daol

2.6K posts

$mara 드디어 청사진을 수익하고 연결짓는 내용들이 나왔습니다.

지금 갖고 있는 데이터센터 임대 + 소규모 데이터 센터 건설 -> 이때까지 우리는 유연하게 비트코인을 채굴하면 됨 = 한시도 쉬지 않고 돈을 벌 수 있는 구조를 만들었음

그리고 이걸 뒷받침해줄 클라우드 알파 버전 등장 그리고 이걸 자동화할 수 있는 엔지니어 채용공고까지 속도 내고 있는데 2년간 개쳐물린 입장에서 드디어 설레기 시작함

blog.naver.com/whddlr114/2242…

한국어

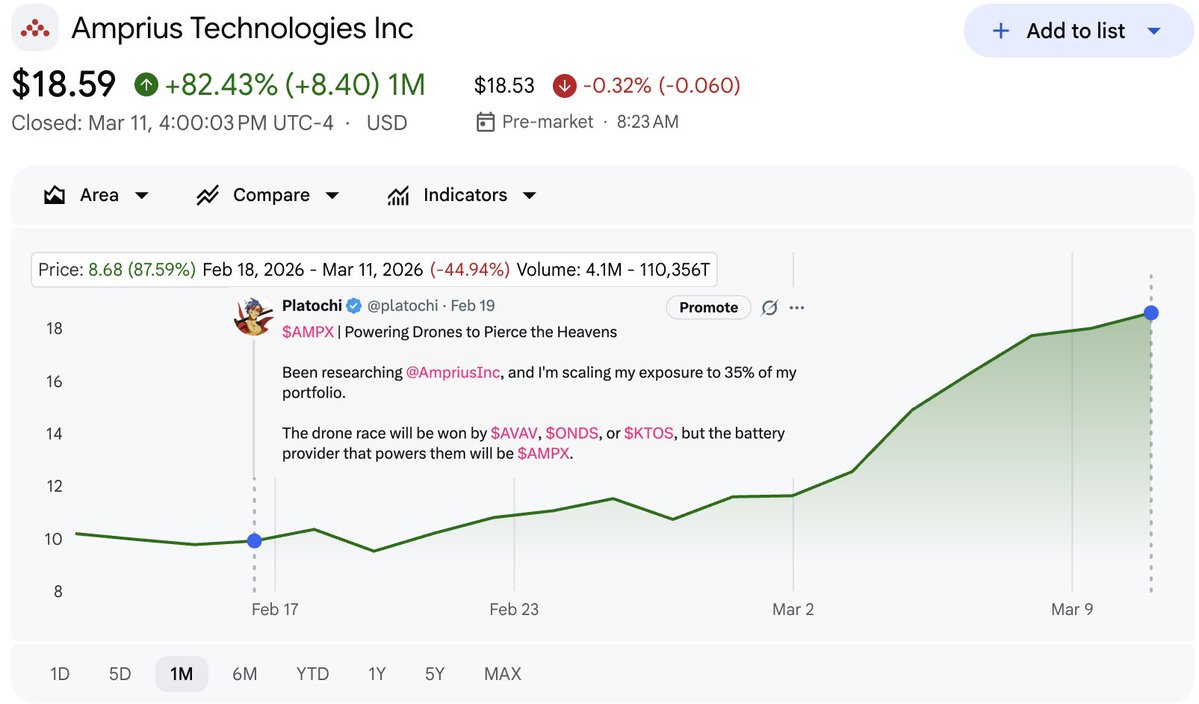

Wow! This might be the quickest 2x I've ever had.

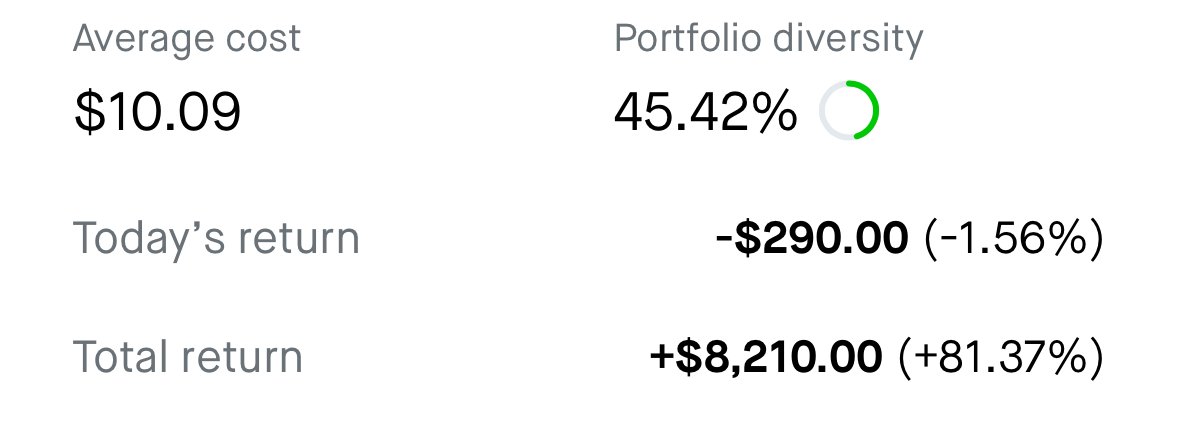

Extremely proud of my research on @AmpriusInc last month. Since posting about it, my $AMPX position is up ~80%. Ended up upping my allocation to ~45% and really glad I did after their earnings report.

