AfterMathAnalytics

267 posts

AfterMathAnalytics

@AfterMath_2819

Aftermath Analytics decodes what comes after the chaos. Built for traders who think in probabilities, not emotions!

the universe 加入时间 Ekim 2025

52 关注24 粉丝

@Barchart I'm sure this is going to work out GREAT

English

@wiseadvicesumit @Barchart or maybe it isnt .... but who knows.. We're good

English

@kaitduffy lol aint no way in the worldwould i try the things i did in my early 20s but..... one can dream haha

English

35 years-old and still doing molly like are you trying to die

English

Service now will be a great buy soon. These software companies will lead out of the bear market ( if we ever see one again)

Wealthmatica@wealthmatica

Is ServiceNow a solid buy right now before the market rotates back into SaaS? 🤔 $NOW

English

@LanceRoberts nothing to see here folks! Just a credit cycle about to collapse along with the american empire.

English

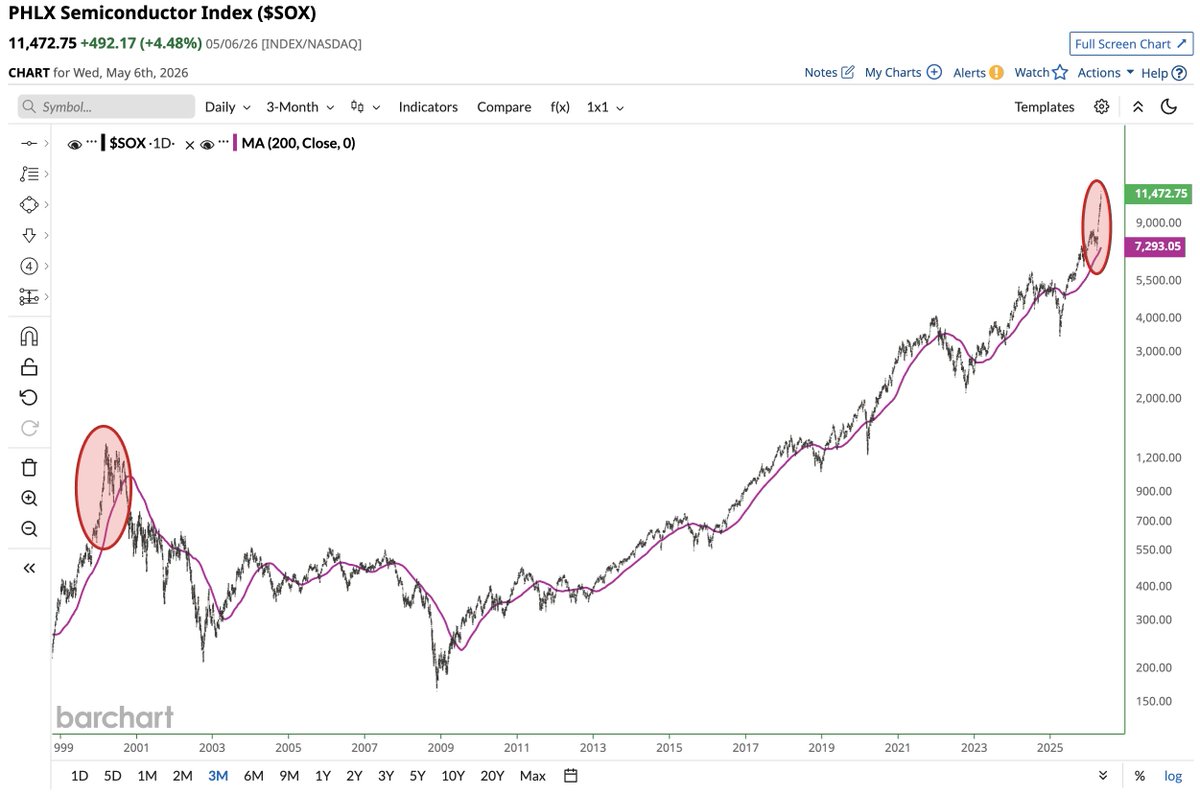

Two extremes hit at the same time: the riskiest stocks hit all-time highs relative to the S&P 500, while the safest stocks hit all-time lows.

English

lol the traders who say 0 or idk 8 or something thinking that means their a good trader just tells me that poor grasshopper hasnt learned to hop yet haha! He will get there. For me..... hundreds, then i started backtesting the right way. See platform for more

Trader Theory@tradertheory

How many times have you blown an account? The number nobody wants to admit out loud.

English

@jbulltard1 either that or the buck stops here. Either way we will find out who is right shortly

English

@assface_burner hate to be this guy but i have a platform that helps you see this.... we are in some volatile times.... aftermathanalytics.com

English

I quit

$spy puts positive for 2 days for 0dte and 1dte

Calls negative

$vix up

Yet $spx keeps going up

English

Deep dive incoming. Full backtest breakdown + what it means for NOW positioning: aftermathanalytics.com/?utm_source=tw… #trading #markets #fintwit

English

The setup: NOW could pop next month. But holding through Q3? History says no. Are you taking the 1-month edge or waiting for capitulation?

English

3 historical matches. Median 1-month return: +0.8%. Win rate: 67%. But 3-month: -11.3%, 0% win rate. Short-term bounce trap?

English

$NOW just crashed 61% from peak. Testing support or capitulation? We ran reversal patterns on the wreckage. Here's what history says. 📊

English

$NOW crashed 61% from peak—is it capitulation or a value trap? History says bounce: 3 similar setups averaged +0.8% in 1 month with 67% win rate 📊 aftermathanalytics.com/?utm_source=tw…

English

English