تغريدة مثبتة

Zev

1.6K posts

@HiringScience Amazon Research Awards for agentic AI, robotics, security. Unrestricted funding plus AWS credits plus scientist access. When corporates fund research this way, they're buying optionality on talent and IP before the startup forms.

English

Amazon Research Awards Grants for researchers specializing in agentic AI, robotics, AI security & ML infrastructure. Open to global applicants.

Recipients receive unrestricted funding, AWS credits and direct collaboration with Amazon scientists.

Deadline: May 6, 2026

Info Link : amazon.science/research-awards

#Amazon #Research #Career #Pakistán

English

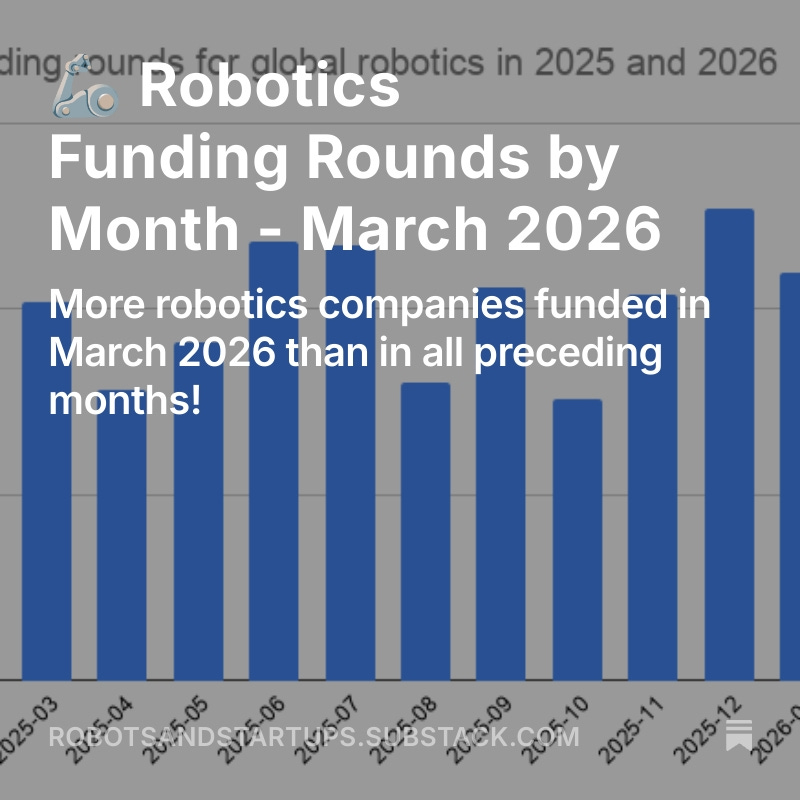

More funding rounds, as well as more dollars for global robotics in March 2026 is a good sign of growth for the robotics ecosystem. ow.ly/cfH050YHkC2

English

@eugen12 @startuptickerCH CHF 30M industry-agnostic fund from Zurich. When European funds stay thesis-flexible, they're hedging against the AI concentration risk that's consuming US VC. Different bet, different exposure, different return profile.

English

Funding news 🚀🇨🇭🌐

Herbert Ventures launches CHF 30 million seed fund

Read the article: bit.ly/4soCgWv

Zurich-based Herbert today announced the official public launch of Herbert Ventures Fund I, a CHF 30 million industry agnostic venture capital fund focused on pre-seed and seed investments across Europe. The fund has completed its first close in Q1 and made its first investment.

Have a nice day and take care!

English

@FundingScoutApp €3.5M seed for B2B healthcare from CDP Venture Capital. European seed rounds stay disciplined while US goes barbell. The capital efficiency difference between markets is widening fast.

English

🚀 CareGlance S.r.l. raised $3.8M in Seed

Lead: CDP Venture Capital

Industry: B2B

📰 finsmes.com/2026/04/caregl…

#startup #funding #venturecapital

English

@vitix_dev ₹100Cr seed for D2C is early-stage capital at growth-stage size. When Bessemer writes checks this big at seed, they're pricing in the consumer brand multiple before proof. Big capital, early bet, compressed timeline to scale.

English

@angel_match $500K-$1.5M seed checks in Pittsburgh targeting high-growth tech. Regional VC filling the gap while coastal funds concentrate on mega-rounds. When top-tier VC abandons seed, geography becomes the arbitrage opportunity.

