@Askash Cape Town really said: “traffic on the N1 or traffic on the Atlantic… your call"😁

English

Casey Sprake

74 posts

@CaseySprake

Market Strategist at AG Capital. Translator of global macro trends into actionable investment insights. Always asking "what if" to manage risk and cut noise.

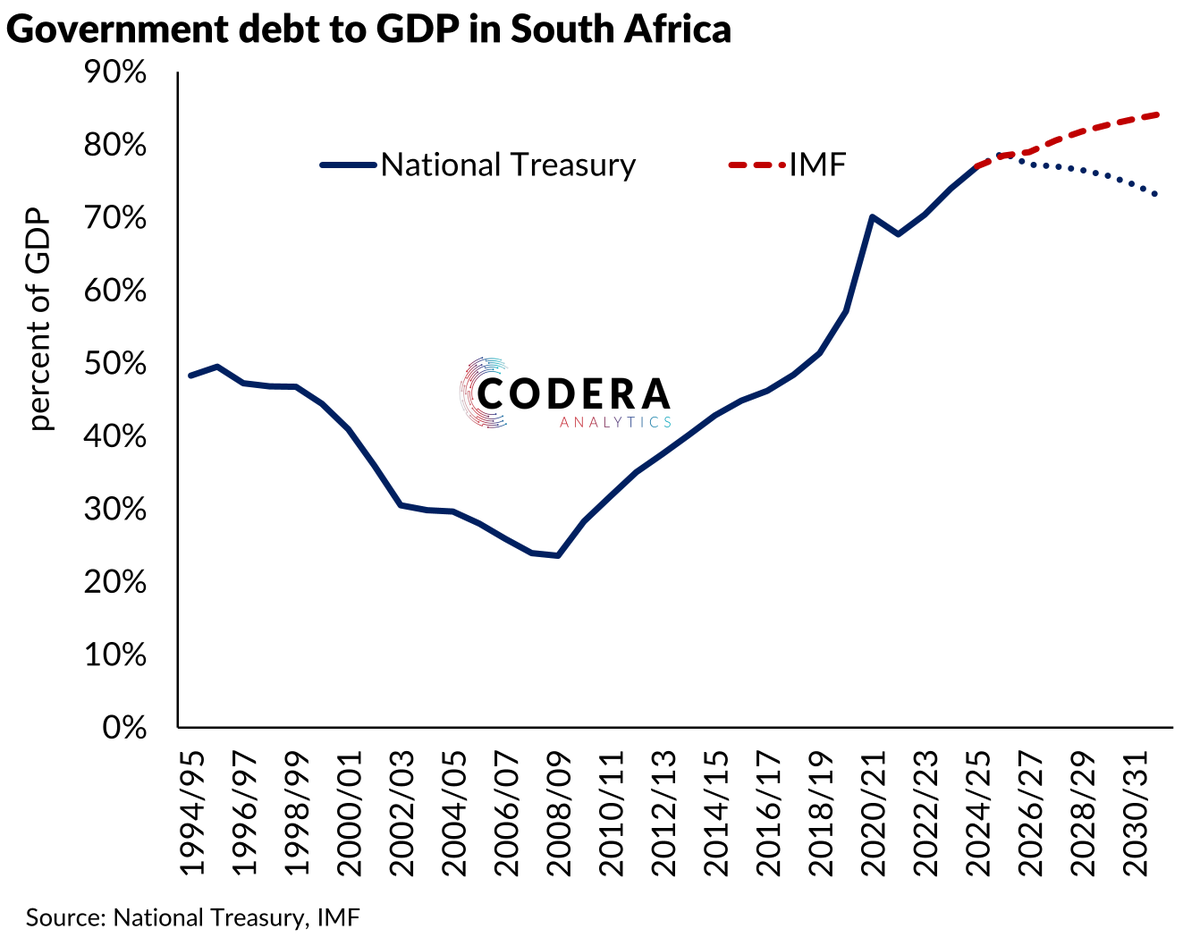

While the National Treasury of South Africa has projected debt to stabilise, the latest IMF projections (published 11 February 2026) continue to imply that debt will not stabilise. @CoderaAnalytics

South Africa’s economy showed resilience in 2025, but growth remains too low to reduce unemployment decisively. A simpler, more predictable licensing and permitting system could help unlock investment and job creation. Read our Country Focus for more: imf.org/en/news/articl…