Naka-pin na Tweet

Rod Lowe

4.2K posts

Rod Lowe

@RodloweLowe

Fund Manager AG Capital Value Flexible fund; Director of Value Asset Management (Pty.) Ltd. ; Elliottwave chartist, father of 3 ; tweets are not advice.

Cape Town Sumali Mart 2014

1.5K Sinusundan5.9K Mga Tagasunod

@hazelwood_dave There is a "theory" that Bessant advised Trump to close all 19 US military bases in ME to reduce the cost of military expense on the US budget which is only surpassed by debt interest. Repatriation could come from US agreeing to a surcharge per tanker passing in the Hormuz strait

English

Some Iranian demands in negotiations could be a problem though. Complete US withdrawal? Reparations? Those are non-starters.

Open Source Intel@Osint613

BREAKING 🔴 WSJ: Iran’s Revolutionary Guard, responding to mediation efforts, is demanding firm guarantees the war will not restart, a halt to Israeli strikes on Hezbollah, the shutdown of U.S. bases in the Gulf, and compensation for its losses.

English

NIO: said buy at $4.68. Has been to $6.22. Velow detailed research from Jan Dekkers explains why this share has potentially explosive upside over the next 12/24 months. Could be one of the best performers for 2026. My PT is $56 medium term & $100+ longer term. Move over Tesla...

