赚钱机会,可能根本不在那些最炫的新产品里。 不在语音 Agent。 不在花哨 demo。 也不在“又一个更强模型”。 真正的大机会,反而在最土、最重、最难用、最没人想碰的软件里。 SAP。 Salesforce。 ServiceNow。 这些东西难用得要命。 但全世界的大公司,到今天还得靠它们活着。 1、 很多人不理解,为什么这些系统这么烂,还没人干掉它们。 因为它们不是普通软件。 它们是企业的内脏。 SAP 管钱、库存、采购、生产。 Salesforce 管客户、销售、收入。 ServiceNow 管内部流程、工单、运维。 它们不只是存数据。 还把一家公司这些年怎么审批、怎么记账、怎么分权、怎么合规,全都埋在里面了。 所以换掉它们,不是换个 App。 是把一家公司的流程、权限、报表、接口、组织记忆,整套搬家。 这就是为什么大家天天骂,最后还是不敢动。 2、 而且这东西不是“有点贵”。 是真贵。 企业从 SAP ECC 升级到 S/4HANA,可能要花 7 亿美元,搞 3 年,还得拉一支几十人的咨询团队。 你看到这个数字,就该明白了: 企业软件最大的问题,从来不是能不能升级。 而是谁敢升级。 因为一动,钱先烧。 时间先拖。 业务先抖。 所以这些系统虽然难用,但地位反而更稳。 不是因为它们好。 是因为替换成本太高。 3、 机会也就在这里。 我越来越不信那种“AI 会直接替掉这些老系统”的说法。 真正会发生的,是在它们上面,重新长出一层新的操作层。 底层系统还在。 但正脸慢慢消失。 以后真正的入口,不再是 SAP 那些事务码,不再是 Salesforce 那些烂页面,不再是 ServiceNow 那些埋得很深的流程。 入口会变成一句话: 你说你想干什么。 系统替你去跑。 这才是 AI 真正改企业软件的方式。 不是重做底层。 是重做人和系统之间那层接口。 4、 这件事最先爆发的地方,是实施和迁移。 企业数字化转型为什么总超预算、总延期、总一地鸡毛? 因为实施本来就是脏活。 一堆会议纪要。 一堆老文档。 一堆历史工单。 一堆没人讲得清的流程和字段。 最后全得翻译成系统能执行的东西。 这里最烧钱。 也最容易出错。 AI 一进来,最直接的价值就是: 把零碎信息变成结构化需求。 把流程映射、配置、测试脚本、迁移文档这些重复活自动化。 把原来只能靠人肉补的知识,拎成真正能复用的东西。 这不是提一点效率。 这是直接帮企业少烧几个月时间、少烧几千万预算。 5、 第二块更大的钱,在日常使用。 因为企业里大量“工作”,其实根本不是工作。 是系统摩擦。 找字段。 跑报表。 跨系统抄数据。 改状态。 走审批。 在十几个页面之间来回跳。 员工不是在创造价值。 是在跟烂界面搏斗。 所以 AI 在企业里最值钱的,不是回答你几个问题。 是给这些老系统上面,搭一个真能执行动作的副驾驶。 你不用记事务码。 不用记哪个字段在哪。 不用记哪个流程埋在哪个菜单里。 你只说你要干什么。 系统帮你查。 帮你串。 帮你执行。 这一下,企业软件的使用方式就变了。 6、 更值钱的是,很多企业系统根本没有好用的 API。 很多关键流程,还卡在各种古老客户端、虚拟桌面、老后台里。 所以真正能打进深水区的,不只是会接 API。 还得有能直接操作电脑界面的 Agent。 这才是最贵的那块。 因为企业里最烦、最费人、最适合外包的工作,往往就在这里: 工单分拣。 期末结算。 客户状态更新。 价格调整。 各种长尾流程。 谁能把这些原来只能靠人手点来点去的动作,变成可治理、可审计的自动化,谁就不是在做小工具。 谁是在直接抢外包的钱,抢低效流程的钱。 7、 所以我现在看这件事,逻辑很简单。 世界未来很长时间里,还是会继续靠 SAP、Salesforce、ServiceNow 这些东西运转。 但真正工作的入口,会慢慢换掉。 以后值钱的,不是那个最会卖老系统 license 的人。 也不是那个最会堆咨询团队的人。 而是那个能在这些老系统上面,搭出新操作层的人。 谁能让人少碰烂界面。 谁能让人少切页面。 谁能让人少记流程。 谁能把一句“我要完成什么”,直接翻译成系统里的可执行动作。 谁就能吃到 AI 在企业里最肥的那块钱。

中文

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

CHILANG-X รีทวีตแล้ว

This will be big

Teslaconomics@Teslaconomics

I don’t think people truly understand what’s about to happen with 𝕏 Money. This is Elon going back to his roots - back to x.com - and building what he always wanted in the first place: one place that runs your entire financial life. When he rebranded Twitter to 𝕏 in 2023, he said straight up that we’re adding the ability to conduct your entire financial world. He even said you may not even need a traditional bank account. Most people brushed that off. And now it’s becoming real. 𝕏 Money has already been live in closed beta internally within the company. A limited external beta is expected soon, and they’ve already secured money transmitter licenses in over 40 states plus DC. 𝕏 Payments is registered with FinCEN. Visa is officially partnered. You’ll be able to fund your wallet instantly, send peer-to-peer payments, move money to your bank, and eventually use a debit card. And I think this is just the beginning. This will probably start as a simple wallet where you can send money as easily as sending a DM. With this technology, you can pay creators, pay subscriptions, pay whatever bills, shop inside the app, get paid inside the app, and much more. Then, there will be high-yield savings, you can invest, you can get loans, have money market accounts, maybe even treasury access, cool smart cashtags that let you see live stock prices in your timeline and execute trades seamlessly, crypto integration, potentially full asset management… the list goes on and on… Elon literally said this is meant to be the central source of ALL monetary transactions. Bro… think about that for a sec. Your 𝕏 profile becomes your financial identity. Everyone you follow is already there. Everyone you interact with is already there. That social graph becomes your distribution engine. Like, you won’t need a separate banking app, no need for a separate investing app, no need for a separate payment app… this all lives where you already spend your time. Right here on 𝕏. Look at WeChat in China, which Elon always alluded to. Payments, messaging, shopping, investing - all integrated in one app. It handles $ trillions in volume and became deeply embedded in everyone’s daily life. Now 𝕏 is building the Western version of that, but with a more global reach, and xAI’s AI layered on top of all this. Before you call me crazy, you have to understand how big this opportunity is. Digital payments globally are measured in the tens of $ trillions of dollars annually. Even just capturing a small slice of that across hundreds of millions, and eventually a billion, users can change everything. 𝕏 already has the audience. That lowers customer acquisition costs significantly. Add fintech revenue on top of ads, plus float, plus lending, plus investing tools, and we’re talking about a completely different valuation profile. Now, $44B for this company looks like the bargain of the decade… this was one of the main reasons I invested in 𝕏. And if they execute the way they’ve executed at Tesla and SpaceX, this could truly fundamentally redefine how people handle $ . Most people today still see 𝕏 as just a social media app. I see it as the foundation of a financial system layered on top of a global network. Ultimately becoming the “everything” app. And this I believe is a once-in-a-generation opportunity. Elon is calling this a game-changer. I believe him.

English