Ben Kizemchuk@BenKizemchuk

Financial markets are losing flow support:

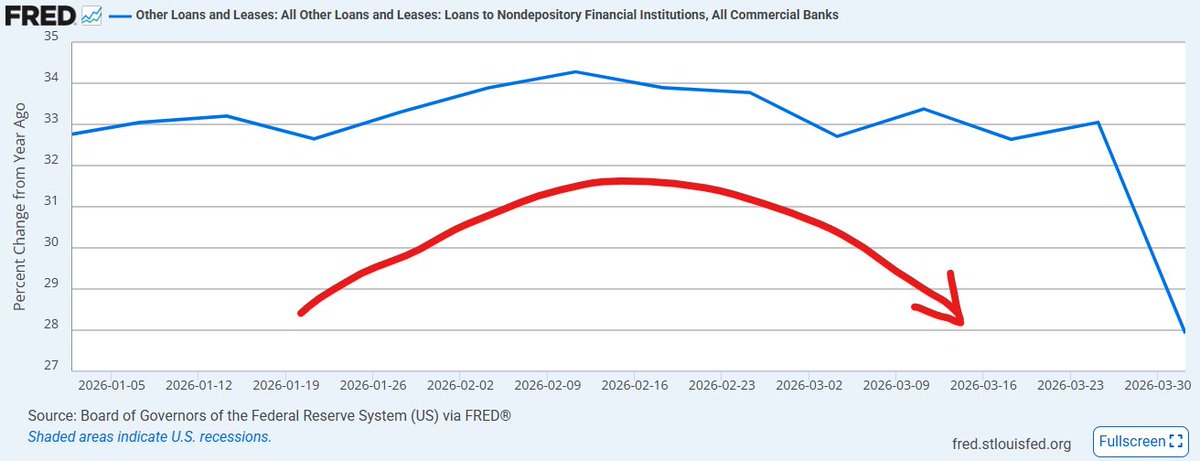

The rate of change in bank loans and leases is flattening near recent highs, indicating that private sector balance‑sheet expansion is beginning to lose momentum. Lending to non‑depository financial institutions (NDFIs), which accounted for a disproportionate share of marginal loan growth over the past cycle, also appears to be leveling off from peak rates of growth.

This coincides with a continued negative year‑over‑year change in federal deficit spending. As a result, the flow of net financial assets being supplied to private‑sector households and corporations is smaller than it was a year ago, reducing the incremental addition to incomes and balance sheet capacity. Although this shift began in late 2025, its effects manifest gradually rather than immediately.

When the growth of net financial assets slows relative to the stock of existing obligations, pressure builds over time. Income growth decelerates, internal liquidity cushions stop accumulating, and the private sector becomes increasingly reliant on credit expansion to sustain nominal activity.

In the early stages of this process, nominal spending can remain firm even as real momentum weakens, because a greater share of demand is financed through credit rather than through rising net incomes. To the extent that productive capacity and supply fail to keep pace, this dynamic can show up as higher prices rather than higher real output, not because demand is accelerating, but because financial claims are growing faster than the economy’s ability to absorb them through increased production. This is likely what we’ve been seeing across various measures over the last six months.

As the fiscal slowdown persists, however, the system begins to tighten rather than reflate. The reduced net inflow of financial assets erodes the foundation that previously supported expanding leverage, and credit growth loses acceleration. Borrowers become more sensitive to rates and terms, while lenders respond to weaker cash‑flow trends by tightening standards. The result is an inflection lower in lending growth, just now visible across bank credit aggregates.

At the same time, growth in retail money market fund (MMF) balances has begun to flatten as well. While MMFs do not generate new net financial assets, they play a central role in distributing existing cash into short‑term funding markets, particularly through overnight repo. When MMF balances are expanding, the system benefits from a growing supply of readily available cash that helps absorb collateral issuance and stabilize funding conditions. When that growth slows, the margin of safety in short‑term funding markets narrows, even if outright stress does not materialize immediately.

In parallel, credit spreads have begun to widen, reflecting increased caution around repayment capacity and refinancing risk. This widening carries outsized macro significance in the current financial structure, where a large share of incremental lending is intermediated through NDFIs rather than funded through traditional banking channels.

NDFIs, particularly private credit vehicles and fund‑finance structures, have been central to financing some of the most capital‑intensive areas of recent growth, including data centers and AI‑related infrastructure. These entities typically rely on layered funding arrangements: bank credit lines, warehouse facilities, and market‑based leverage. Their lending capacity is therefore highly sensitive to both spread volatility and funding conditions.

In such a system, rising spreads do not remain confined to end borrowers. Funding costs reprice at multiple layers simultaneously: for operating companies, for private lenders, and for the banks providing backstop financing. As these pressures feed back through the system, credit availability tightens more abruptly than aggregate loan data alone might suggest.

This is where slower credit formation begins to translate directly into slower income growth at the macro level. Because new lending generates new financial claims and spending power, a deceleration in credit creation reduces the flow of income through firms and households. At this stage of the cycle, when fiscal inflows are also contracting, households and corporations tend to respond by scaling back discretionary activity, deferring investment decisions, and placing greater emphasis on liquidity preservation.

Taken together, slowing net fiscal inflows and tightening financial conditions are now poised to start reinforcing one another, constraining both the creation of new financial assets and the spending they support. The result is a potential broad deceleration in economic growth driven by the cumulative effects of weaker flows through the financial system.

In this context, equity markets become more vulnerable to sustained drawdowns. With weaker flow support underpinning incomes and balance sheet expansion, valuations rely increasingly on sentiment and positioning rather than improving fundamentals. That raises the likelihood that market weakness persists or re‑emerges after rallies, and that downside risks remain elevated unless either fiscal flows or credit growth can re‑accelerate meaningfully. Under those conditions, a failure to stabilize could open the door to a much larger adjustment over time, including the possibility of an extended bear market decline on the order of a 50% retracement from the January peak, should macro flows continue to deteriorate.