Vulpes Bio

1.9K posts

Vulpes Bio

@Vulpescap

B.S/PhD in Biology Former analyst at biotech-specialist HF Citizen of Graham and Doddsville VIC member Not investment advice, my opinions only

加入时间 Nisan 2024

159 关注1.8K 粉丝

@TweetAwayDK That said even efficacious antidepressants fail trials often due to pbo performance

English

@Vulpescap Ah, right. I read where you said there wasn’t any drug left on board at day 14, just didn’t connect that to what we see in the chart. Thanks

English

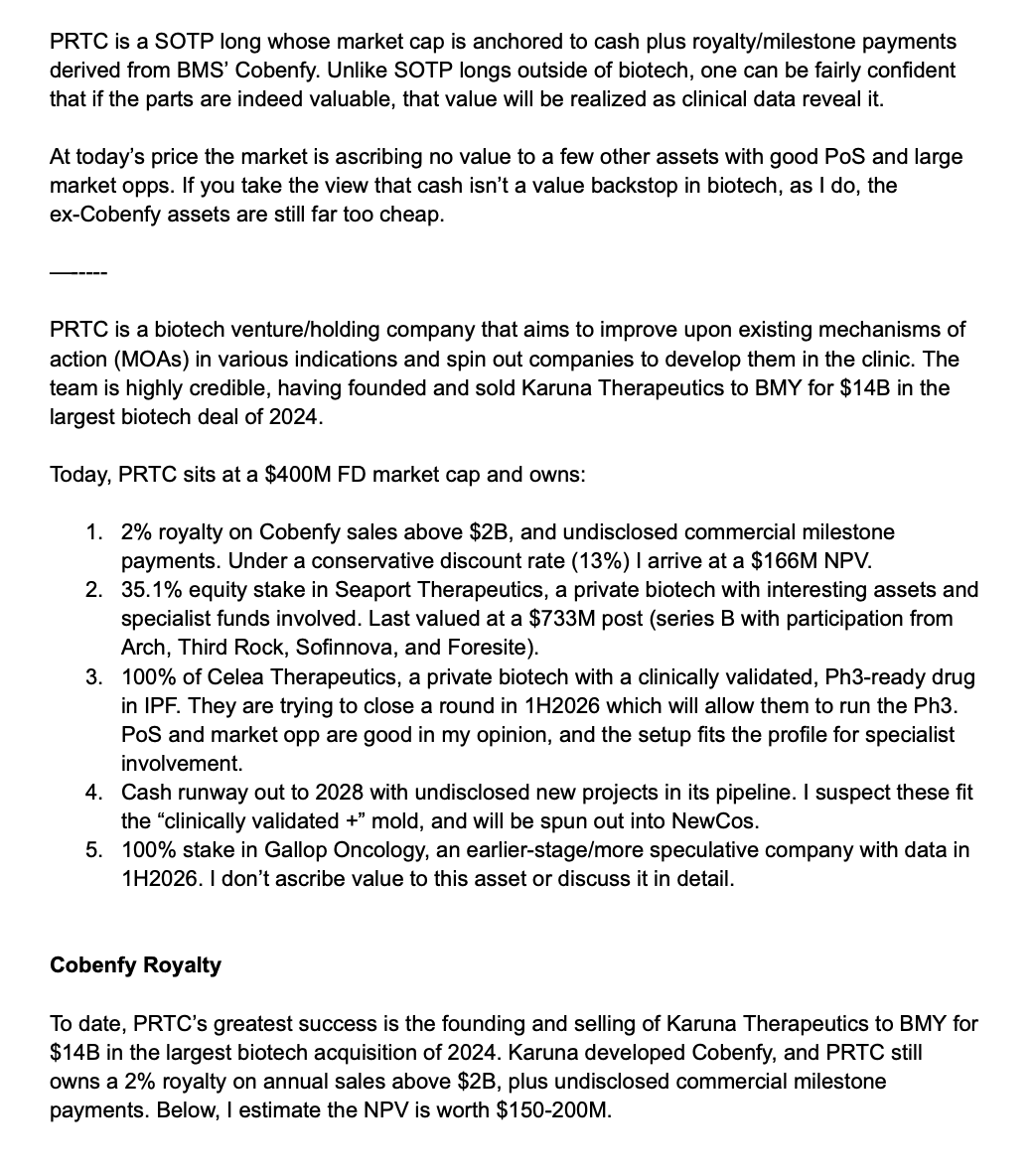

$PRTC too cheap at $400M FD IMO. UK-listed, low liquidity, doesn't look like anyone is paying attention.

