Kingslayer Capital

118 posts

Kingslayer Capital

@KingslayerCap

Trying to find good stocks.

Sumali Ekim 2025

109 Sinusundan35 Mga Tagasunod

@RebellioMarket Buffett did it for 60 years and is worth $150 billion dollars

English

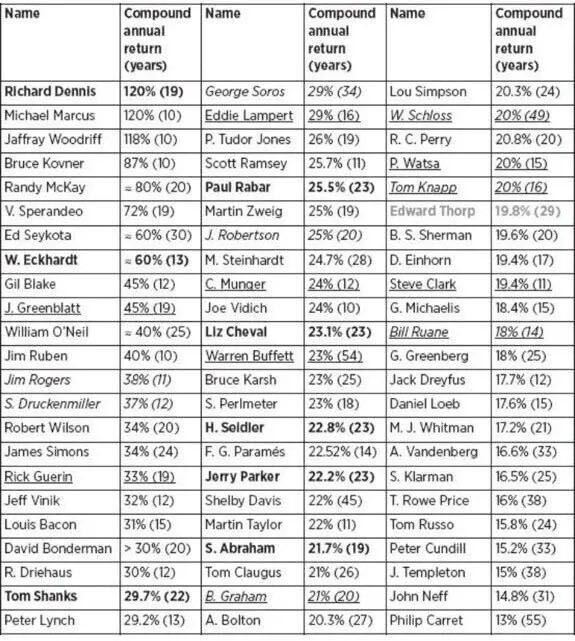

If Warren Buffett is truly the greatest investor of all time how do you explain these numbers?

Michael Marcus: 120% CAGR over 10 years

Richard Dennis: 120% CAGR for 19 years

Bruce Kovner: 87% CAGR over a decade

Ed Seykota: 60% CAGR for 30 years

William O'Neil: 40% CAGR for 25 years

Maybe the real question isn’t who’s the greatest

it’s what strategy truly wins

English

@CompoundinGirl He won't respond to this bc it's exactly right

English

Bill Ackman is clearly one of the great investors of our time. His analytical rigor, willingness to take concentrated positions, and ability to think independently have produced some remarkable investments over the years.

In another universe, he could have been a “Baby Buffett.”

But there is one structural difference that prevents that path: fees.

If your goal is to compound capital for 30, 40, or 50 years and truly do what is best for your investors, it becomes extremely difficult to operate within a traditional fee structure.

This is not really about the amount of the fees themselves. It is about the relationship they create.

Once a manager charges management and performance fees, the incentives inevitably shift. Asset gathering becomes rational. Shorter time horizons creep in. Drawdown sensitivity increases. There is pressure to justify activity, to market performance, to manage optics.

Even if the manager has the best intentions, the structure introduces friction between what is optimal for the investor and what is optimal for the firm.

The beauty of Buffett’s model is that it removed this friction. His wealth compounds alongside his shareholders. No management fees. No incentive fees. Just long-term ownership.

When the manager and the investors are effectively partners, the time horizon can stretch to decades and the decision-making becomes radically simpler.

That alignment is incredibly rare, and it is one of the reasons Berkshire Hathaway is so unique.

Ackman is an exceptional investor. But the structure matters as much as the skill.

@BillAckman please convince me otherwise.

His positions: $BN $UBER $AMZN $GOOG $META $HHH $QSR $CMG $HLT $HTZ $SEG $FNMA $FMCC

Bill Ackman@BillAckman

Today, Pershing Square Inc. (PSI), an alternative asset management company, filed to go public along with Pershing Square USA, Ltd. (PSUS) a new closed ended investment company managed by Pershing Square. In the combined offering, investors in the IPO of PSUS will receive shares in PSI for no additional consideration. For example, if an investor buys 100 shares of PSUS in the IPO, they will receive 20 shares of PSI at no additional cost. I explain the transaction in detail in a letter that can be found here: sec.gov/Archives/edgar… [sec.gov] The prospectus for PSI can be found here: sec.gov/Archives/edgar… [sec.gov] And the prospectus for PSUS can be found here: sec.gov/Archives/edgar… [sec.gov] The PSI and PSUS Registration Statements have not yet become effective. The securities described therein may not be sold, nor may offers to buy be accepted, prior to the time the Registration Statements become effective. Before you invest in the combined offering, you should read the Registration Statements for more complete information about the PSI, PSUS, and the combined offering.