jan dekkers@jan_dekkers

$Nio Owners want to know what their stock would be worth The $60 Billion Question: What #NIO Stock Is Really Worth If Shenji Hits the Big Number Let me cut straight to what every NIO shareholder actually wants to know. You own a stock trading at roughly $6.50 per share. You have watched the company navigate production challenges, margin pressures, and a brutally competitive EV market. And now you are hearing that Shenji, NIO's chip subsidiary, could be valued at $60 billion in an IPO. The question is simple. What happens to your stock? I am going to give you the answer in plain numbers, then walk you through exactly how we get there. No tables. Just the math that matters. The Simple Answer - If Shenji reaches a $60 billion valuation and NIO maintains its current 62.7 percent stake, your NIO shares would be worth approximately $24 each. That is nearly four times the current price. But before you get too excited, let me be very clear about what has to happen for that number to become reality. The $24 price tag is not automatic. It depends entirely on whether Shenji can generate the earnings required to justify that valuation in the eyes of public market investors. How the Math Works - NIO currently owns 62.7 percent of Shenji. That is a controlling stake, which means NIO consolidates Shenji's financial results but also captures the full upside of the subsidiary's value. If Shenji is valued at $60 billion in an IPO or a funding round, NIO's stake alone is worth $37.6 billion. Now add NIO's core electric vehicle business. Today, the market values that business at roughly $12 to $13 billion. That is what investors are willing to pay for NIO's car sales, battery swapping network, and brand presence in China. Combine the two, and you get a total market capitalization of approximately $50 billion. Divide that by NIO's 2.1 billion shares outstanding, and you land at roughly $24 per share. This is the arithmetic that has NIO shareholders watching Shenji's every move. The Earnings Reality Behind the $60 Billion Number Here is where the conversation gets serious. A $60 billion valuation is not just a number pulled from thin air. In the semiconductor industry, valuations are anchored to earnings. The multiple the market assigns to those earnings tells you how much growth investors expect. Let me give you three real-world examples using actual semiconductor companies. ON Semiconductor trades at 226 times earnings. If Shenji commanded that multiple, it would need to generate approximately $265 million in annual net income to support a $60 billion valuation. Intel trades at 91 times forward earnings. At that multiple, Shenji would need roughly $659 million in net income. KLA Corporation trades at 37 times earnings. At that multiple, Shenji would need $1.62 billion in net income. Each of these scenarios produces the same $60 billion valuation. But they imply vastly different levels of earnings power. The question for NIO shareholders is not whether Shenji can hit a $60 billion headline number. It is whether Shenji can generate the earnings that make that number credible. Where Shenji Stands Today - To understand whether those earnings targets are achievable, you need to know where Shenji is right now. The subsidiary recently completed an external funding round that valued it at approximately $1.5 billion. It has already shipped more than 150,000 of its NX9031 chips to NIO vehicles, plus over 400,000 Yangjian LiDAR chips. The NX9031 is the world's first 5-nanometer automotive-grade intelligent driving chip, delivering four times the computing power of NVIDIA's Orin-X. Shenji is already generating licensing revenue in the hundreds of millions of yuan from intellectual property agreements. And later this year, the company will launch its M97 chip, targeting 700 TOPS of computing power and actively pursuing external customers like Leapmotor and Geely. Current revenue run rate is roughly $250 to $300 million. At semiconductor gross margins of 50 to 60 percent, and net margins potentially reaching 20 to 40 percent at scale, Shenji's current earnings power is likely in the range of $50 to $100 million annually. To hit the $265 million net income target required for the ON Semi multiple scenario, Shenji needs to roughly triple to quintuple its earnings. To hit the $659 million target for the Intel multiple scenario, it needs to grow earnings six to twelve times. And to hit the $1.62 billion target for the KLA scenario, it needs earnings growth of sixteen to thirty-two times. The lower end of that range is challenging but achievable with aggressive external customer growth. The upper end requires Shenji to become a dominant player across automotive AI chips, robotics, and agent-based inference applications. What Actually Moves the Stock If you are a NIO shareholder, you should ignore the headline $60 billion speculation and focus on three specific catalysts that will determine whether that number becomes real. The first is external customer announcements. Shenji currently sells almost exclusively to NIO. The market will not assign a premium multiple until the company proves it can win business from other automakers. The M97 chip launch in the third quarter of 2026 is the moment to watch. If Shenji announces binding contracts with Leapmotor, Geely, or other major manufacturers, the narrative shifts from captive supplier to independent AI chip company. That narrative shift is what drives multiple expansion. The second is earnings growth. Forget the valuation for a moment. Watch the quarterly numbers. If Shenji can demonstrate consistent revenue growth, improving margins, and expanding external revenue share, the market will reward that progress regardless of the current multiple. Earnings are what ultimately support valuations. The third is NIO's core business. This is the part that many investors overlook. Even if Shenji succeeds spectacularly, NIO's consolidated financials still include the electric vehicle business. NIO posted its first profitable quarter in Q4 2025, but operating margins remain negative and the company still carries significant debt. If the core EV business deteriorates, it could drag down the entire company regardless of Shenji's performance. The Bear Case You Need to Consider - I have walked you through the upside. Now let me give you the risks that could keep that $24 price tag out of reach. The first risk is that external deals do not materialize. Shenji is in active discussions with Leapmotor and Geely, but those discussions have not yet resulted in binding contracts. If the M97 chip launches without major external customers, the narrative remains stuck on "captive supplier" and the multiple stays compressed. The second risk is dilution. NIO currently owns 62.7 percent of Shenji, but future funding rounds could reduce that percentage. If Shenji requires additional capital before an IPO, NIO's stake could be diluted below 50 percent, reducing the value that flows through to shareholders. The third risk is competition. Horizon Robotics has long dominated China's automotive AI chip market. While the company dropped its bundling requirement in late 2025, it remains a formidable competitor with established relationships and significant scale. Shenji will have to win market share against an entrenched incumbent. The fourth risk is timing. Even if everything goes right, a Shenji IPO may still be years away. NIO shareholders looking for near-term catalysts may be disappointed if the timeline stretches longer than expected. What Your Stock Is Really Worth Today Let me give you a realistic framework for thinking about NIO's value right now. In the most conservative scenario, where Shenji remains a captive supplier with limited external revenue, the subsidiary is probably worth $2 to $4 billion. That puts NIO's total value in the $14 to $17 billion range, or roughly $7 to $8 per share. This is essentially where the stock trades today. In a moderate scenario, where Shenji lands one or two external customers and demonstrates meaningful earnings growth, the subsidiary could be valued at $10 to $15 billion using semiconductor multiples in the 30 to 50 times earnings range. That gives NIO a total market cap of $22 to $28 billion, or $10.50 to $13.50 per share. In the optimistic scenario that everyone is talking about, where Shenji becomes a legitimate third-party AI chip player with multiple external customers and expanding robotics applications, the subsidiary could reach $40 to $60 billion. That gives NIO a total market cap of $50 to $70 billion, or $24 to $33 per share. The difference between these scenarios is not about luck. It is about whether Shenji can execute on external customer acquisition, scale production, and expand beyond automotive into adjacent markets like robotics and agent-based AI. The Bottom Line for NIO Owners If you own NIO stock, you own a controlling stake in one of the most promising automotive AI chip companies in China. That is the opportunity. But it is also the risk. The market currently values NIO as if Shenji will remain a captive supplier. The upside exists because the market has not yet priced in the potential for external success. Your stock is worth $6.50 today. It could be worth $24 if Shenji delivers on its external growth story. But that outcome depends entirely on execution. Watch the M97 chip launch. Watch the customer announcements. Watch the earnings. The multiples will take care of themselves if the growth is real.

