class

101 posts

I used ChatGPT to create a Python simulation of the approach below gist.github.com/vivek-v-rao/f8…

Vivek V Rao@VivekVRao1

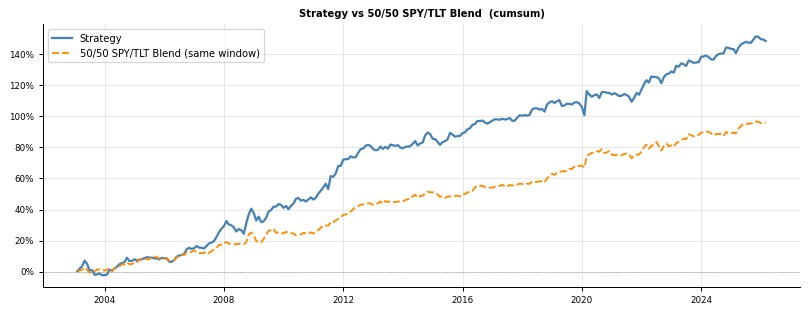

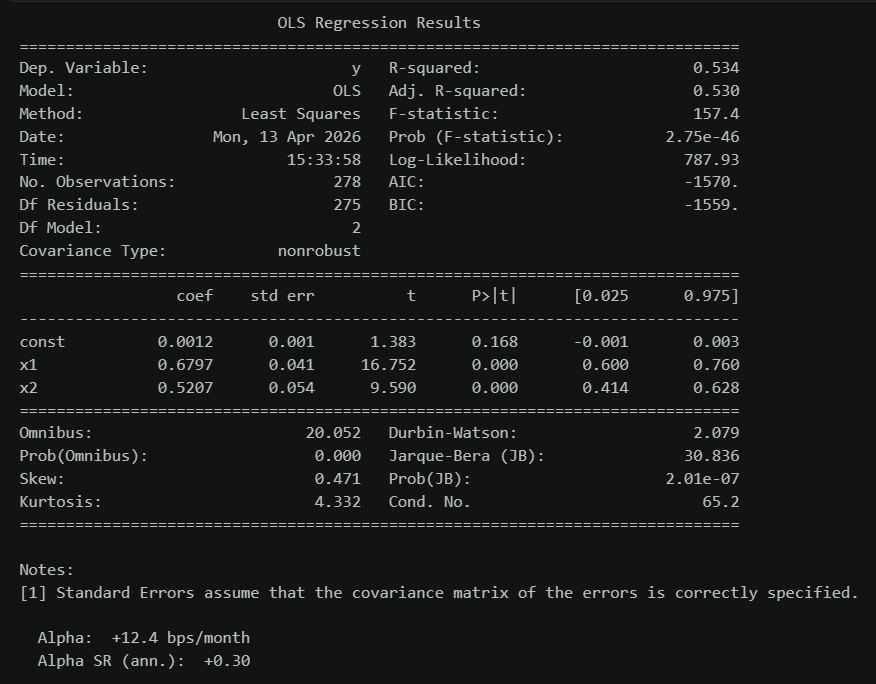

You can use more compute in backtesting in ways that don't incease the chance of overfitting. If I test a trading strategy with ranges for several parameters, I like to also test the strategy with those ranges on random price data, with returns either resampled with replacement or from an IID multivariate normal distribution matching the original returns. If the Sharpe of the best parameter set on historical data is not much higher than the best Sharpe found on random data, that is a warning sign.

English

@therobotjames Nice. How does it compare to just investing $10K in spx over the same period?

English

three dead simple edges in macro etfs you could trade with a goddamn potato.

. . .

if you understand how edge is created in markets, you can do the simplest most neanderthal stuff and make money.

i’m going to show you three dead simple edges that you can trade in spy and tlt.

English

Smoothing usually decreases cov(a,r), as it weights past (less relevant) data more. But, it will also decrease σ_a (noise in your alpha). As long as the σ_a decreases more than cov(a,r), your smoother will boost ic.