English

@yummyCenturyEgg More like demand pull forward during Covid and normalization of demand thereafter with new (capacity constrained) entrants

English

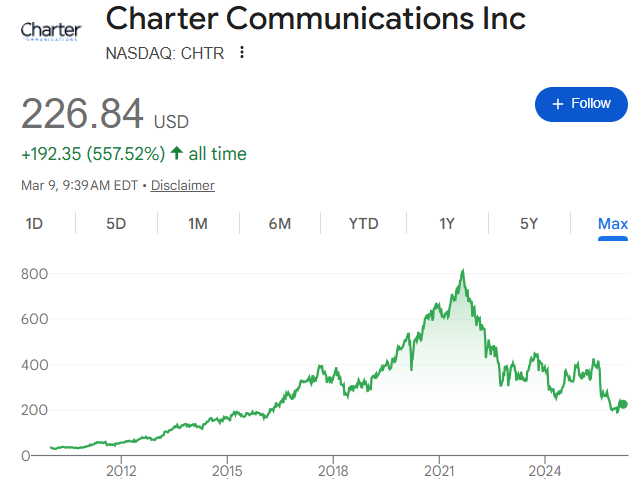

For whom the Bell Curves - $CHTR

"Any man's death diminishes me... never send to know for whom the bell tolls [curves]; it tolls [curves] for thee." - John Donne.

If there were an Olympics for compounders, $CHTR would medal in just about every event: solid moat, steady cash flow, strong management, disciplined capital allocation, and aggressive share repurchases. And yet, somehow, the stock still wound up tracing out a bell-curve formation. It's brutal out here.

English

@KingslayerCap Hypothetically yes. Buy low sell high how hard can it be? Easier said than done

English

You guys gotta read this. I know I'm tough on value investors, and some of you might think "well, we're contrarians, so this is exactly what we need to see to buy the dip". But let me tell you, value investing during times of rapid change is NOT a robust strategy. We've seen this unfolding in the last 10 years...the next 10 years will happen at a much quicker pace. Value investing is dependent on things reverting to the mean, which is not the case during periods of change. In the next 10 years, when every facet of the competitive landscape is touched by AI, you can't just buy cheap. Compounders are even more at risk, because their stock prices are not reflecting this potential for change. Again, some of you might think I'm just a hater, but I like to think I've just internalized the lessons over the last 10 years and projected them forward. For value investing to work, you need to make a coherent case for why things are not going to change. And this coherent case can't just be "we have a margin of safety". Stop looking at the stock chart and valuation tables, and start mapping out all the AI startups that are operating in your industries. @MrMojoRisinX you should expand on this series and write a book on it. I think it's a very worthwhile endeavor.

Mojo@MrMojoRisinX

New Post! Ben Graham Was Wrong And He Would Have Been The First To Admit It $VALU.Q see bio and next post

English

Enjoyed listening to Gavin on a non AI podcast. I am jealous at how much smarter he always says things that I agree with completely. And I am definitely stealing the theory that ages 50-70 are the peak of investment powers.

Gavin Baker@GavinSBaker

Fun to do this with my friend @tseides Minimal discussion of AI; much more of a focus on investing. Background, philosophy, process, etc. youtu.be/CFtlGhmAeM0?si…

English

@rhunterh $CHTR's FCF profile is such that you don't need to believe in terminal value for the stock to work

English

Terminal value of 99% of companies is ~$0, the terminal value in a DCF is a statement of belief about how quickly it gets there. In the full course of time every business is a declining annuity.

Long Equity@long_equity

Sometimes compounders stop compounding. What lesson do you take away from this?

