Naka-pin na Tweet

I just took a position in CCXI, Churchill Capital Corp XI and here's why (Save this).

CCXI is a SPAC that on June 24 announced a definitive merger with Agility Robotics valuing the company at $2.5 billion pre money with over $620 million in gross proceeds to fund scale.

When the deal closes, shareholder vote expected the week of August 19, CCXI becomes AGLT, the first and only US listed pure play humanoid robotics company with active commercial deployments.

Every other humanoid company worth owning is either private, Figure AI, Physical Intelligence, 1X or buried inside a conglomerate where humanoid robots are a footnote.

When the whole retail world wants a trade and there is exactly one liquid way to express it, scarcity alone is a thesis but Agility is the real thing.

Digit has logged more than 65,000 hours of actual work across nine customer sites, with over $300 million in multi-year orders already signed for Digit v5.

Paying customers include GXO, Schaeffler, Toyota Manufacturing Canada, and Mercado Libre with Amazon actively testing.

The job Agility picked matters too, Digit was built for one boring, monetizable task moving things around warehouses.

Figure AI, at a roughly $39 billion private mark, is chasing general-purpose everything with no paying customers yet while Agility earns money first and needs a miracle second.

Nvidia named Agility the launch partner for its Halos physical-AI safety system, the same level of designation Jensen gave Nebius in the neocloud world that means preferential chip access, co-development resources, and a direct seat at the table for whatever physical AI looks like next.

Now look at where this market is going.

Goldman Sachs projects 1.4 million units shipped annually by 2035, Morgan Stanley puts the total ecosystem at $5 trillion by 2050 and Citigroup sees 648 million deployed humanoids by mid-century.

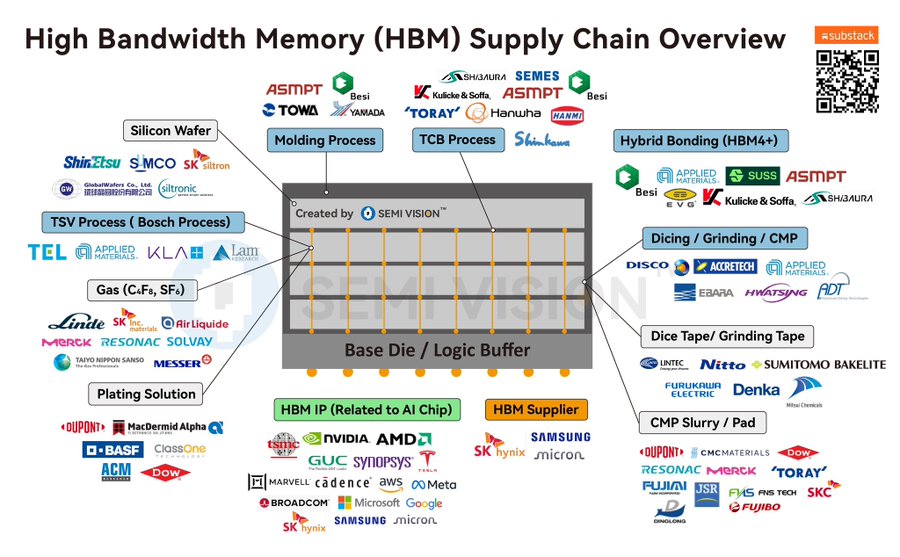

The image above shows 30+ named robot makers spanning China, the US, Germany, and beyond but almost none of them are publicly investable as clean pure-plays.

CCXI gives you that clean pure-play today, at a $2.5 billion valuation, for a company already generating commercial revenue, already deployed in live industrial settings, and about to receive $620 million in fresh capital to scale production.

CCXI is the only place where the entire humanoid map collapses into a single liquid ticker and where buying the maker pulls every supplier on that map up with it.

The shareholder vote closes by August 19. The S-4 drops in July with full financials and the window is narrow and that is exactly why I took the position now.

Make sure to follow me @MelvinInvests for more overlooked opportunities in robotics and AI.

Want my full breakdown of CCXI and every humanoid supply chain play we're tracking in the Milk Road portfolio?

You can come join Milk road Pro for just a dollar using the link below!

English