@aleabitoreddit @Andres17G With this reaction assuming it didn’t go through. But just a guess

English

Ray B

1.2K posts

@aleabitoreddit Anything explaining axti's 20% jump?

$EOS.AX - This $1B laser defense stock is Iran's Worst Nightmare. I have worked in the defense sector for 20 years and I have never seen risk/reward like Electro Optical Systems. Here's why this tiny energy directed weapon specialist inspired by Star Wars is the next multi-bagger. The nature of warfare has fundamentally shifted. Expensive, multi-million dollar platforms are now vulnerable to $2,000 drones. This has created a $100B+ global scramble for a Hard Kill solution that scales. EOS is the only company with the tech, the battle-tested results, and the export freedom to own the global market. The Rest of World Monopoly Geography is the ultimate moat in defense. US-based pioneers like $LASR (nLIGHT) are world-class but bound by strict ITAR (export) regulations. The EOS Edge: $EOS.AX is completely ITAR-free. While US tech is often locked behind years of red tape, EOS can deliver to Europe, the Middle East, and Asia with unmatched agility. This is why Germany recently bypassed legacy domestic giants like Rheinmetall to invite EOS to the table. As CEO Andreas Schwer (ex-Rheinmetall) stated: "EOS can deliver twice the power for half the price by 2027" The Sovereign Pivot - Australia’s $5B Bet The Australian Government has identified a negligible domestic drone defense capability and allocated $5B–$10B to fix it. EOS is the only domestic player with integrated, battle-proven kinetic (Slinger) and laser (Apollo) systems. Global Validation (The 100kW Milestone) While others are in the R&D phase, EOS is in the delivery phase. The Netherlands - Signed the world’s first export contract for a 100kW High Energy Laser (HEL)—a €71.4M (~A$125M) deal. Ukraine & Middle East - EOS systems are already on the ground, proving their kill-link accuracy in the most intense electronic warfare environments on earth. The Geographic Valuation Gap The market is pricing $EOS like a local manufacturer, ignoring its role as the global challenger to US-restricted tech. $LASR - Valued at ~$3.6B USD as the US domestic champion. $EOS.AX - Valued at ~$1.2B USD as the Rest-of-World champion. Both companies are addressing the same massive structural tailwinds, but $EOS.AX provides exposure to the entire global market at a fraction of the valuation of its US-listed peers. The Financial Inflection (By the Numbers) Gross Margins - Hit 63% in the most recent results; tier-1 tech margins. Order Backlog - A record $459M (up 238% YoY), providing massive revenue visibility into 2027. Bottom line - $EOS has the technology that Europe, the Middle East, and Australia are desperate for. It is the only ITAR-free pure-play in the world capable of delivering the future of counter-drone warfare today. For a deeper look into EOS, check out my substack (link in profile + first comment) for deeper dives into all things EOS.