English

@ohcapideas I like Greg but he is an operator and it is a bit concerning to that is managing the other 94%

English

Have to admit I’d be a little insulted to be Weschler, the only remaining portfolio manager, and to only have responsibility for 6% of the investment portfolio. I’m sure he plays a broader consulting role, but Berkshire probably needs to institutionalize the investment portfolio a little bit more in the future and have a handful of managers for the non semi perm holdings.

English

A very good letter - one you can tell was written by an operator. Things could work out ok for some time optimizing operations and buying back shares. But, that only works if the share price moves lower. With year book value, P/B ~1.52x.

Ohio Capital Ideas@ohcapideas

I’m really hoping Abel improves the disclosures somewhat (today or over time). I’m not sure it’s too much to have an MSR balance sheet and rev/income figures for the ten biggest MSR subs.

English

@LuBtc888 I'm sorry, what? "Not Buffett"..... 90% of Munger's net worth was in berkshire lol

English

查理·芒格把家族的钱交给了谁打理?不是巴菲特,而是一个叫李录的华人。

这个在过去几十年里封神的顶级投资家,低调到全网几乎找不到他哪怕一分钟的公开录像。

直到这段被封存了近20年的“禁片级”哥大内部授课流出。

整整一个半时,没有教你怎么看K线,没有教你怎么追热点。

只用框架与判断力讲透两个字:估值。

真正的大师课,值得反复学习。

芒格的个人的外部家族资产,并没有交给巴菲特去设立基金运作,而是唯独看中了李录。

芒格一生中个人的钱只投了三个地方:伯克希尔(他自己的公司)、好市多(Costco),以及李录的基金。

他还曾在公开场合称呼李录为“中国的巴菲特”。

0x鸣人@LuBtc888

想要成为顶级富豪情商需要有多高? 当记者问查理·芒格:你和巴菲特搭档了那么久,凭什么他比你更有钱? 芒格的回答,给所有自作聪明的人上了一课。

中文

@A_P_Capital I think you'd be hard pressed to find a company with more growth in FCF/share over the next 3 years. Agree leverage will add more volatility but I think crux of thesis is inflection in FCF in 2027/2028

English

@KingslayerCap Yeah. See much more upside in other companies with better growth. It is incredibly cheap but has a huge amount of debt and will be tough to have much pricing power with competition. A lot of companies I had been watching fell recently, so swapped it out.