English

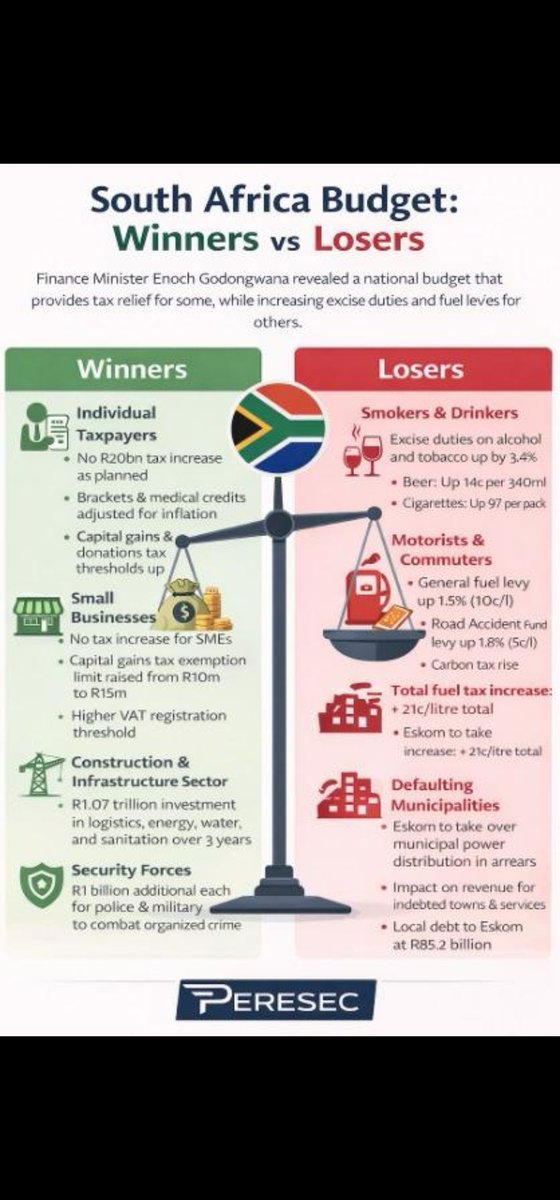

Stefanutti, WBHO, Raubex....Budget speech ann. R1.07 trillion to be spent over next 3 years into infrastructure (logistics, energy, water, sanitation, water treatment, data centres). Constructions shares likely the most under-owned shares currently. Like gold shares 3 years ago.

English

NIO: touched $5.40 last night in NY on what looks like a "breakout" & attempt to regain 200 dma. Still think this EV play with own driverless software, global expansion & battery swapping technology may be one of the best global performers in 2026

Rod Lowe@RodloweLowe

I suggested entering Fresnillo plc. 16 months ago at £5.60 with a price target of £40. It touched £39.18 in last week. I'm now suggesting entering $NIO at $4.68 with a longer term 3 yr. target of $58+

English

⚠️IF YOU HAD TO BUY AND HOLD JUST ONE STOCK FOR THE NEXT 5 YEARS, WHAT WOULD IT BE?

