پن کیا گیا ٹویٹ

AppWorks

689 posts

@AppWorks

Going the distance with founders in web3 + AI 🥷 2,086 founders accelerated 💎 $380M total fund size (takes both tokens & equity)

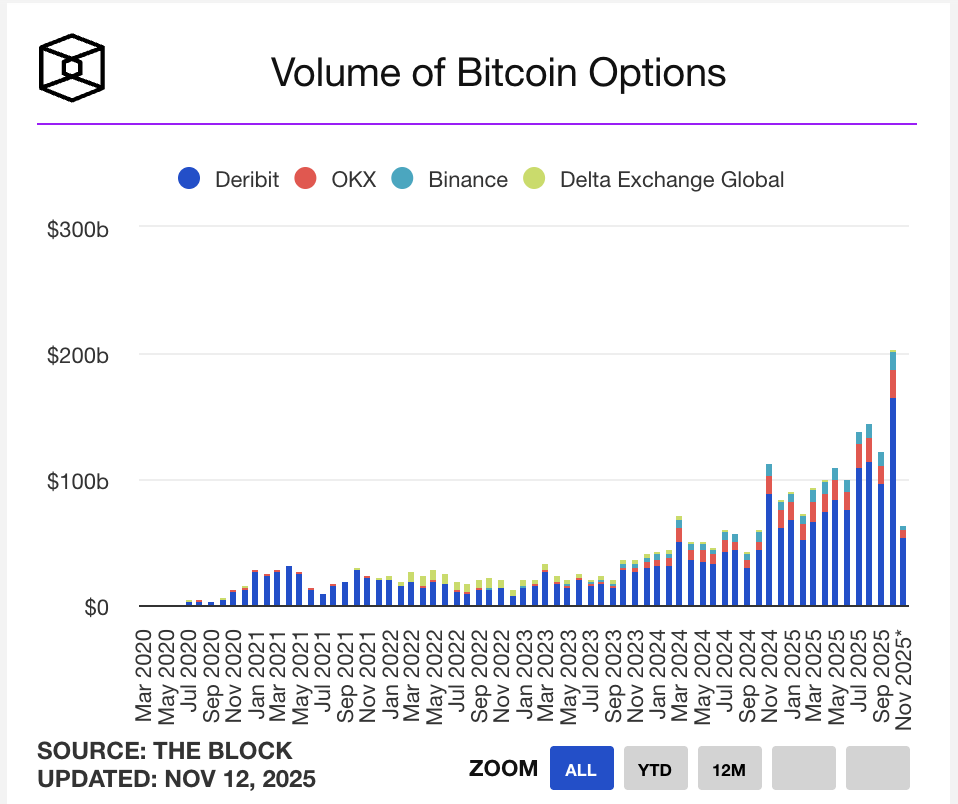

Pre-seed crypto deals have fallen off a cliff — by quarter: Q4 ’24: 345 Q1 ’25: 117 Q2 ’25: 104 Q3 ’25: 55 Q4 ’25: 31 Q1 ’26: 5 source: the block

0/ Breaking down #UNIfication from the $UNI value accrual POV 🧵 🦄 Use Protocol Fees to burn $UNI TLDR: It’s huge and meaningful. But at the expense of LP’s profitability. Need to observe more. The long overdue and highly anticipated fee switch will go live. TLDR would be using 1/4 to 1/6 (depends on the pool fee tier) of the LP fees to burn $UNI.

Building DeFi’s Next Yield Powerhouse: 3-Month Retrospective In under 3 months, Boros has achieved: 🔷$2.83 billion in Trading Volume 🔷$4.7 billion in Open Interest 🔷$1m in Annualized Fees And we’re just getting started. Regardless of market conditions, unlocking the billions of untapped yield in funding rates remains our primary goal. The next steps are simple: 🔷New pairs such as SOL, HYPE 🔷New exchanges 🔷Educating new and existing users on various funding rate trading strategies Boros is Pendle’s key to making yield tradable onchain, as our Yield Unit mechanism can be used for any floating rate market. This means: 🔷Tradfi rates like T-bills and mortgage rates can all be captured by Boros 🔷The yield Boros can tap into is far bigger than crypto’s current 3.3T market cap 🔷Our current growth is a fraction of what’s possible long-term, even in just crypto (200B of OI) Bringing YUs into the mainstream won’t happen instantly, but nothing great in crypto was built overnight. With each new maturity and new pair listing, Boros gets one step closer to becoming DeFi’s next zero-to-one success. Let’s write DeFi’s next chapter together. Job’s not done.

