Tweet ghim

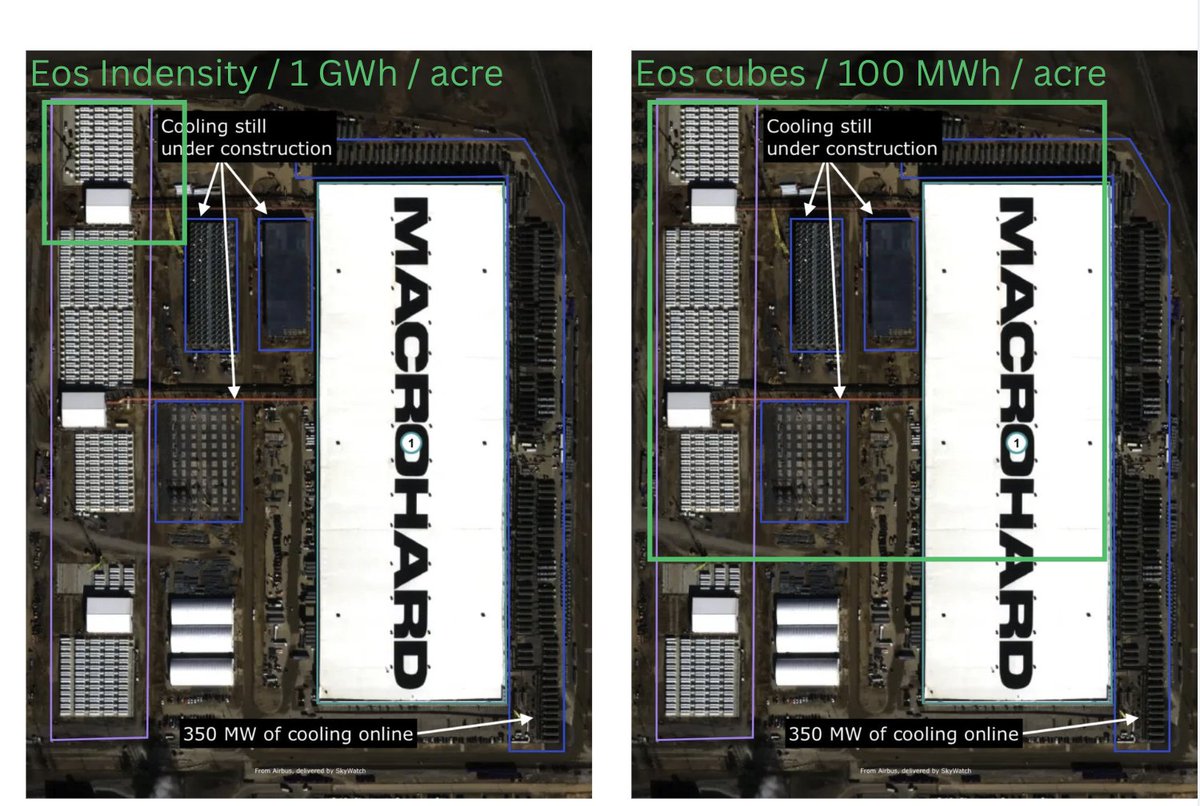

This is why $EOSE Indensity actually matters.

The image makes it clear. On the right is what ~100 MWh per acre looked like with the old Eos cubes. A 1 GWh system needed something like 10 acres, which immediately ruled out data centres and most sites near load, regardless of how safe the chemistry was.

On the left is what Indensity changes. Same zinc chemistry, completely different architecture. By building vertically around a steel superstructure, Eos compresses that same 1 GWh into roughly one acre.

In hindsight, this was always the plan. There is no way Eos could have seriously targeted data centres while accepting the footprint of the cubes. Zinc’s safety advantage only becomes economically useful once you use it to build up instead of out.

I do not think the market has absorbed what this unlocks. This is not just about data centres. It opens up urban deployments, tight substations, constrained grid nodes, and sites next to existing gas generation where land is scarce but firm power is valuable. Indensity lets Eos bring zinc into places lithium struggles, and challenge lithium on one of its historical strengths: density.

🔋 Battery Buffett 🔋@BatteryBuffett

Very rough estimate of the land usage required to reach similar GWh stored if you used Eos Indensity at 1 GWh / acre instead of Tesla Megapack $EOSE (Green square)

English