English

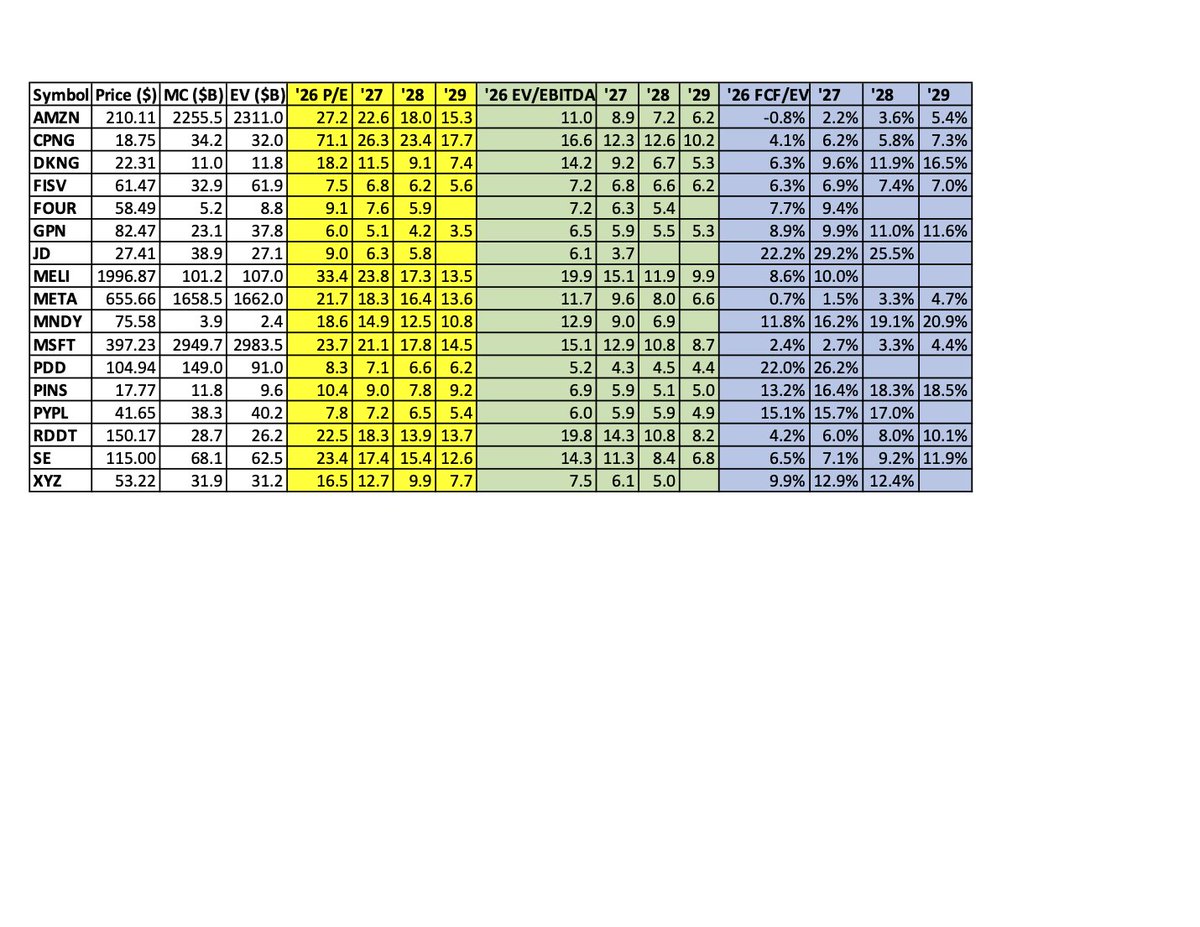

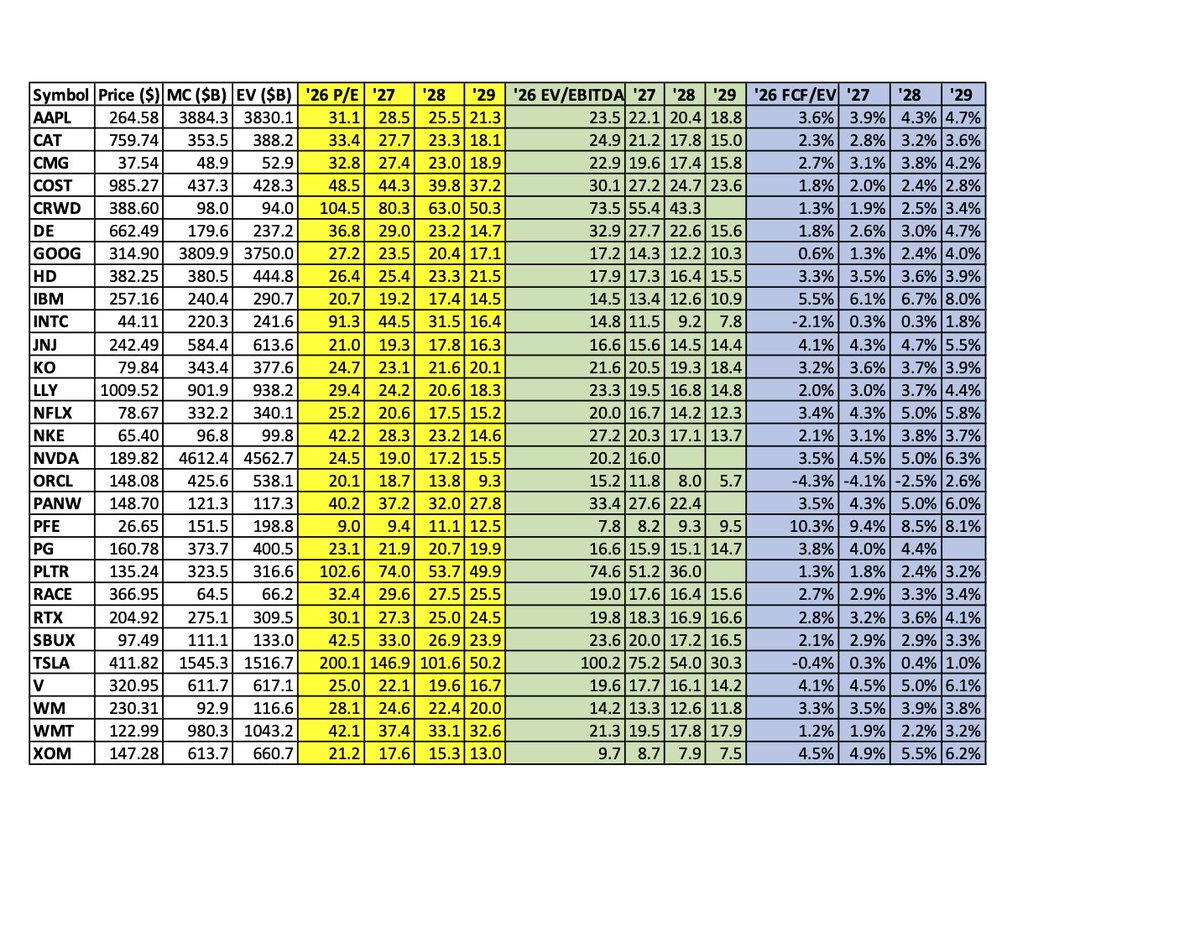

Updated fundamental metrics of my current top picks $AMZN $CPNG $DKNG $FISV $FOUR $GPN $JD $MELI $META $MNDY $MSFT $PDD $PINS $PYPL $RDDT $SE $XYZ and another chart of popular stocks.

English

@michaeljburry @aakashgupta Dubbed Cassandra by Warren Buffett for a reason. Very impressive track record Dr Burry, thank you for sharing your thoughts. We are very appreciative!

English

Well, I have called just about everything significant that has happened the last 26 years.

It's hard to say I've never had the timing right.

I was short Amazon at the top in 2000.

I went way long small cap value in late 2000.

I bought AAPL in 1998 and then again in 2002.

In 2003, I got into Korea stocks before a big run.

In 2004, I got into China stocks before a big run.

In 2004, I got into oil before a big run.

I bought gold in 2005 and still 20 years later...

In summer 2005, I figured I was buying 5 years swaps on something would print within 2, and it did.

In 2008, October, I told my investors it was time to buy. More stocks bottomed then than in March 2009.

In 2009, I invested in Almonds/Water, it worked ok.

In 2013, I moved to buy Bitcoin after meeting with a friend at Lightspeed. I should have. Slept on it and did not.

In 2015, I bought NVDA. The CFO knows.

In 2018, I started pounding the table on Japan and opened a Japan fund, which I had to close for COVID.

In late 2019, I warned indexing and passive investing would make for very corrlated severe drawdowns in the market, and COVID hit 6 months later, we got the most correlatedl, sharp decline in modern history.

Early 2020, I entered 2020 very short. Which worked.

During early COVID I loaded up on stocks and had nearly a 100% year for the fund.

In 2020, I called lockdowns would be disastrous for women and children, and went on Twitter to say it.

IN 2020, I got GME to buy back 1/3 of its stock and change its board. Did ok.

July 2021, I gave Barron's an interview to warn on specific meme stocks at the top, and they crashed through Dec 2023.

2021, I warned about very high inflation from the policies that were being undertaken.

2023, I warned people to sell because I saw the banking crisis coming. I told them all was clear at the bottom in March as I could see it wouldn't be contagious.