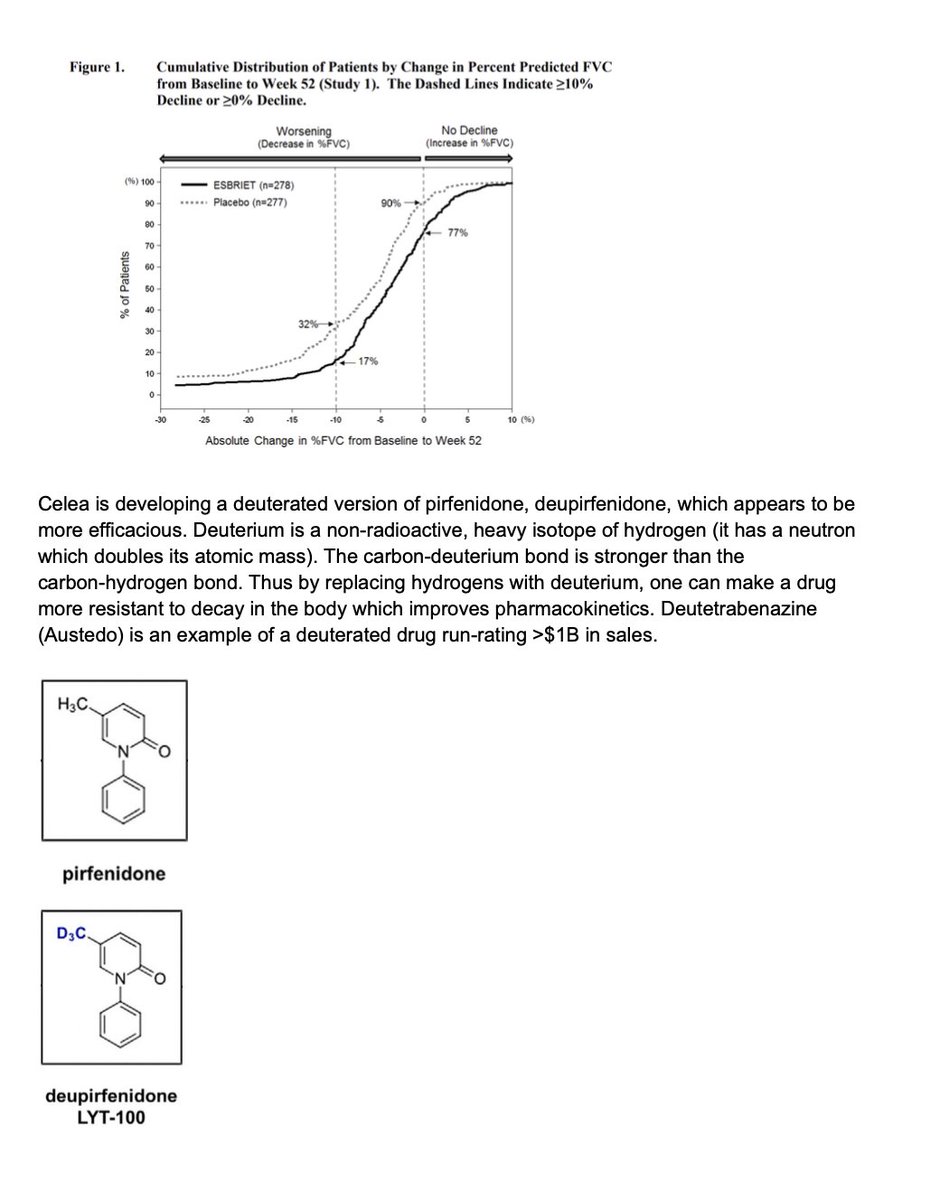

I think Seaport Tx's (PRTC owns 35% plus MSD royalties) MDD trial has a good chance to hit.

I think brex/zuranolone works in MDD but $SAGE was flew too close to the sun with a 2wk PEP because that worked in PPD (but the MOA is a better fit for PPD). Seaport PEP at 6wks is the proper trial design.

PRTC also owns a clinically validated IPF drug ready for Ph3 (chance to be best-in-class). SpinCo needs to raise. It's a free call option -- if they can't raise and this disappears, still cheap.

PRTC also owns the dregs of the Cobenfy economics (2% royalty above $2B), probably worth $100-200M NPV.

Full writeup here (do your own work)

English

@TweetAwayDK Doses only given til day 14, then thin efficacy dropped off at day 42. That's my point - SAGE should have dosed out to 6wks like Seaport is doing

English

@Vulpescap Appreciate the write-up. Chart seems to show zuranolone is no better than placebo at day 42; doesn't fit thesis that SPT-300 with similar efficacy but 6wk/42 day trial design will work. Pipeline generally feels "me-too", early stage, needs funding. Cobenfy is meh. Tough sell

English

@nikitabier Can't wait for @elonmusk to spam my feed with AI videos again

English

The full power of Grok on the algorithm launches next week. It will be the most important change we've done on X.

English

Is there anything worse than the fckin Lancet subjournals for getting access? Even of these real academic libraries don't even pay for this ass lol

English

@BiotechAutist @a_a_free do you have an opinion on where this trades +/- on PDUFA for tiv?

English

@Vulpescap @a_a_free They actually did. But they told rgnx the same thing.

ir.regenxbio.com/news-releases/…

English

Sorry I waited for this moment to troll you :p because you clearly did some misses on this one and it was 70% that it's gonna be approved. Well done on the previous hits but you got lucky because those companies are already shitcos. DNLI is well managed company and they know what they are doing.

Biotech Autist@BiotechAutist

1/ I’m SHORT $DNLI. They filed a safety study as their pivotal trial in the BLA. This application relies entirely on the clinical assumption that the FDA employs morons who treat uncontrolled substrate shifts like stone tablets from God.

English

@BiotechAutist @a_a_free Getting up to speed on this now, did fda not say that it’s reasonably likely to predict clinical benefit?

English

Stifel definitely sounded constructive, but I think you’re overreading it. Label discussions and late-cycle review are process signals, not approval signals. Companies can be in labeling talks and still get a crl (example: aldx). CDER vs CBER helps a bit at the margin, but it doesn’t change the evidentiary standard. The real questions are still whether FDA accepts CSF HS as reasonably likely to predict clinical benefit and whether the single-arm Phase 1/2 package is awc enough.

English