TLDR: Smooth alphas to boost ic, let optimizer handle turnover

English

As far as I understand. Smoothing alphas can:

1) Reduce turnover

2) Increase ic

For 1, as ceph points out, an optimizer can do this (and probably should). But an optimizer cannot do 2.

why?

a=alpha, r=return

ic(a, r) = cov(a,r) / (σ_a * σ_r)

Robot James 🤖🏖@therobotjames

@macrocephalopod @NewRiverInvest @robertmartin88 @witchqueendot @stevehouf @Mtrl_Scientist 👋 Say you've got some volatile alpha that explains step ahead returns. And you wanna smooth it cos real world. And you observe decay in IC for increasing half life of smoothing. But you also prefer the more autocorrelated alpha. How do you think about the tradeoff?

English

@SystemicStratHL To push back on the macro view a bit if you look at S&P's forward PE, its ~21x today, which isn't cheap, but not particularly high either.

English

Macro predictions and game plan.

It seems I've been spot on over the past 1-2 years on general trends that played out, so I'll share what I plan to do personally.

1. BTC is going to underperform everything in the medium term.

Reason: BTC has proved itself not to be a good hedge against inflation and world chaos. Nothing new is expected from the 'crypto president' and the next administration probably won't be as complacent. Also, DATs are going to have to sell their leveraged BTC at some point. It's still a long way to go, but everyone is watching and knows it will come eventually.

2. US stocks are probably going to find a reason to have one last rally to ATH or near it — just enough to trigger some final momentum buying before the rope is cut and we start the generational crash we thought could never happen again.

Reason: The Iran situation is going to have a very significant impact on inflation. This will make it very unlikely for the FED to be able to cut rates in the short/medium term. Investors are going to realize that 1) stocks are overpriced (high PE ratios, leverage, etc.) and 2) there is no safety net anymore. So it will naturally fall. Then, in the medium/long term, the FED will be forced to lower interest rates, print again, and we will probably recover some — to the detriment of the USD.

Game plan:

> Short BTC (self-evident)

> Wait for a new ATH on stocks or a few months trading near ATH with momentum funds buying in, then start buying volatility ETFs as they will compound nicely in a crash (e.g. VXX)

> Buy up gold and silver on pullbacks, as they should outperform due to global instability and the medium-term resumption of money printing.

Thinking about how to engineer a vault that could reflect this view, and offer some added alpha to it.

Would it be something you would be interested in?

Also lmk where you think I'm wrong in my view 🙏

English

@stalequant By "sees" the TWAP do you mean with public or non-public information?

English

So nice to have a conversation with your entire second brain and query notes with natural language rather than page through search bar results with CTRL+F + click (or page through physical paper notes)

English

@m1ha313 @systematicls cache consistency like making sure its not stale?

English

@systematicls The hardest thing in computer science are “cache consistency and naming things”

English

I wish I was better at naming articles, maybe some provocative, like:

"There are lessons in here every quant should want to know"

sysls@systematicls

English

@midpricedog Why is this simpsons paradox? Are men applying to easier departments to get into?

English

WaPo writer never heard of Simpson's paradox. Why am I not surprised …

The Washington Post@washingtonpost

Brown University accepted nearly equal numbers of male and female students, but got almost twice as many female applicants. That math meant it was easier for men to get in. Trump's DEI ban may end gender balancing efforts that often benefit men. wapo.st/3MjaLOK

English

@classpath Hi! Currently working on something similar. Can I DM you?

English

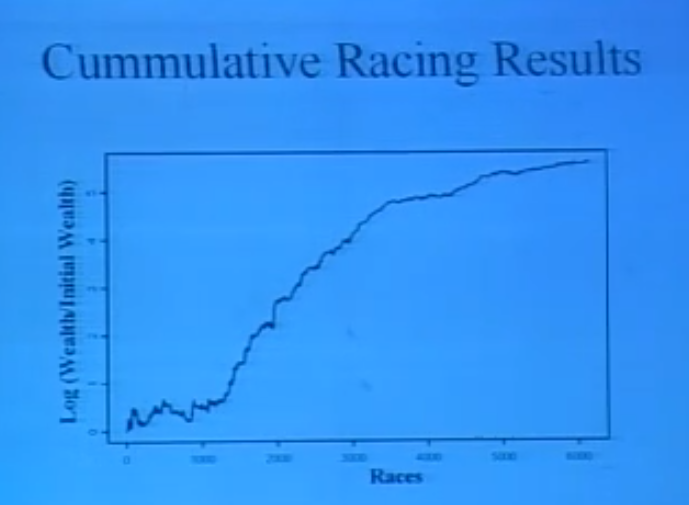

@midpricedog his equity curve so good he puts it on a log scale. Link: youtube.com/watch?v=YOVrZr…