2020s, I shorted Tesla, but these were trades, and it was volatile. I did not lose money overall shorting Tesla. Had some really big quick wins. Plus Tesla is only worth about $120.

I am not perfect, I did not hold AAPL or NVDA long enough, in 2025 we were up almost 100% again by Liberation Day, and I lost most of the gain (still up about double digits for the year at closing) but I would put the calls I've made over these decades up against anyone.

I would add visual proof for all this, but it is too much for this medium.

English

Burry is mass-publishing the accounting case for his put options on Nvidia and Palantir while the rest of the market is still debating whether the capex cycle has legs.

The math he’s referencing is specific. The Big Four hyperscalers just guided $650-700 billion in combined 2026 capex, a 60%+ increase from the $381 billion they spent in 2025. Amazon alone committed $200 billion, so far above the $146 billion consensus that the stock lost $450 billion in market cap over nine straight sessions.

Burry’s core thesis is the depreciation trick. Nvidia’s GPU architecture runs on a 3-year cycle, with each generation delivering 2-3x more compute per watt. The H100s shipping today are economically obsolete by 2027. But the hyperscalers are depreciating them over 5-6 years. Burry estimates this gap understates depreciation by $176 billion between 2026 and 2028, inflating reported operating income by 20%+ at companies like Oracle and Meta.

That’s the “accounting tricks” he’s referencing in the tweet. He did the math.

The cash flow picture backs him up. Amazon is projected to go negative FCF in 2026, somewhere between -$17 billion (Morgan Stanley) and -$28 billion (BofA). Alphabet’s free cash flow is expected to collapse 90%, from $73.3 billion to $8.2 billion. The Big Five raised $108 billion in bonds in 2025 alone, more than 3x the average of the prior nine years. JP Morgan projects $1.5 trillion in tech debt issuance ahead. They’re repackaging data center debt as asset-backed securities, $13.3 billion this year, a structure with a history that includes Enron and 2008.

The depreciation cliff is the part the market hasn’t priced. The five hyperscalers plan to add $2 trillion in AI-related assets by 2030. At 20% annual depreciation, that’s $400 billion per year, which exceeds their combined 2025 profits. And AI services currently generate roughly $25 billion in direct revenue against $650 billion in infrastructure spend. Four cents per dollar invested.

But here’s where you have to be careful with Burry. He shorted Tesla at $180. It went to $1,200. He called the housing crisis two years early and nearly went bankrupt waiting for the trade to work. He bought puts on Nvidia and Palantir, capped-downside bets, because even he knows his timing is unreliable.

The pattern with Burry is always the same: the structural analysis is correct, the timing is wrong, and the market can stay irrational long enough to wipe out the trade before it pays. He sees the depreciation cliff. He sees the accounting inflation. He sees the debt structures. All of that is real.

The question is whether AI revenue scales fast enough to fill the gap before the write-downs hit.

AWS alone runs at $142 billion annualized, growing 24%, with a $244 billion backlog. Google Cloud’s backlog surged 55% to $240 billion. These companies are monetizing capacity as fast as they install it.

Burry is building the bear case in public so the crowd does the work for him. That’s the trade. Whether it pays depends on something Burry has never been good at: timing the moment when the music stops.

Cassandra Unchained@michaeljburry

A question I have for $ORCL, $GOOG, $META, $MSFT, $AMZN, $NVDA, $CAT, and all the rest, “When does the spending for AI data center buildout actually end?” It is consuming all your cash flow, you are borrowing, you are financing in ways you never have, apparently because it is so urgent, because it scales? But if it scales, when does it end? Now you are engaging in accounting tricks to hide expense, to protect earnings, as the impact is so severe. You will be tortuously adjusting your earnings in a new and sinister ways. When does it end?

English

@adamkhootrader Asset sale is a bit of smoke and mirrors.

1) they sold their best assets. All 1L floating rate debt at low LTV. The unsecured, 2L, pref, equity positions are likely where issues are (ie what they didn't sell)

2) they sold to kuvare, whose assets are managed by....OWL

English

Why the BDC Selloff Is a Narrative Problem, Not a Fundamental One. $OBDC

There's been a lot of fear around Blue Owl and the BDC space this week. I want to cut through the noise for our community.

