@ZDNet AI/ML reporter; Editor, The Technology Letter. Covering business and technology for 31 years for Barron’s, Fortune, Bloomberg, NY Times and others.

Some things make absolute sense, like the gradual replacement of copper by optics in the backplane of equipment racks. We’re in a climate, however, where some of it is being rushed by one company’s agenda. Worth keeping in mind as one contemplates the very bright opportunity in front of laser suppliers such as Lumentum and Coherent.

Lumentum and Nvidia push ‘scale up,’ but is it real?

Nvidia’s vision for computing is supercomputers dedicated to AI. A lot rests on the fiber-optic components that Lumentum, Coherent, Broadcom and others make. It could be a big expansion of their market opportunity. Risks include the possibility that the world won’t completely accept Nvidia’s vision for everything.

$LITE $COHR $NVDA

thetechnologyletter.com

I’m delighted to report that The Technology Letter is featured on the Bloomberg terminal. I was a reporter at Bloomberg twenty-three years ago covering tech. It remains one of the best business news reporting outlets in the world. Every day now, you can see TL articles on major company and stock developments direct in the feed for a given ticker.

If you don’t yet have a Bloomberg Terminal subscription, you can sign up here: bloomberg.com/professional/e…

For the latest direct from TL, check out the home page: thetechnologyletter.com

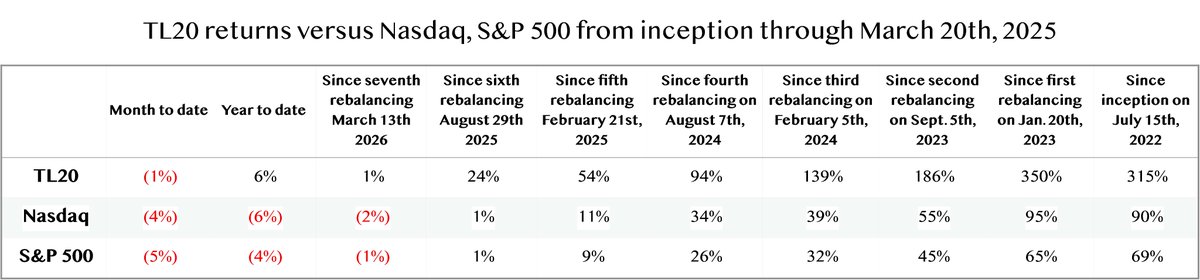

I’ve been writing for over a decade about a semiconductor renaissance taking place. That development is building now every day, with hundreds of companies such as Google having become chip designers. This week I rebalanced the TL20 group of stocks to consider, which is up 320% in three and a half years. One of the new additions is Celestica, the principal maker of the TPU under contract with Google. Celestica is in that bunch of contract electronics manufacturers (EMS) that do an amazing job of getting by with thin margins and still generating real cash profits. In a little over 3.5 years, the TL20 is up 315% even in this tumultuous market.

The TL20 rebalancing: The biggest thing since the microprocessor

Whatever you think about speculative excess in AI, the fact is that we are at an historic moment in the history of computer chips, a semiconductor renaissance that has been gathering steam for years. That very profound change is sending ripples through the tech market. Nvidia is a big part of the story. Here are other ways an investor can capture the seismic shift.

thetechnologyletter.com

$CLS

Micron could go as high as $700 as the numbers are just incredible

Micron Technology turned in an astounding second-quarter report, with gross profit of seventy-five percent, and a twenty-billion-dollar-per-quarter DRAM business that is tripling. Price targets are as high as $700. And yet, people are selling on the news. The chief risk to Micron is over-supply, and Micron itself doesn’t know how much supply would be too much. Probably, over-supply risk is remote at the moment, even if it’s not zero.

thetechnologyletter.com

$MU

$NVDA

It’s funny because Nvidia is facing gigantic capital returns to its shareholders, but the stock is not moving. And I suspect it has something to do with the fact that nothing Jensen Huang says about AI is reassuring these days. The way he describes the It world is basically as slaves to OpenAI and Anthropic, which is depressing. He’s got to find a new narrative.

Nvidia could have half-trillion in buybacks and dividends the next few years

Nvidia CEO Jensen Huang used his meeting with analysts on Tuesday to emphasize a trillion dollars in orders. Equally astounding is the potential for half a trillion dollars in buybacks and dividends over the next three years that his CFO, Colette Kress, implied. Once again, though, Huang’s remarks about the AI bubble were a bit tone-deaf.

thetechnologyletter.com

$NVDA

Adobe badly needs a visionary at the helm

The Narayan era at Adobe was one of talking up business metrics such as “RPO” and other very dry stuff about “SaaS.” The company became trapped in that kind of language and that mindset. The problem is it no longer impresses investors, and it can’t possibly be exciting for customers. Adobe’s competitors such as Canva and Figma are doing a better job of articulating what working with AI might look like. Adobe desperately needs a visionary to show how the company will lead in an era of change.

thetechnologyletter.com/the-posts/adob…

$ADBE

Buyers name software’s price: a look at the deals

Here’s a fun game you can play at home: Which aging software giant will try to make up for a lack of innovation by acquiring a younger firm currently in the bargain bin? Which private equity shop will milk the cash flows of some struggling outfit under the pretense of “making it great again”? If you want to know what happens to software stocks, consider the prices at which firms have been taken out, including IBM’s $10 billion deal for Confluent and Salesforce’s $8 billion deal for Informatica.

thetechnologyletter.com/the-posts/buye…

$CRM $NOW $DT $DDOG $TWLO

Cohesity CEO: ‘AI is a tsunami coming at you, you’re either buried or you surf it’

Please enjoy my interview with Cohesity CEO Sanjay Poonen.

