Loic LeMener CFA, CFP® đã retweet

Loic LeMener CFA, CFP®

4.5K posts

@CfaDallas

I like to post contrarian data points. Not advice! See important disclosures here: https://t.co/MA7VJvMMjU

Free cash flow race to the bottom.

Wall Street to Main Street hits record high: value of financial assets is now 6.7x US GDP, the highest ever

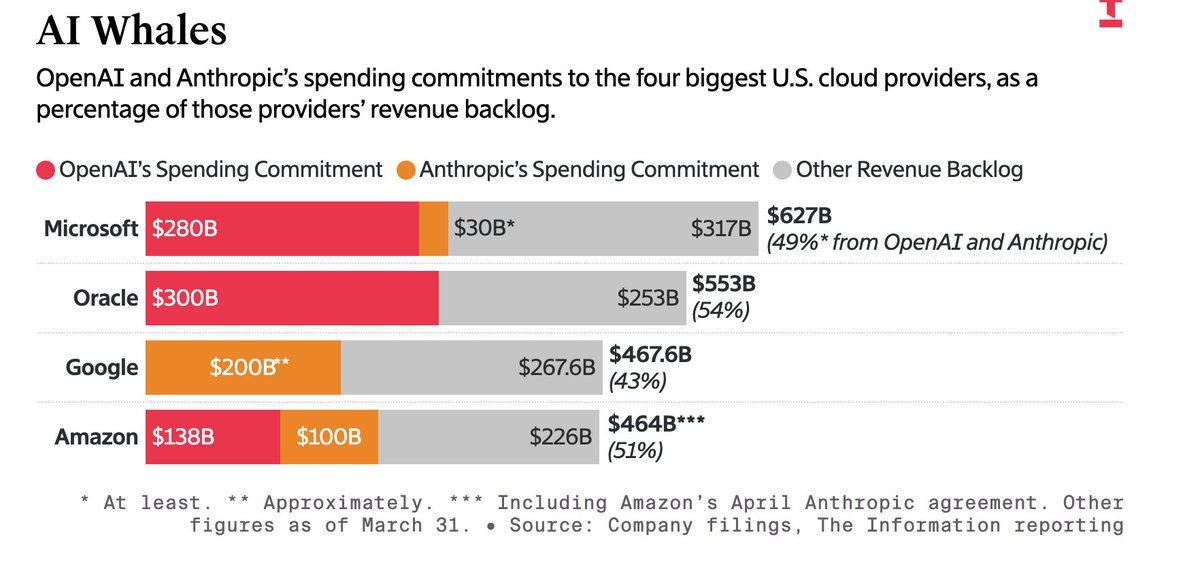

"I'm willing to go bankrupt rather than lose this race." Google co-founder Larry Page on the AI spending race. Looks like he wasn't kidding.

*ALPHABET RAISES 2026 CAPEX GUIDANCE TO $180B - $190B Previous range for $GOOG was $175B - $185B. CFO also noted that 2027 capex is expected to increase “significantly” from 2026 capex

‘DESERT WARRIOR’ is tracking to be one of the biggest box office flops of all time. The Saudi Arabia-funded film has earned $488K so far on a $150M budget.