OBDC II — a private, non-traded fund — stopped quarterly redemptions. The media called it a crisis. But the reality is much simpler: this was a mature fund reaching its end of life, and investors were redeeming at full NAV to buy the same loans on the public market at a 20% discount. It was an arbitrage play, not a run on bad credit.

Blue Owl's response actually proved the loan book is rock solid — they sold $1.4B of loans at 99.7% of par to major pension funds, with demand far exceeding supply.

OBDC's fundamentals remain strong: non-accruals fell to 1.1%, portfolio companies are growing revenue and EBITDA, Moody's upgraded the credit rating, and management just executed their largest-ever buyback.

Don't let headlines shake you out of quality positions. This selloff is an opportunity, not a warning.

English

@chamath Lesson one: be early employee at Facebook

Lesson two: act like that makes you an authority on everything else

English

Launching a YouTube channel to share business stories, lessons I've learned, and important topics I’m actively exploring…

youtu.be/0-LAT4HjWPo

YouTube

English

@DDInvesting @OctusCredit I'm not saying they will although I'm sure some will.

I'm saying you have to accurately weigh the expected value. If there's a 80% chance you get paid par and 20% chance you recover 70c, that's a lot different than 80% chance of par and 20% chance of zero

English

My take: The Blue Owl news is retail media fear mongering.

My credentials: I started and run the leading information and data provider on all things credit (@OctusCredit). I’ve been involved or have knowledge of most major bankruptcies since Enron.

Companies file for bankruptcy or go insolvent for three reasons: 1) they run out of money (ie. Revlon) 2) fraud (Worldcom) 3) capital structure management (everything else)

Software companies will not run out of cash. They are negative working capital businesses with negligible physical capex (software spend is capitalized albeit an analyst will adjust for that). The worst software companies will have gross retention ~ 90% and net retention 95-100%. That means the theta decay on annual recurring revenue (ARR) is single digits. Further a software company can manage expenses to further improve margins in a declining revenue environment to increase EBITDA and cash flow

Fraud…I posit negligible risk. Most private credit backing software deals are the leverage in an LBO backed by a sponsor. As a CEO that has done multiple recaps with multiple sponsors, the financial diligence (QoE and beyond) is intense. Further its very hard to obfuscate financials of software companies given the cash flow nature of the business

Which leads me to capital structure management. Very very few of these deals have meaningful financial covenants. Yes many will have a leverage covenant but the covenant itself is so high with so many addbacks its nearly impossible to breach outside of a cataclysmic drop in EBITDA (which Ive already explained is difficult for software cos). So nothing is bringing these companies to the table to effectuate a liability management exercise.

Further, and importantly the private credit lender and sponsor relationship is a unique one. A lender wants to have a positive relationship with a sponsor so the sponsor will continue to show them their deals. The fees for doing a private credit deal are substantial and quick and being shut out of a Tier 1 or Tier 2 PE deal would be bad for business. So the private credit fund will usually work in collaboration with the private equity fund to insure steady waters (you’ve seen this with PIKing many deals the past 18 months)

In addition, private credit and leverage is only a portion of the cap stack. Given the multiples over the past 5 years for SaaS companies there is a substantial amount of equity underneath the debt stack even in a unitranche. And not small equity checks. Equity checks in the billions that PE funds will do whatever they can to keep the keys to preserve their franchise and fund economics.

A quick point about the gates going up at Blue Owl. For the last two years Ive been telling people private credit will have its BREIT moment. That’s not a ding on the asset class, more of a point in time when the liquid marketplace for the asset hasn’t YET developed to maturity. This has happened for effectively every major asset class in the history of finance and banking. It is not new. It is simply the growing pains a scaled asset class transcends with time. In a couple years this market will be more liquid.