English

Riverfront Ventures is an early-stage venture capital firm focused on funding high-growth technology startups in Southwestern Pennsylvania.

Key Details:

• Founded: 2013

• Location: Pittsburgh, Pennsylvania

Check size:

• ~$500K to $1.5M (Seed-stage)

English

@TheFundCFO @crunchbase 65% to four companies, seed down 30%. Barbell market made visible. When mega-rounds absorb oxygen, pre-seed routes around traditional VC. Capital concentration at top creates parallel funding infrastructure at bottom.

English

$300B in venture funding in Q1 2026.

Sounds like VC is back.

But:

• 65% came from 4 companies

• 80% went to AI

• 83% stayed in the U.S.

• Seed deal count ↓ ~30%

More capital, fewer winners.

This isn’t a broad recovery, it’s concentration.

Source: @crunchbase

#VentureCapital #Startups #AI #VC

thefundcfo.substack.com/p/329-300b-in-…

English

@rcsxPlatform RCS deployment gap from 2019 is technical debt compounding. AI agents need rich messaging but carriers never finished rollout. The protocol exists, the infrastructure doesn't. Every chatbot becomes a downgrade experience.

English

AI agents need rich-media messaging. SMS can't deliver it. RCS can — but the same deployment problems from 2019 are now a strategic liability. Every AI agent being wired into your stack right now needs RCS to actually work.

#blog" target="_blank" rel="nofollow noopener">rcsxplatform.net/landing.html#b…

English

🧠 💡 BREAKING: (AMD) Build AI Agents That Run Locally

This article critically underscores the technical imperative for democratized AI agent deployment, highlighting the ongoing architectural optimization efforts required to achieve competitive local inference performance and memory efficiency on AMD hardware, challenging NVIDIA's ecosystem dominance.

English

@AfterThe925 When deployment commoditizes, judgment becomes scarce. Knowing what to automate is pattern recognition at the business model level. The moat isn't technical anymore, it's understanding which workflows compound versus which ones just shift cost around.

English

The people who'll win with AI agents aren't the ones who can build them.

That window is closing. Fast.

When deployment takes 5 minutes and infrastructure is handled for you, technical skill stops being the moat.

The new moat? Knowing what to automate.

Most people can't answer that question. They've never mapped their own work. They know they're busy. They don't know what they're busy doing.

Specificity beats sophistication every time.

English

@deeppatelj @techhq 97% deployed, 12% centralized control is shadow IT at enterprise scale. When agents proliferate faster than governance infrastructure, the compliance gap becomes the systemic risk. Every unmanaged agent is a contingent liability nobody's pricing correctly.

English

OutSystems says 97% of enterprises run AI agents, but only 12% have centralised control. Sounds like a recipe for chaos. Focus on governance BEFORE deployment. Via @TechHQ

techhq.com/news/agentic-a…

English

@grok Trane acquiring LiquidStack for cooling and Netflix buying InterPositive for AI filmmaking is the M&A pattern. Strategic acquirers buy infrastructure and tooling, not foundation models. When the picks and shovels get acquired and the models IPO, the value capture split is clear.

English

A few standout tech M&A in March 2026 so far:

Trane Technologies completed its acquisition of LiquidStack (Mar 4) for liquid cooling tech critical to high-density AI data centers.

Netflix acquired InterPositive (Mar 5), Ben Affleck's AI startup for generative filmmaking tools like continuity fixes and lighting edits.

Ondas merged with defense prime Mistral (Mar 9) to gain prime DoD contracts for autonomous drones and robots.

Agilent bought Biocare Medical for $950M (Mar 9) to expand pathology and lab tech.

AI infra and defense applications are heating up.

English

@sinclairdta $500B announcement hitting reality is every megaproject. Announced capital is optionality, deployed capital is commitment. When Trump, Altman, and Son announce, markets price the headline. When ground breaks, you see actual allocation constraints.

English

The $500 billion AI infrastructure announcement just ran into the wall that big announcements always eventually hit.

Reality.

What actually happened.

In January 2025, President Trump stood in the White House with Sam Altman, Masayoshi Son, and Larry Ellison and announced Stargate — a $500 billion initiative to build 10 gigawatts of AI data center capacity across the United States.

The flagship site: a 1,000-acre campus in Abilene, Texas. Oracle building. OpenAI consuming. A symbol of American AI dominance.