English

I suggested entering Fresnillo plc. 16 months ago at £5.60 with a price target of £40. It touched £39.18 in last week. I'm now suggesting entering $NIO at $4.68 with a longer term 3 yr. target of $58+

Rod Lowe@RodloweLowe

Fresnillo plc. chart depicts massive 12-year triangle completing with price coming to a reflection/ determination point at £5.60 area. The elliotwave count has £40+ medium term

English

In other words... "the wider the base, the higher the space" a terminology used in technical analysis for massive base building. The silver shares did this as well as an example of massive accumulation before upside price explosion. $NIO displaying similar chart characteristics.

NIO 🇨🇭 Investor@NIOSwitzerland

NIO The longer the accumulation (or consolidation/base) phase lasts, the stronger and more explosive the subsequent breakout tends to be...😁

English

$NIO....potentially has massive upside from current $4.67 over the next 12 to 24 months with return to profitability Q4'25, annuity income from BaaS and global expansion campaign. Price Targets of $24 (12 mth) & $58 (24+mth). Next Tesla but better i.m.o.

Steve Investing@SZ_Investing

Macquarie Upgrades $NIO to a Buy rating with PT $6.1

English

@Michael78208654 Will wait for the results on the 24th November & order book size and growth and then reply to above.

English

Stefanutti: Directors have authority to buy back shares passed under Special Res. 3 at the AGM on the 1st Aug. '25. With the R685m Kusile settlement & sale of Mozambique business proceeds & Zambian settle. ; it will be interesting to see how many shares they intend buying back.

English

@michaessers Claim 6. is significantly smaller than claim 5. Claim is for delays in Kusile only from 2020 to 2025....no idea if amount will get that amount at Financial on 24 Nov

English

@RodloweLowe Thanks for clarifying

Any idea what the damages claim might amount to?

English

Stefanutti awarded R685 mil. (ex vat) from Eskom tonight after close, they have now submitted their claim 6. Amazing how technical analysis can assist one in making decisions (see below). In perspective Stefanutti market cap "was" R750 million before the cash award announcement.

Rod Lowe@RodloweLowe

The seller at R4 out of the way now & the Eskom/Kusile Dispute award news appearing imminient, this reverse H&S technical play could start playing out into year end with PT of R9.50. Not many sellers around!

English

@michaessers Correction, the interest was included in the claim 5. sum awarded of R685 million cash on Friday. Claim 6. by SSK is a further damages claim for delays that occurred 2020 to completion in 2025. Unlikely that Eskom fights this as they elected 1 DAB specialist and SSK elected 1.

English

@RodloweLowe Great news.

Any idea the value of claim 6?

English

@CapitalShipyard Most of market were more than "skeptical" of this award. Changes Stefanutti entirely as a going concern as debt goes to zero, monthly interest on debt & legal fees go to zero (been paying both for 8 years at around R220m p.a. -at last count). Earnings can now be R4+ in 12 mths

English

Is this better or worse than everyone was expecting?

Rod Lowe@RodloweLowe

Stefanutti awarded R685 mil. (ex vat) from Eskom tonight after close, they have now submitted their claim 6. Amazing how technical analysis can assist one in making decisions (see below). In perspective Stefanutti market cap "was" R750 million before the cash award announcement.

English

@JSE_Invest CLH just bought back 43 million shares over last 9 months & cancelled then as well at an average price around R3.98. SA Inc. is finally working out how to create value; Allan Gray 'forced' to then announce an increase in their holding in CLH due to the 8% cancellation of shares

English

#JSECMH: Combined Motor Holdings buying back 15% of shares outstanding. Epic. Had too much cash for way too long. I only have a small position because it's taken forever for them to do something. Good to see it finally happen.

English