So in summary:

1) lots of cash flow

2) negligible risk of fraud

3) big equity cushions

As I look into the market, this may be a once in a generation time to buy incredible assets that are trading at historically low multiples because of an AI narrative that throws the baby out with the bath water.

English

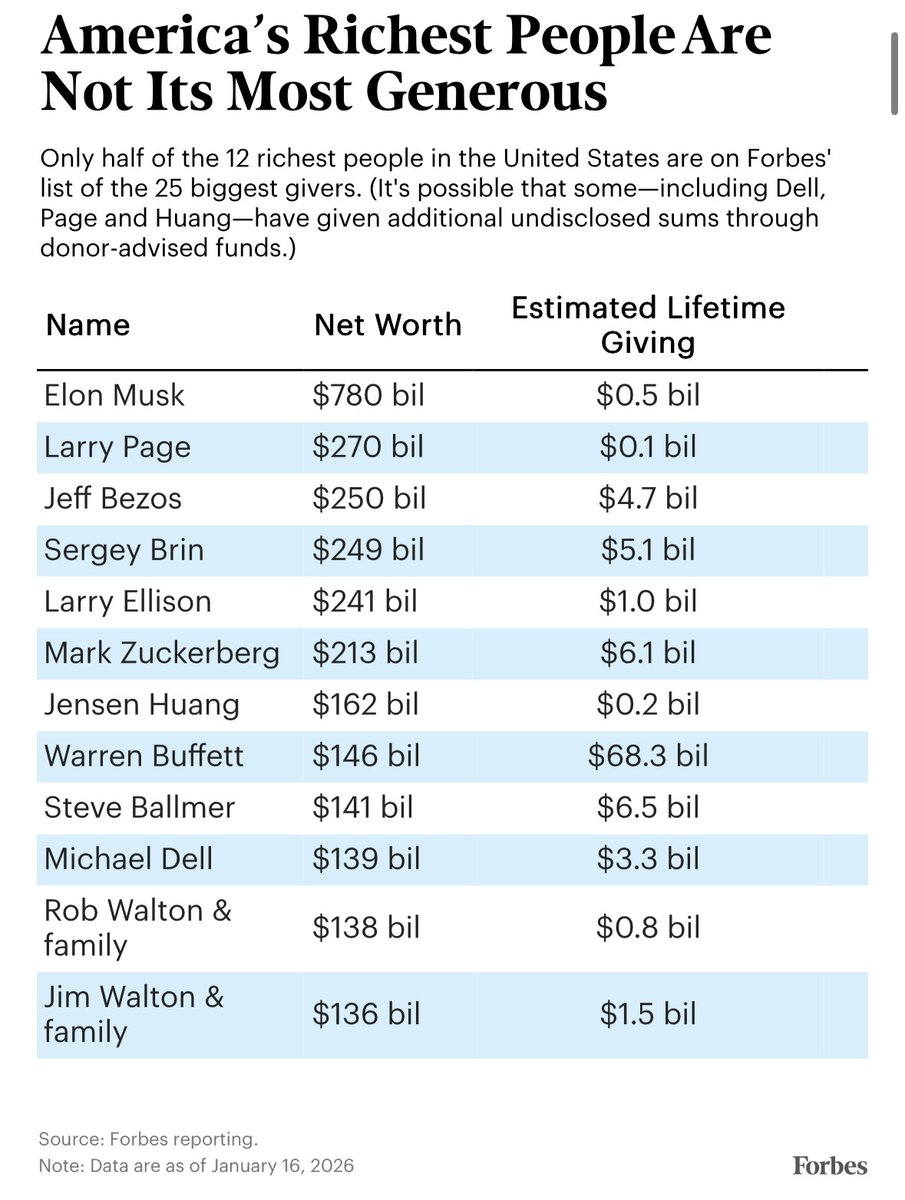

@TheRealJChubby To state the obvious, the wealth is tied up in stock which they need to be able to control their companies. It's not cash sitting in a bank account.

Not saying these are necessarily good people but it's a bit of an unfair dig imo

English

This is why we just have to take it from them.

English