감사합니다/thanks to both the Korean & English finX communities, especially @Daol224 @SJCapitalInvest @bennybigbull & @crux_capital_!

platochi@platochi

$AMPX | Powering Drones to Pierce the Heavens Been researching @AmpriusInc, and I'm scaling my exposure to 35% of my portfolio. The drone race will be won by $AVAV, $ONDS, or $KTOS, but the battery provider that powers them will be $AMPX. Q3 2025 numbers: - $1.2B MC - $21M revenue - Triple-digit YoY growth - Gross margins flipped positive at 15% (targeting 30%), - OPEX at 37% of rev (aiming for 10%) - -$2M EBITDA but backed by $73M cash and low burn rate. - ~20M shares out, efficient collections (92 DSO), and at-the-market issuance flexibility. Tech edge: Silicon anodes hitting up to 500 Wh/kg energy density — double what graphite-based cells do (250-300 Wh/kg). SiMaxx uses nanowire structures to handle swelling for high-end/niche apps, while SiCore (2024 launch) is built for scale on existing lines. Fast charging (0-80% in <6 min), dramatically extended drone ranges, better payload/endurance for eVTOL, defense, light EVs, wearables, and even humanoid robotics. A huge plus is their silicon anode batteries last about 2x longer than conventional cells. Good for people who like to 'monitor the situation.' Supply Chain: SiMaxx in Fremont, CA; SiCore anodes from spun-off China entity; cells in Korea (tariff dodge); QA back in US. Aviation drives ~75% revenue, plus defense/light EVs. A huge plus imo is that they decided to go fabless in 2022. That materially derisks them relative to their competition. Deals: Partnership with Nanotech Energy announced as of Feb/3. First U.S.-based manufacturing partner which makes Amprius compliant with defense, aerospace, and other mission-critical market needs. Amprius & Nanotech are developing the SA128 silicon-anode cell. Cell specifications include: Format: 21700 cylindrical Capacity: 6.8 Ah Energy density: 320 Wh/kg Not the theoretical max energy density reported from SiMaxx but close to SiCore tech specs. Differentiation: Proven tech + fabless efficiency positions them as the "picks and shovels" anode play in a $100B+ battery market (drone/eVTOL TAM ~$8-10B by 2030). Competitors are Enovix, QuantumScape (no rev yet), or CATL/BYD (mass scale but less edge in high-density niches). Risks: - Customer concentration (35% from one) - Geo exposure (China ties amid tensions) - Unproven at massive scale - Competitor with $ENVX (very bad execution) - High beta But cash buffer + IP moat offers resilience. Valuation outlook: Easily $4B MC by 2027, so a 2x from here. To 2028, P/S-based models (7.7 avg 12-mo or 11 shorter-term) project 70-133% upside (base ~70%, ranges -21% to +200% depending on growth assumptions). Longer-term 2030 scenarios eye 6x potential if they capture even conservative market share with strong margins. Trade setup: Macro + price action are bearish. If $AMPX hits high $8s/low $9s, I'll position on Jan/2027 leaps up to 35% of my port.

English

$ampx

고객사 444->550이상 확보

국방 드론 수요가 꽤 인상적으로 늘어났구나 생각이 드는 어닝콜이었는데, 여전히 점유율면에서는 한 자릿수여서 조금 걸리는 부분이 있긴 했습니다.

그래도 이걸 조금씩 채워가면 그만큼 상방이 크게 열릴 수 있겠다는 생각도 들었구요

blog.naver.com/whddlr114/2242…

한국어

$mara

드디어 가시화 되고 있는 행보(최소 연 단위로 기다려야 수익이 가시화 될 것 같음)

마라는 민감 데이터를 다루는 산업 바로 옆에 소규모 DC를 가져야 한다고 생각하고 있었음. 그런 의미에서 이번 SDV와 Exaion 협력은 이 청사진의 제대로 된 시작이라고 봄

blog.naver.com/whddlr114/2242…

한국어

$ampx 드론용 국내 배터리 공급망 강화에 있어 앰프리어스의 역할과 국방수권법을 준수하는 배터리 조달이 얼마나 중요한 우선순위가 되고 있는지를 강조합니다

Amprius Technologies@AmpriusInc

📰 Amprius was featured in Manufacturing Dive! The article highlights our role in strengthening the domestic #battery supply chain for #drones and how NDAA-compliant battery sourcing is becoming a critical priority. Read more below: manufacturingdive.com/news/amprius-t… $AMPX #tech

한국어

$ampx ceo 조사 좀 해봤습니다. 배터리와 자동화 분야에 꽤 굵직한 인사이고 마케팅적으로도 잘하겠구나 싶었습니다. 여러가지고 대 확장 시기에 적절한 인사였다는 생각이 들었습니다.

ceo는 이번 실적 발표 대단한 자신감을 갖고 있다는 점도 인상적이었습니다.

blog.naver.com/whddlr114/2241…

한국어