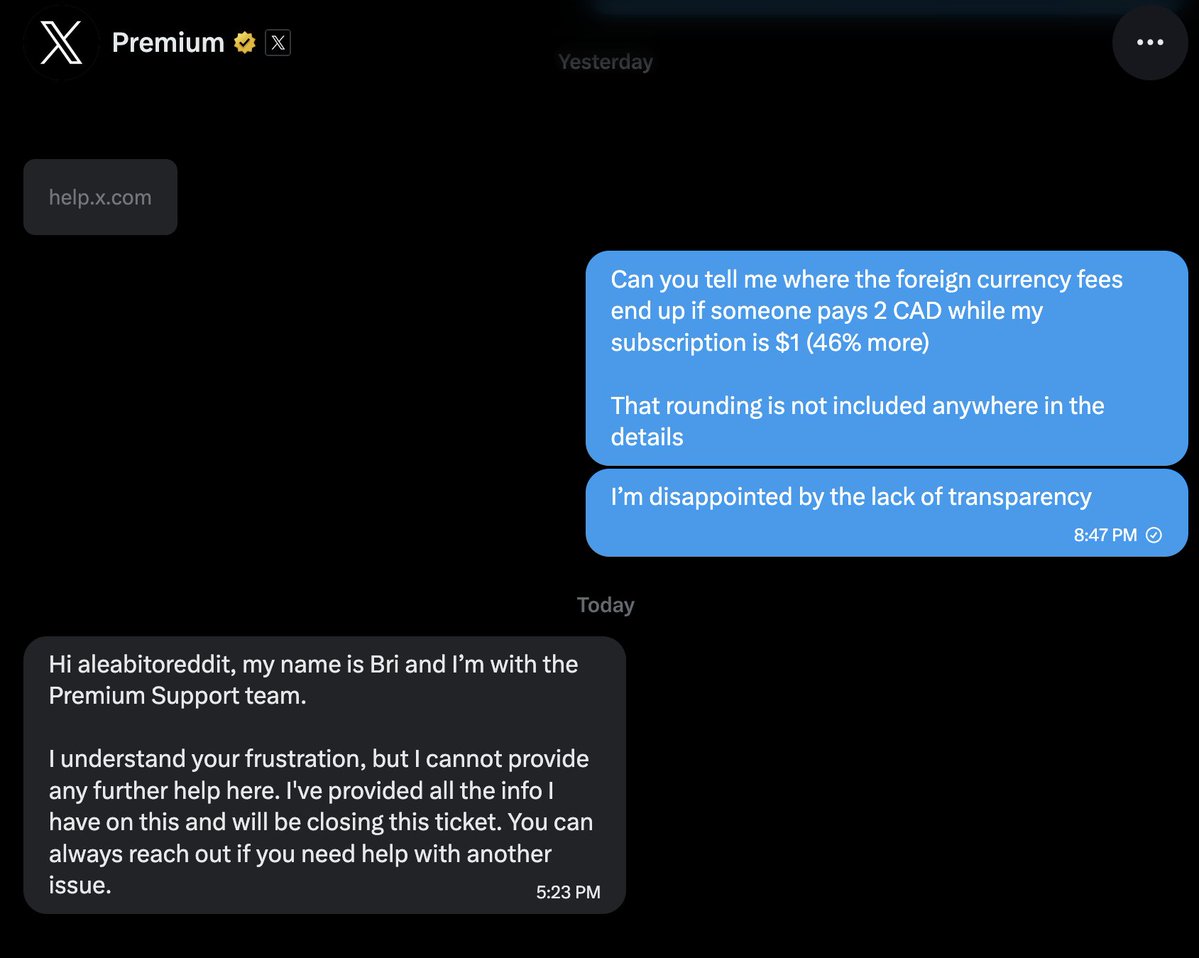

Just in case you’re wondering why I’m bullish on $CRCL and Stablecoins. 8605 subscribers at $1.00: -> $1595. Not even including int. like Canada paying 46% more (2 CAD vs $1 USD subscription) and the FX/rounding disappearing into the void. I’m not here for subscription revenue so I don’t plan on changing anything. But just found this pretty amusing even if you factored in pro rata or holds/delays. You would reduce 30% App Store fees, Stripe card TX fees, and other black box fee mechanisms like foreign currency rounding. Stablecoins are definitely the future, and you can already see banks trying to control it with Clarity Act lobbying.

$SIVE is now up +73.78% today ($231M MC). As markets price in information synthesis of the next potential $LITE of photonics. If I had to explain the difference: One laser source in Lumentum primarily benefits from current optical bottlenecks. The other in $SIVE is for the upcoming CPO/Silicon Photonic bottleneck. Lumentum is largely benefiting right now from $NVDA and hyperscalers securing capacity of EML lasers for current pluggable optical transceivers cycles. As seen with the current EML bottleneck, hyperscalers are buying out any 800G/1.6T transceiver + upstream capacity from: - $AAOI (in-house) - $COHR, $LITE (EML lasers + design) -> $FN (assembly) - $COHR, $LITE (EML lasers) -> Innolight / Eoptolink What's next? Silicon Photonics and Co-Packaged Optics. The architectural shift to CPO requires massive arrays of high-power CW DFB lasers. And this would likely trigger a complete, sudden paradigm shift in volume demand. $SIVE benefits from InP CW DFB lasers for SiPh and CPO: The up and coming companies like: $AYAR, $POET source $SIVE lasers, but primarily do advanced packaging. Then they feed up to larger companies like $MRVL Celestial (that buy $POET's interposers). However, if you go upstream, the light source is $SIVE. CW DFB lasers are light engine ( $SIVE ); the silicon photonics package ( $POET and others) is how it gets transmitted. CPO scale is not there yet. But we know it's coming. And as seen with current optical transceiver cycles: - Light sources from $LITE and $COHR demand much higher valuations than companies like $FN that focus on advanced packaging. Markets have been focusing on $POET, but missed where they get the actual $LITE type light source for Starlight. The risks are present including facing multi-source competition with $LITE, $COHR, $AVGO, and others. So again, make sure to do your own research. But my argument against that: Sivers been early enough to tailor custom lasers to fit $POET, Ayar, and other specifications before they got popular (sort like the $POET to $MRVL Celestial analogy). There's volume risks as well: But the potential Win Semi qualification offsets that. Dilution risk to scale capacity, is always present with every early-stage company as well. I did my thesis on $LITE last year and still love the stock for Google TPU ramp/OCS. But this year, I'm focusing on: $SIVE, as my personal CW DFB laser exposure for the new photonics architectural shift. I’m sharing my own thoughts on capturing the rotation from the current EML cycle to the upcoming CW DFB/Silicon Photonics cycle.