Sanjay Poonen of privately held Cohesity is glad his company is still private in a stock market that is very unfriendly to software shares at the moment. Still, he is optimistic that in coming quarters, major software makers will prove the “Death by AI” mania is wrong. In the meantime, he boasts that an increasing amount of Cohesity code can be automated via AI.

“Thirty to forty percent of our code now is being generated with Claude Code.”

thetechnologyletter.com/the-posts/cohe…

$RBRK $CVLT

Oracle by the numbers ain’t pretty

Oracle shares are rising because the growth that had always eluded the company is finally appearing. That’s at the cost of an orgy of debt and massive cash burn. Most important, the level of customer “concentration” is not being disclosed, a serious risk for the company.

thetechnologyletter.com/the-posts/orac…

(For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.)

$ORCL

Meta, Nvidia rush to agentic AI even as software stocks get cut further

It certainly seems like the market is totally f*cking nuts when responsible software vendors keep sinking in valuation while Nvidia prepares to unleash more of the AI stuff that is shutting down networks.

thetechnologyletter.com/the-posts/meta…

(For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.)

$META $NVDA $HUBS $ZS $CRM $NOW $AMZN

Micron: Yes, it is, kind of, different this time

Micron’s market is still cyclical, but the slope of this current cycle suggests a stock crash is not imminent.

thetechnologyletter.com/the-posts/micr…

(For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.)

$MU

I’ve made mistakes, and then I picked Oracle

Stargate always seemed farcical. Why didn’t I trust my gut?

(For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.)

thetechnologyletter.com/the-posts/ive-…

$ORCL

So, Google’s YouTube is the biggest media company in the world

The giant’s clever curation of “skinny bundles” has produced over 150 million paying video subscribers. Who wouldn’t want that! It’s now a half-trillion-dollar business.

(For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.)

thetechnologyletter.com/the-posts/so-g…

$GOOGL

I'm often asked about whether I invest my own money in the things I write about and recommend. I do not. The reason is pretty simple. In decades as a journalist at Dow Jones and other institutions, I followed a rigorous code of not having conflicts of interest. I have maintained that rule as a publisher of my own newsletter. I think it allows me to be intellectually objective in my assessment of investments.

BE Semiconductor sometimes seems like one step forward, two steps back

Shares of BE Semiconductor sold off hard on Friday based on several millions of a meter’s worth of chip design. It’s not fatal, and the outlook still looks good for the company’s “hybrid bonding” technology.

thetechnologyletter.com/the-posts/be-s…

$BESI

Marvell? I’ll stick with Broadcom

Marvell’s stock has gotten a reprieve this morning, and the business does seem in fine shape. But I’ll go with the company that has a broader book of business and deeper resources, Broadcom.

For a limited time, subscriptions to the newsletter are $1 a week for the first four weeks.

thetechnologyletter.com/the-posts/marv…

$MRVL $AVGO

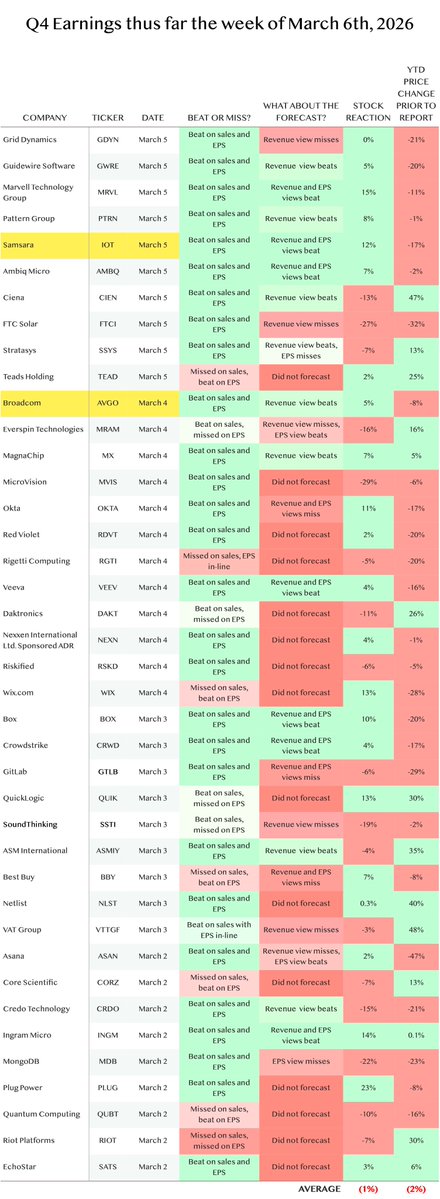

Samsara is doing just fine, let’s see if the stock holds gains

Software maker Samsara has continued to demonstrate what you call “durable growth.” We are going to see if that is enough for the shares to hold onto gains going forward, of if the stock will slump again as it has many times in past.

thetechnologyletter.com/the-posts/sams…

$IOT