@Jebaim3 It is trading as if it won’t. Expectations and sentiment are at rock bottom levels. And that is exactly where the alpha is. Zoom out, the story and potential is very much intact. $eose

English

Tim Apple 🔋🔋🔋

352 posts

EXCUSE ME

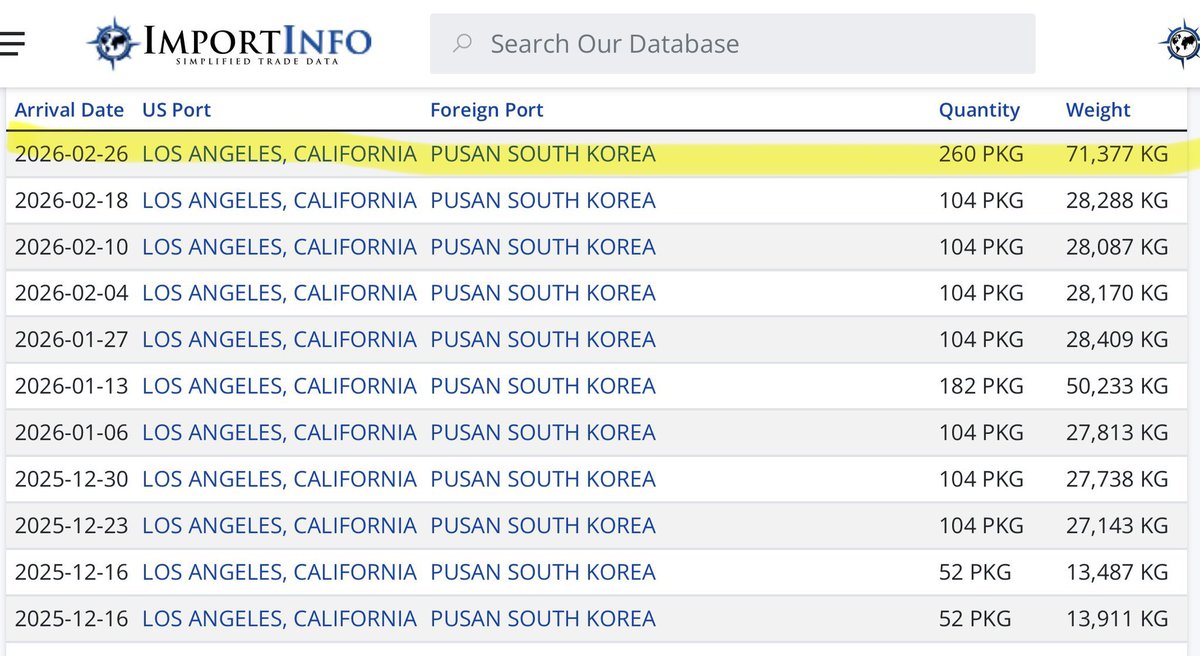

$eose after some thought and discussions- this very well could have been a simple we are going to trust John Mahaz and towards the end of the quarter John told Joe and Nathan hey guys we have to shut it down as we have a ton of issues that have been discovered and we cant ship these batteries- These problems lasted for several weeks into January and only once resolved management wanted to get the call out of the way as fast as possible- As John said he underestimated things and took full accountability and thats all there is to it, 1st generation automation sucking ass and nobody realized it till the head chef pushed it to capacity and saw the lack of repeatability John was handpicked by Cerb and Joe and Nathan followed his lead on production timelines- He has never built a battery before- although its probably the simplest thing he will ever build It sucks- but in the end of the day its just a setback- there is way too much good going on behind the scenes I think they can now (if they havent already) sent Nextera perfect batteries and everything will be glorious again- this will also make line 2 way more efficient out of the gate, I dont believe them that it will take 2 full quarters to ramp, I think they sandbagged everything as they knew that was the only way to regain momemntum moving forward Let the line pump and the orders flow !