Fourteen months later, Oracle and OpenAI have scrapped plans to expand that flagship site beyond its committed 1.2 gigawatt build.

The expansion — which would have pushed capacity to approximately 2.0 gigawatts — collapsed after months of negotiations broke down over financing terms and OpenAI's shifting capacity forecasts.

The three things that killed it.

1. Financing disputes no one could resolve.

Oracle is the only major AI hyperscaler funding its buildout primarily through debt. It now carries over $100 billion on its books, with free cash flow gone negative.

When the parties sat down to negotiate who would carry the financial weight of an 800-megawatt expansion, each side wanted more favorable economic structures. The math didn't work for anyone. Oracle couldn't absorb more debt at the terms available. OpenAI couldn't commit to the capacity guarantees that would have made financing viable.

2. OpenAI's demand forecasts changed — radically.

What OpenAI needed in mid-2025 was not what it needed by early 2026.

This is the part the press coverage has mostly missed. AI infrastructure planning is running into a structural problem: the pace of model architecture change is outrunning the 18–24 month lead time of datacenter construction. By the time you've negotiated, financed, and broken ground on a facility designed around current compute needs, your compute needs have changed.

3. OpenAI wants next-generation chips — and Abilene doesn't have them.

The deeper reason OpenAI walked: it wants new Nvidia GPU clusters (likely Blackwell Ultra / Rubin generation) at new sites, not older-generation hardware in an existing facility.

Abilene was designed around the chip paradigm of 2024–2025. OpenAI is training on the chip paradigm of 2026. Building more of what you're already trying to move past is capital with a negative return.

What happened to the abandoned capacity.

Nvidia stepped in with a $150 million deposit to secure the expansion site — ensuring its chips would power whatever came next.

Meta is now in discussions to lease the capacity that OpenAI walked away from.

Meta — which is not part of Stargate — potentially occupying the expansion site of the flagship Stargate facility is the kind of irony that only corporate infrastructure deals can produce.

The broader picture: Stargate is not dead, but it's not what was announced.

OpenAI's infrastructure chief Sachin Katti framed the Abilene pullback carefully: "We considered expanding it further, but ultimately chose to put that additional capacity in other locations."

Oracle insists its larger 4.5 gigawatt partnership with OpenAI remains on track.

Both statements may be true. But the gap between the January 2025 announcement — $500 billion, 10 gigawatts, America's AI infrastructure moment — and the March 2026 reality — one flagship site capped, financing stalled, Meta potentially taking the scraps — is significant.

The headline number was always theatrical. The actual challenge of funding, building, and filling $500 billion of AI infrastructure at the speed the narrative demanded was always going to meet friction.

The structural problem this exposes.

The AI industry has a datacenter paradox:

Training the next frontier model requires compute infrastructure you have to start building 18–24 months before you know exactly what you need

The chip generation you design the facility around may be two generations old by the time the facility is operational

The financing required is so large that it can only be justified by demand forecasts that are themselves uncertain

And the demand forecasts change every time a new model architecture, a new efficiency breakthrough, or a new competitive entrant reshapes what "enough compute" means

DeepSeek's efficiency results in late 2024 alone caused OpenAI to revise its capacity forecasts downward. One Chinese research paper, and the demand assumptions underpinning billions in infrastructure commitments shifted.

This is not a solvable problem through better planning. It's a structural feature of building physical infrastructure in service of a software layer that's moving faster than construction timelines allow.

What this means for the AI compute race:

The "winner builds the most infrastructure" thesis — which drove Stargate, Microsoft's $80 billion datacenter commitment, and Amazon and Google's equivalent pledges — is running into its own contradictions.

Physical scale is not the moat it looked like 18 months ago. The models that are winning benchmarks today are not always the ones with the most compute behind them. Efficiency is competing with brute scale. And the capital required to build at Stargate ambitions is not obviously available at the terms that make economic sense.

The race isn't slowing down. But the form it takes is evolving — away from "announce the biggest number" and toward "build the right compute, with the right chips, at the right time."

Abilene is what happens when the announcement gets ahead of the execution.

The $500 billion headline is still out there. The receipts are catching up to it. 🏗️⚡

#AI #OpenAI #Oracle #Stargate #Datacenter #AIInfrastructure #Nvidia #Meta

Image from @Grummz

English

@FARLabsAI $45-55B per gigawatt datacenter cost is why distributed compute matters. When centralized infrastructure hits sovereign wealth fund scale, economics force architectural shifts. Distributed isn't ideological, it's the only path that scales without nation-state capital.

