Sabitlenmiş Tweet

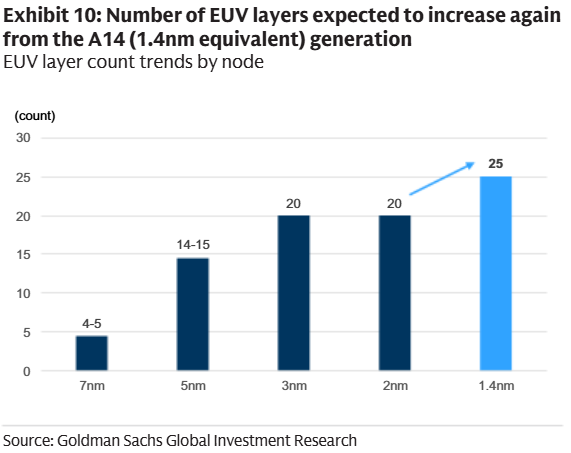

Growth in the digital economy is supported by many themes - AI, Cloud , Automation, Energy Transition & Edge Computing.

Underpinning it all...semi-equipment companies. They have high barriers to entry & have dominated their niches for a long time.

$ASML $AMAT $KLAC $TEL $LRCX

English