YouTube

English

See also: The Gambler Who Cracked The Horse Racing Code. archive.is/mtL1h

Its funny seeing Bill Benter mentioned after all these years. ~7 years ago, I read about this guy Spring semester in my sophomore dorm room, 1 month out from starting my SWE internship at a OMS/EMS vendor. I was absolutely enamored with his work and read the article multiple times. It was a major spark for further reading and my career path.

fdf@0xfdf

@bennpeifert Instead of a book, I would suggest William Benter's "Computer Based Horse Race Handicapping and Wagering System: A Report". It's a short, 16 page paper. It's a better first course in the spirit and practice of quant trading than almost all books about actual quant trading.

English

Hyperliquid and Polymarket both have markets on Monad's token price, one as a perp, the other a binary.

The two prices move in interesting ways.

Observations:

1. Volatility realized by Hyperliquid's contract (15-minute bars) was much higher at listing, but converged with Polymarket contract implied volatility after the first week of trading.

2. If you use Hyperliquid to construct an implied price for each Polymarket contract from current price and RV, the price paths are similar.

3. Under this simple model, both Polymarket contracts have either been too expensive or pricing in a jump on day of listing.

4. However, the realized volatility on Hyperliquid's contract should be suppressed by the way they charge funding.

It's risky to short Hyperliquid's pre-launch contract because of the mark price used for liquidation. (See: XPL.)

Because of this, it plausibly trades at a slight premium. This would mean the Polymarket contracts are pricing even higher odds relative to Hyperliquid.

5. Even so, the odds of listing above 6B have been steadily decreasing.

English

If anyone wondered why I’ve been posting less actively for the last year or so — it’s because I think I’ve said nearly everything that I can say on the topic of quant finance.

I started posting ~5 years ago because I thought there was a big gap between what I was reading on twitter, and what is common knowledge among experienced quants in industry.

I think my posts narrowed that gap somewhat, as well as others like @__paleologo, @0xfdf and @systematicls.

I don’t have anything to sell, and if I continued posting about quant topics I would either be repeating myself or revealing proprietary information. I have no wish to do either.

So consider this a soft goodbye — I’ll still be reading and I’ll still reply, but I probably won’t post anything new on the topic of trading. If I ever write about it again it will probably be long form as that seems more appealing than farming likes on twitter.

Gappy (Giuseppe Paleologo)@__paleologo

I don't believe I have posted anything *remotely* practical in one year. I think @macrocephalopod has slowed down too. @moreproteinbars and @QuiteMidlife outdo each other posting food pics with occasional war stories; @bennpeifert also really got tired and busy. As for @Gingfacekillah, his books are where it's at. @0xfdf went silent. @KrisAbdelmessih at least has a good substack. And then "traders" (on those lists!) on X are perhaps *too* practical. As for actual professional traders and PMs, all lurkers: not one of the those I personally know posts. Maybe we're all worried about the coming of the Antichrist, but it sure feels like X is in the shallows. Things evolve. Personally, having both time and permission, I'd rather write a substack.

English

@stalequant How does credora calculate p(default)? If its a function of APY then that would explain the good r^2 but not necessarily mean its correctly priced.

English

Suppose you stop adding new features to your mode model and just run it live with no manual intervention:

- how long before your sharpe halves?

- how long before your sharpe goes to zero?

Or equivalent:

- how quickly does your model need to evolve to maintain the same sharpe?

English

A short thread with lots of questions on “research decay”, something that has occupied my mind a lot in the recent period.

English