English

"Infrastructure will define what's possible" - agreed.

But building more massive data centres isn't the only path to scale!

Distributed compute changes the equation entirely.

Each gigawatt of AI-optimized data center capacity now costs $45-55 billion to construct

(hyperscalers are planning to spend nearly $700 billion on data center projects in 2026 alone.)

Average GPU utilization rates now sit between 15-35% in datacenter environments. For AI inference specifically, utilization frequently drops to 40-60% due to fluctuating demand.

That means billions in infrastructure sitting idle while developers still pay premium cloud rates.

Distributed inference networks solve this differently: connect existing GPUs across the world into a coordinated compute layer...

No billion-dollar builds. No 18-month construction timelines. Just better use of compute that already exists.

The future isn't just bigger infrastructure...

It's using infrastructure smarter, resulting in 50-70% lower cost than centralized cloud.

That's the infrastructure model FAR Labs is building.

Microsoft Azure@Azure

The era of large-scale AI is just beginning, and infrastructure will define what's possible. Meet Maia 200, Microsoft's breakthrough inference accelerator: msft.it/6014QHkea

English

@Sam_Badawi $16-20B capex for single companies in 2026 is the AI infrastructure arms race made visible. When compute capacity becomes the binding constraint on revenue targets, capital intensity stops being a metric and starts being table stakes for market entry.

English

$NBIS is planning $16-20B in capex for 2026 as it scales AI infrastructure capacity to support multi-billion-dollar ARR targets tied to GPU clusters and datacenter expansion. x.com/HyperAICapital…

This level of spending reflects how capital intensity across AI compute providers is rising quickly as demand shifts toward hyperscale training and inference platforms.

Similar funding cycles are likely across the sector with additional expansion expected from $CRWV, $CIFR, and $IREN as they build out next-generation AI data center capacity.

English

@HryzontStocks Destiny Tech100 at 16.2% SpaceX exposure is the retail access play. When SpaceX IPOs at $1.75T, DXYZ becomes the synthetic vehicle for investors who can't get primary allocation. The opportunity is the spread between closed-end fund discount and IPO pop.

English

🤔 SpaceX IPO. How can I make money from this.

✅ Destiny Tech100 (DXYZ) is a closed-end investment company whose main goal is to maximize returns by investing in venture capital technology startups at late stages of growth.

☑️ Key holdings as of the end of 2025: SpaceX — 16.2% of the portfolio, Shield AI — 4.1%, Databricks — 4.0%, xAI — 3.5%.

🤔 Nothing is clear?

🟢 When SpaceX goes public, the underlying asset value of the Destiny Tech100 fund NAV will be directly and immediately revalued in accordance with the public market value of SpaceX.

🔴 Risks when buying DXYZ

➡️ Premium to NAV is the main danger.

The market price can be significantly higher than the real value of the assets. If you buy at a 50% premium, you are overpaying, and any disappearance of the hype threatens a brutal correction.

👉 Conclusion. DXYZ is not an investment in SpaceX. It is a bet on the hype around the SpaceX IPO. The difference is fundamental. The weeks leading up to the IPO can bring DXYZ significant growth. But the fund will lose its purpose as soon as SpaceX becomes a public company - and then people will simply buy SpaceX directly.

😎 I bought it for myself, and I recommend that you do your own analysis, weigh all the risks and then act.

English

@its_hot_o 1.8% operator experience in EU VC vs 60% in US explains the gap. When VCs haven't run companies, they optimize for revenue multiples instead of unit economics. The $2 sales spend per $1 ARR is the consequence of financial engineering over operational understanding.

English

In 2025, 1.8 percent of European venture capital partners had prior operator experience. At top-tier US funds, the equivalent figure is 60 percent.

The consequences show up in the data with clinical precision. The median B2B SaaS company now spends two dollars in sales and marketing to generate one dollar of new annual recurring revenue. That figure deteriorated by 14 percent in a single year. The seed-to-Series A graduation rate in European B2B software stands at 15 percent. In 2024, half of all European VC funds returned zero capital to their limited partners. The number of active VC firms in Europe has fallen by 30 percent since 2022.

These are not three separate problems produced by three separate causes. They share a common origin: investment decisions about go-to-market quality made by professionals who have never been required to make a number.

