پن کیا گیا ٹویٹ

Public portfolio content coming soon.

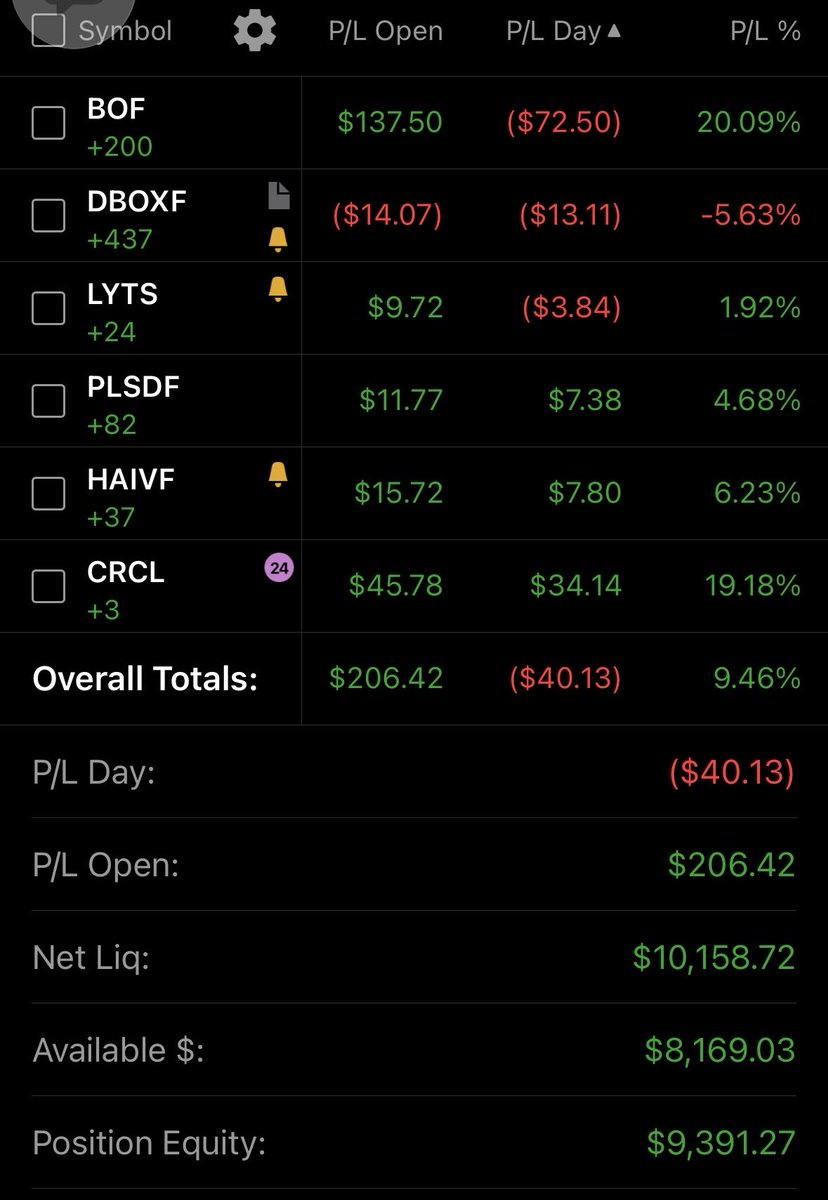

Added three positions in the last 2 trading days:

$BOF

$BWAY

$HAIVF (aka $HAI.TO)

Continuing to build out the portfolio, and will provide write-ups for each coming soon.

English

Goldilocks Zone Capital

1.3K posts

@GZ_Cap

Discovering underfollowed companies in the Goldilocks Zone (GZ) - where the right conditions exist for alpha.

Exploding drone boats hitting commercial shipping in the #StraitOfHormuz is exactly the type of threat industry has been warning about. The @USNavy and @DeptofWar need to rapidly integrate capabilities that already exist to maintain freedom of navigation.

$CRCL showing great relative strength today. Up over $100 - looking like it has the potential to be a true market leader

Very soon there are going to be more AI agents than humans making transactions. They can’t open a bank account, but they can own a crypto wallet. Think about it.