$EOSE Q4'25 Review 1/n Core Framework: Where Did the Money Go? COGS breaks into two types: Fixed (paid regardless of production) and Variable (scales with every kWh produced). Each of the three operational failures hit a different layer. ─────────────────── Problem 1 — Downtime: 35% actual vs 10% target When the line stops, workers are still on site, depreciation still runs, factory overhead still accrues. Zero production, full cost. Q4 fixed cost base (est.): Total COGS: $112.4M (official, 8-K) Adj. COGS (ex D&A/SBC): $107.1M (official, 8-K) D&A in COGS: $4.7M (official, 8-K) SBC in COGS: $0.6M (official, 8-K) Est. fixed portion (~45%): ~$50M 25 excess downtime points = ~$14-17M in fixed costs paid for zero output. Volume impact: Actual: 65% utilization → ~227 MWh shipped Target: 90% utilization → ~314 MWh Delta: +87 MWh just from fixing downtime Revenue impact: 87 MWh × ~$256/kWh ≈ +$22M left on the table ────────────────── Problem 2 — Bipolar Yield Failures Every defective bipolar plate = materials consumed + labor spent + no sellable product. Rework means paying twice. Scrap means writing it off entirely. Target: 97% first-pass yield (official, Q4 earnings call) Actual: est. ~80-85% (Jan'26 target achieved = large improvement) Per 100 units needed: @97%: 103 attempts → 3 scrapped @83%: 120 attempts → 20 scrapped Delta: 17 extra units of wasted effort per 100 Material + labor waste: Est. direct material ~55% of COGS: ~$60M Bipolar plate: critical high-cost component ~15-17% overconsumption: ~$7-10M material waste Rework labor: ~$2-3M Total bipolar waste: ~$9-13M ─────────────────── Problem 3 — Supplier Outage: 1 Week Lost Line stopped. Fixed costs kept running. 1 week = 1/13 of the quarter = 7.7% of quarterly capacity Fixed costs for 1 week: ~$50M / 13 ≈ $3.8M stranded Lost production capacity: ~35 MWh Revenue impact: 35 MWh × $256/kWh ≈ $9M ─────────────────── The Amplification Effect — The Hidden Layer The three problems above didn't just create direct waste. They forced the same fixed cost base to absorb across far fewer units. Actual output: 227 MWh → fixed burden ~$220/kWh Target output: 357 MWh → fixed burden ~$140/kWh Gap: $80/kWh × 357 MWh = ~$28M excess COGS This $28M wasn't new spending. It's the cost of underutilization — the same infrastructure, penalized by fewer units to spread across. ─────────────────── Summary: What Was Wasted Excess downtime fixed costs: ~$14-17M Bipolar scrap + rework: ~$9-13M Supplier outage fixed costs: ~$3-4M ─────────────────── Total direct waste: ~$26-34M Lost revenue (3x Q3 promise miss): ~$33.5M (official) Fixed cost amplification: ~$28M (derived) ─────────────────── "What If Everything Had Gone to Plan?" Target scenario Actual (official) Revenue: ~$91.5M $58.0M COGS: ~$91M $112.4M Gross profit: ~$0 to -$5M -$54.4M Gross margin: ~0% to -5% -93.8% ─────────────────── The fixed infrastructure for a profitable quarter was already in place. The output wasn't there to justify it. Same factory, same headcount, same depreciation — just 130 MWh short of where the math worked. All three issues confirmed resolved by January 2026. $EOSE

*Trump Administration Considering New National-Security Tariffs on Half a Dozen Industries, Sources Say -- WSJ *New Tariffs Could Cover Power-Grid and Telecom Equipment, Large-Scale Batteries, Other Industries, Sources Say -- WSJ

$EOSE super calm going into earnings. Market is heavily underweight imo. There will soon be a flight for certainty in this AI world. We dont know how software will evolve. We do not know how the job market will evolve. - But the constant in all this is: we will need more electricity. Even if AI were to magically disappear tomorrow, we would still need more electricity and modernizing the grid. If AI takes over the world, electricity demand is exponential. Flight to certainty will happen and electricity equipment suppliers will be among its biggest winners. FEOC compliant, supply-chain resilient, backed by Secretary of Department of Defense companies will have an out-sized benefit imo. Sentiment is currently trash in the stock. Management has been silent, but I have very little doubt they've been executing like hell. Earnings date was brought forward one week. My belief is they will not come empty handed. Lots of progress throughout the company and externally in the environment they operate with. Thursday cant come soon enough, dying to hear from first source what the company has been going through and their positioning and expectations for 2026-2028. In the meantime, patience.

Solar and battery storage combined drove 81% of new U.S. grid capacity in 2025. 32.5 GW solar + 18.2 GW storage = 50.7 GW of zero-fuel infrastructure. The grid isn't choosing renewables anymore. It's economically opting to - with Texas leading the way

JPM on FLNC: "The company said that that its data center pipeline stood at 30 GWh, ~80% of which having originated since the end of September, suggesting quite the pickup in a short period of time"