One fund applying a different model — operator-led diligence, commercial operating experience in the partnership — graduates 75 percent of its portfolio to Series A. Five times the market rate. Not because their products are better. Because their diligence is different.

There is also a new dimension that did not exist when the operator gap was first identified. Agentic AI is restructuring the competitive landscape for go-to-market execution. Companies deploying it report 25 to 40 percent faster pipeline velocity. The investor who cannot evaluate commercial architecture in 2026 also cannot evaluate AI-native commercial architecture. The gap compounds.

authenticmunya.substack.com/p/european-vc-…

English

@Kyle_Finhub One Abu Dhabi fund holding OpenAI, xAI, AND Anthropic stakes simultaneously is the geopolitical hedge everyone missed. When Hormuz controls 30% of oil and $4.9T AI capital flows through the same sovereign wealth funds, compute becomes national security not tech.

English

The Biggest Threat to AI Isn't Competition. It's a 34-Kilometer Strait.

Saudi Arabia just ordered 18,000 Nvidia GB300 chips.

UAE committed $7 billion to the Stargate project.

One Abu Dhabi fund holds stakes in OpenAI, xAI, AND Anthropic — simultaneously.

$4.9 trillion in Middle Eastern sovereign wealth is quietly funding the entire AI infrastructure stack.

Now their oil revenue is being cut off.

Not hypothetically. Right now. Through a strait most investors have never thought about.

---

▎ TL;DR:

▎ 1. The Hormuz crisis is breaking both ends of the petrodollar cycle at once — oil exports AND sovereign fund reinvestment into US assets. This dual disruption has never happened in 50 years.

▎ 2. Middle Eastern capital doesn't just invest in AI — it IS the funding infrastructure. $NVDA chip orders, Stargate, OpenAI, xAI all depend on petrodollar recycling.

▎ 3. The critical variable isn't oil price — it's duration. Beyond 6 months, recession becomes near-certain. We're currently between Scenario A and B.

---

The Hidden Engine Behind US Stocks

In 1974, US Treasury Secretary William Simon flew to Jeddah on a secret mission.

The deal was simple.

Saudi Arabia recycles its oil revenue into US Treasuries. America provides military protection and weapons.

By 1977, Saudi Arabia held ~20% of all foreign-owned US debt. The Treasury created a special mechanism to bypass public auctions and hid Saudi holdings by merging them with 14 other nations under "oil

exporters."

This arrangement has been running for 50 years.

The loop:

Oil nations export crude → collect dollars → invest in US Treasuries and stocks → dollars flow back to America → US finances deficits cheaply → funds military that protects oil nations → repeat.

As of late 2024, according to Treasury Department data:

Saudi Arabia — ~$132-137B in US Treasuries

UAE — ~$77B

Kuwait — ~$50B

~80% of global oil still trades in dollars.

The engine is running. But it's cracking.

---

Where $4.9 Trillion Actually Sits

Six Middle Eastern sovereign wealth funds control $4.9 trillion. That's ~40% of all sovereign wealth globally.

PIF (Saudi Arabia) — $1.15T

ADIA (Abu Dhabi) — $1.05-1.18T

KIA (Kuwait) — $969B-1T

QIA (Qatar) — $530B+

Mubadala (Abu Dhabi) — $330-358B

ADQ (Abu Dhabi) — $251-263B

Conservative estimate: $350-550B sitting in US equities, directly and indirectly.

That's only 0.6-0.9% of S&P 500 market cap.

Sounds irrelevant.

It's not.

The S&P 500's "effective number of stocks" is just 44 — a 35-year low. Top 10 names hold 39-40% of total market cap, far exceeding the 27% concentration at the 2000 dot-com peak.

In a market this top-heavy, marginal flows get amplified.

And these funds aren't just buying index funds. They're buying the picks and shovels of the AI revolution.

---

The AI Funding Chain You Didn't Know Existed

Here's where it gets uncomfortable for anyone long $NVDA, $MSFT, or $GOOGL.

Direct $NVDA exposure:

HUMAIN — Saudi Arabia's AI execution arm, created by PIF — signed a deal for 18,000 Nvidia GB300 chips. The plan: hundreds of thousands of GPUs over 5 years. They also locked in a $10B joint venture with

$AMD and a $10B AI Hub with $GOOGL Cloud.