Onchain Corporate Banking: No More Fintech, Just Techfin Going Forward Cross-border payments are just the entry point. The real opportunity is whether stables can disrupt the entire corporate banking stack. Once stables move beyond payments, everything else follows (treasury management, FX, lending, capital markets services). Capital markets services are basically helping companies issue RWA. Tokenized securities are one example, but the same concept applies to receivables tokenization or asset tokenization (even GPUs or other productive assets). These are all new ways for companies to access liquidity. So as stables slowly take over the banks' traditional lending roles, we're seeing a big shift. Companies are moving away from relying on banks for loans and turning to capital markets instead. Thats why we're keeping a close eye on the latest RWA adoption stories and any challenges popping up along the way. ▋ Cross-border payments remain the most mature stables use case in corporate finance Clients doing cross-border business have the strongest motivation to use stables (because their customers are demanding it, wanting to send and receive stables). HiFi / Bridge / BVNK turned "virtual accounts + stables wallets" into APIs that banks and large platforms can call. Users deposit in local fiat (virtual accounts/IBAN), then the system converts to stables for cross-border payments or onchain transfers. Real example: multinationals paying contractors globally. Settlement went from 3-5 days to basically instant. We're talking 100+ countries with over 10,000 contractors now choosing to get paid in stables. ▋ Onchain cash/asset management: A new paradigm for corporate treasury When customers pay stables, merchants receive money instantly. What happens next? These funds can directly convert to onchain money market funds (MMF), letting merchants do cash management and earn interest continuously. If merchants need liquidity, they can use it for repo borrowing of stables for instant payments. Banks can collect management fees from tokenized funds. Everyone benefits from this mechanism. Take Canton Network for instance: by September 2025, their onchain repo market reached a daily average of $340B. Even better, they started settling repos on Saturdays, moving beyond the old weekday-only standard in finance. On Saturday, August 12, 2025, Canton Network did a repo deal with US Treasuries and USDC. Big names like Bank of America and Société Générale were involved, with Circle handling the cash part. Tradeweb, DTCC, and Citadel Securities were all in the mix too. This marks a big shift: 24/7 capital markets are here, making it way easier for businesses to get cash anytime they need. ▋ FX settlement: The next big market in the stables ecosystem StraitsX already launched "stables-powered" cross-border acquiring with Alipay+ / GrabPay. Incoming tourists can pay with familiar wallets, merchants instantly receive SGD settlement. It's basically modularizing FX and clearing/settlement into software infrastructure. For end users, it's all about convenience (no more queuing at banks for currency exchange). For whoever controls distribution, embedding FX into the payment flow means they can capture higher spreads without anyone really noticing. So why use stables for FX at all. The 24/7 thing matters most when you've got cross-timezone, urgent stuff happening on weekends (think e-commerce, supply chain payments, broker settlements). Example: Singaporean tourists in Taiwan on Sunday trying to convert SGD → TWD. Traditional rails are painfully slow on weekends. But SGD stables → TWD stables settle instantly. And you can immediately park it in onchain MM funds to start earning yield. You're basically compressing cross-border float time from days to minutes. Or just settle straight through local RTP systems to get fiat TWD back. The FX I just mentioned uses stables to accelerate fund transfers in the middle. But liquidity between different currency stables pairs is currently very poor. So anything involving FX settlement still needs to go back through fiat channels, and once you touch fiat, speed slows down. But if more currency stables actually get adopted? Direct settlement between different country stables becomes the next big market. DeFi's always been good at providing liquidity for long-tail assets. Fluid's got this interesting vision of becoming an FX settlement platform. The concept's pretty clever: you borrow debt in different currencies (smart debt), and traders basically trade against your dual-currency debt position (say USDC + EURC). The transaction fees you earn offset your borrowing costs. It's like turning your debt into a revenue stream. Put all these pieces together and you start seeing a new FX primitive taking shape. Cross-currency liquidity meets credit. FX market making used to be this exclusive bank trading desk thing. Now multinationals holding various stables can just throw them into lending protocols for yield, or LP on DEXs. Or get really aggressive with leveraged LP on Fluid. Basically, any multinational with multiple currencies can become an FX market maker. You could even collateralize your onchain money market funds, borrow dual-currency debt for hedging, and simultaneously act as a forex liquidity pool. Use the LP fees to lower your actual financing and hedging costs. This is what next-gen "financing + market making" starts to look like. FX settlement's probably gonna be the most disruptive thing happening in the stables world. ▋ Onchain Capital Markets aka RWA RWA cases are everywhere now, won't bore you with those. Its not about the tech for tokenizing stuff. It's whether the surrounding infrastructure is actually there. Four things need to work: privacy protection, reusable identity and rights, onchain registration that holds up legally, and actual market infrastructure so you can borrow against these assets, pledge them, liquidate them. Privacy means transaction parties only see what's relevant to them (Canton's sub-transaction privacy setup does this well). Compliant identity needs reusable KYC. Same credentials work across multiple markets. No more redoing KYC every time you jump to a new chain or protocol. Legal ownership is about mapping real registries onchain so the onchain state actually holds up in court. Example: DTCC runs nodes on Canton that map to UST's actual registry. When it comes to trading and collateral, a few key things get overlooked a lot: - OES (Off-Exchange Settlement) keeps your assets at regulated custodians like BitGo. Exchanges just mirror credit limits. Way less counterparty risk, way less chance of someone "borrowing" your assets. - UTA (Universal Trading Account) bundles spot, derivatives, and lending all in one account. Same collateral pool works across everything. No more fragmentation by product line. - Digital money needs 24/7 settlement. When both securities and cash are onchain, you get true DvP (Delivery versus Payment). T+N basically becomes T+0. But there's still friction. MMFs hold traditional assets underneath, creating liquidity gaps on weekends. You need backup credit lines or market makers acting as weekend liquidity bridges. Bottom line: RWA's value isn't just "putting stuff onchain." It's getting all four tracks working together (privacy, rights, identity, settlement) so assets can actually be pledged, transferred, liquidated, and legally recognized onchain. ▋ The evolution of the stables narrative: From cross-border payments to corporate banking infrastructure The stables story has moved way past "cross-border payments." The whole corporate banking stack is shifting onchain. You receive payment, immediately allocate to MMF. Need liquidity? Do a repo. Use OES to cut exchange counterparty risk. Use UTA to unify margins across products. Add the digital cash leg, and suddenly 24/7 settlement with near T+0 DvP actually works. Winners won't sit around waiting for traditional institutions to catch up. They'll merge liquidity and credit into one thing. Turn settlement into an actual user experience. Enable weekend redemptions. Make collateral reusable. Allow direct cross-currency settlement. Make capital efficiency something users can actually feel. One thing I noticed recently: most crypto startups would rather partner with big consumer platforms than banks. Banks just move too slow. DeFi infrastructure's getting embedded into Consumer Tech and B2B SaaS instead. Banks are falling behind. Maybe we won't have fintech in the future. We'll have techfin everywhere.