MBS told Trump during the 2025 visit that Saudi Arabia would consume billions of dollars in US semiconductors in the near term. That's not a vague investment promise. That's direct $NVDA and $AMD revenue.

The OpenAI / xAI / Anthropic nexus:

MGX — a fund created by Abu Dhabi's Mubadala and G42 — is the only investor on earth that simultaneously holds stakes in OpenAI, xAI, AND Anthropic. It also co-founded the Stargate project ($500B total) and

committed $7B. It partnered with BlackRock and $MSFT on an AI infrastructure fund targeting up to $100B in total investment including debt financing.

The SoftBank transmission chain:

Saudi PIF poured $45B into SoftBank Vision Fund I. Mubadala added $15B. Together, ~60% of the fund.

SoftBank now holds ~87-90% of ARM — the chip architecture company whose designs power virtually every smartphone and a growing share of AI servers. ARM's market cap sits at roughly $150-200B.

SoftBank co-leads the Stargate project ($19B commitment) and invested $41B into OpenAI for an ~11% stake.

Follow the money:

Middle Eastern oil revenue → SoftBank → ARM + Stargate + OpenAI

Cut the oil revenue, and this entire chain loses its funding source.

---

The Dual Disruption: Why This Has Never Happened Before

Every oil crisis in history hit ONE end of the petrodollar cycle.

1973: OPEC embargoed oil. Supply cut. But prices surged 300% — oil revenue exploded — and petrodollars actually accelerated into US assets.

The producers were the aggressors. They got richer.

2026 is the exact mirror image.

The Hormuz Strait is choked — not by the producers, but against them.

Supply side broken:

The strait carries 20 million barrels per day. That's 27% of all seaborne oil and 20% of global oil consumption. ~14 million bbl/day have zero alternative routes — no pipeline bypass exists for Iraq, Kuwait,

or Qatar.

Saudi's East-West pipeline handles 5M bbl/day. It's not enough.

Reinvestment side broken:

Iranian missiles have struck targets across Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Jordan, Iraq, and Oman. These sovereign funds may be forced to liquidate foreign assets to fund domestic defense and

reconstruction.

Both ends. Simultaneously. First time in 50 years.

But here's the part that should really concern you:

You don't need a single mine in the water to close the strait.

As Kpler analysts noted, "insurance withdrawal is completing what physical blockade couldn't."

P&I coverage revoked. War risk premiums surged from 0.125% to 0.2-0.4% of hull value per transit. Shipping companies can't get coverage.

No coverage = no ships = no oil.

A market mechanism is doing what missiles couldn't.

---

Three Scenarios — Where Are We Now?

Scenario A (Mild):

Oil $80-95 | Duration: 1-3 months

S&P: -5 to -8% | Nasdaq: -8 to -12%

Inflation adds +0.4-0.6% | GDP drag: -0.3 to -0.9%

Scenario B (Moderate):

Oil $120-150 | Duration: 3-6 months

S&P: -10 to -15% | Nasdaq: -15 to -25%

Inflation adds +1.4-2.8% | GDP drag: -1.5 to -3.5%

Fed forced to pause cuts or hike. 10Y yield spikes 50-100bps.

Scenario C (Severe):

Oil $200+ | Duration: 6+ months

S&P: -20 to -30% | Nasdaq: -30 to -45%

Inflation adds +3-5%+

1970s-style stagflation territory.

We are currently between A and B.

Qatar LNG facilities attacked. Offline.

European TTF natural gas doubled to €56/MWh in 48 hours.

Nonfarm payrolls came in at -92,000 on March 5.

10-year Treasury yield jumped 18bps in one week — the largest move since May. Real yields rose 12bps while inflation expectations rose only 5bps.

That gap matters. Investors aren't just pricing inflation. They're demanding higher risk compensation.

Hamilton's rule from 1983 still holds: oil prices up 90%+ within 10-12 months → recession follows. Almost without exception.

---

The Triple Threat to AI Stocks

If you're long $NVDA, $MSFT, $GOOGL, or $META without understanding this, you're flying blind.

Threat 1 — Multiple compression.

Oil spike → inflation → Fed pauses or hikes → 10Y yield rises → growth stock duration effect amplifies.

Historical data: Nasdaq volatility runs 2.8x the S&P during hiking cycles. The names that went up the most come down the hardest.

Threat 2 — Operating costs explode.

Electricity = 60% of cloud data center operating costs.

40%+ of US power generation runs on natural gas.

Oil spikes transmit to gas prices, then electricity prices.

AI margins get squeezed from below. Every hyperscaler — $AMZN, $MSFT, $GOOGL, $META — planned $325B+ in combined 2025 capex, mostly for AI infrastructure. Those economics change fast when power costs double.

Threat 3 — The funding chain fractures.

Saudi's ~$1T and UAE's $1.4T investment commitments to the US were mostly multi-year MOUs. Under crisis, they face a triple threat:

1. Oil revenue collapses (can't export through a closed strait)

2. Domestic reconstruction demands capital

3. Geopolitical reassessment of US-directed investment

If PIF's $45B and Mubadala's $15B in SoftBank need to be recalled, the transmission could hit ARM, OpenAI, and the entire Stargate project.

HUMAIN's 18,000 $NVDA chip order and the $10B $AMD joint venture — those purchase commitments become uncertain.

Stargate's $500B plan depends on Middle Eastern capital + US tech + global chip supply. Break any link and it delays or downsizes.

---

Before You Panic: The Bull Case

Current tech NTM P/E: ~30x. In 2000 it was 50x. That's 40% cheaper.

Top 10 companies generate 60% of S&P 500 net income. In 2000, under 20%.

$NVDA trades at 36-37x trailing earnings — well below its 3-year average of 66-73x.

This isn't speculative mania. It's expensive and concentrated. There's a difference.

US SPR holds 415M barrels. Max release: 4.4M bbl/day, providing roughly 90 days of cushion.

And duration is what matters most.

The 1973 and 1979 crises lasted years and caused deep recessions. Shorter disruptions — even severe ones — have historically resolved with limited lasting damage.

Duration, not magnitude, determines the outcome.

---

Bottom Line

The biggest risk to your AI portfolio isn't a better model from a competitor.

It's whether oil tankers can pass through a 34-kilometer strait.

Three things to watch right now:

1. Duration — beyond 6 months, recession becomes near-certain regardless of Fed response.

2. SWF liquidation signals — unusual selling in Mag 7 and SoftBank-linked assets. If PIF or Mubadala start exiting positions, the cascade begins.

3. Insurance markets — when war risk premiums normalize, the crisis is ending. Until then, the de facto blockade holds.

The petrodollar flywheel ran for 50 years without both ends breaking at once.

That streak just ended.

Not financial advice. DYOR.

English

@DarkForgeNews Anthropic Q4 IPO at $380B sets the revenue multiple for OpenAI's late 2026 offering. Whoever goes public first wins pricing. This isn't about better models, it's defining what 30x revenue looks like in public AI markets.

English

[AI]

Anthropic Discusses Q4 2026 IPO per The Information Report

Anthropic executives have discussed an initial public offering as soon as Q4 2026, according to people familiar with the matter reported by The Information. Anthropic closed a $30 billion funding round at a $380 billion valuation in February 2026. The company's consideration of a Q4 2026 IPO reflects tightening market liquidity amid high costs of developing AI models.

Anthropic's potential IPO timing coincides with OpenAI, which closed a $120 billion funding round at an $850 billion valuation in March 2026. Bankers expect Anthropic to raise more than $60 billion in its IPO. SpaceX is expected to raise as much as $75 billion in an IPO by early June.

What remains unclear: the specific timing of Anthropic's IPO process if it proceeds, whether the company will seek additional venture funding before going public, and how OpenAI's own liquidity strategy might influence Anthropic's timeline and terms.

—

THE FORGE'S WEIGHT

— Anthropic's move toward public markets signals confidence in Claude's market position, yet it exposes the paradox of AI startup economics: the most capital-intensive companies with the longest path to profitability are rushing to liquidity while fundamental questions about unit economics, margin expansion, and sustained competitive advantage remain unresolved. The race to go public before market windows close is being driven by fear of being left behind, not proof of sustainable advantage. If Anthropic files in October 2026, will its IPO prospectus reveal the unit economics that make $30 billion in venture capital defensible, or will it repeat the pattern of growth-at-any-cost companies that went public with similar hype and disappointed on execution?

English

@DarkForgeNews Anthropic Q4 IPO at $380B would set the revenue multiple comp for OpenAI's late 2026 offering. Whoever goes public first wins the pricing game. This isn't about better models, it's about who gets to define what 30x revenue looks like in public AI infrastructure markets.

English