AlphaHungry

380 posts

AlphaHungry

@AndrewTakes

Long / short equities. Here to learn. Striving to earn.

Beigetreten Temmuz 2015

1.3K Folgt212 Follower

Welcome to our side @ContrarianCurse

SuspendedCap@ContrarianCurse

In semi cycles past, supply comes up in steps and demand follows an S-curve, usually. Eventually the plateau comes, the step outstrips demand and it all comes down I’m long semis majorly right now. More than in a long time because it occurred to me this is the first semi cycle, ever where bringing on supply (compute) is still directly tied to unlocking new capabilities which serves to pull up and retether demand. This has never occurred before. If TSM brought on too much supply, iPhones didn’t just suddenly accelerate as a result of that. I’m not entirely convinced we won’t blow up some point, but if things *were* to be different - this is how

English

@michaelsikand That's a misleading slide. . The SiPh CPO stops at 200m of surface area in the switch.... but you have upwards of 30 transceivers plugged in * 50mm SiPh per = 1.5K surface area which won't need SiPh content anymore w/ CPO (IE Soitec wafers)

English

$1T markets are for suckers.

The $0 markets are where the multi baggers live.

Co-packaged optics (CPO) is the future of AI networking. $0 to $20B market by 2036 (IDTECHex).

I'm patient, so I decided to front-run the CPO market into Soitec $SOI.PA / $SLOIF.

Every CPO switch, whether it is NVIDIA’s Spectrum-X, Broadcom’s Davisson (TH6), or Marvell’s Celestial AI Photonic Fabric, needs Soitec's Photonics-SOI wafers.

Right now, silicon photonics is a small fraction of Soitec's revenue. But check out this 2024 PPT slide from them.

With the rise of CPO, photonics SOI content per chip QUADRUPLES.

Finding that asymmetric lever in the technology is the fire step to identifying asymmetry in a stock.

English

@institLPGP do you like $msft in this context which has sold off hard?

English

couple things

1. Pls dont takeaway leading models in Claude code pro plan

2. If anthro thinks the window for massive consumer surplus is over:

A) they see enterprise taking off

B) compute deficit and GPU prices to leap

C) ai infra moon $nbis $stx $asml $acmr $nvda

ℏεsam@Hesamation

Redditor claims Claude Code is nerfed for Pro/Max users vs Enterprise customers and the strategy is to use the paid plan users to generate hype on X and LinkedIn so companies would reach out to them.

English

@lazereater @Randall7575 Invert man, judging by the writing style of Randall's responses, it looks like an LLM is writing those for him. Wouldn't give him the time of day.

English

@Randall7575 Wrong again Randall. $celh pays them every year. I think you should take a little time to research what you are talking about before you share your profound insight.

English

$TPB

7-Eleven shelf ≠ demand.

If it takes slotting fees + discounts to move cans,

that’s not growth—it’s bought velocity.

English

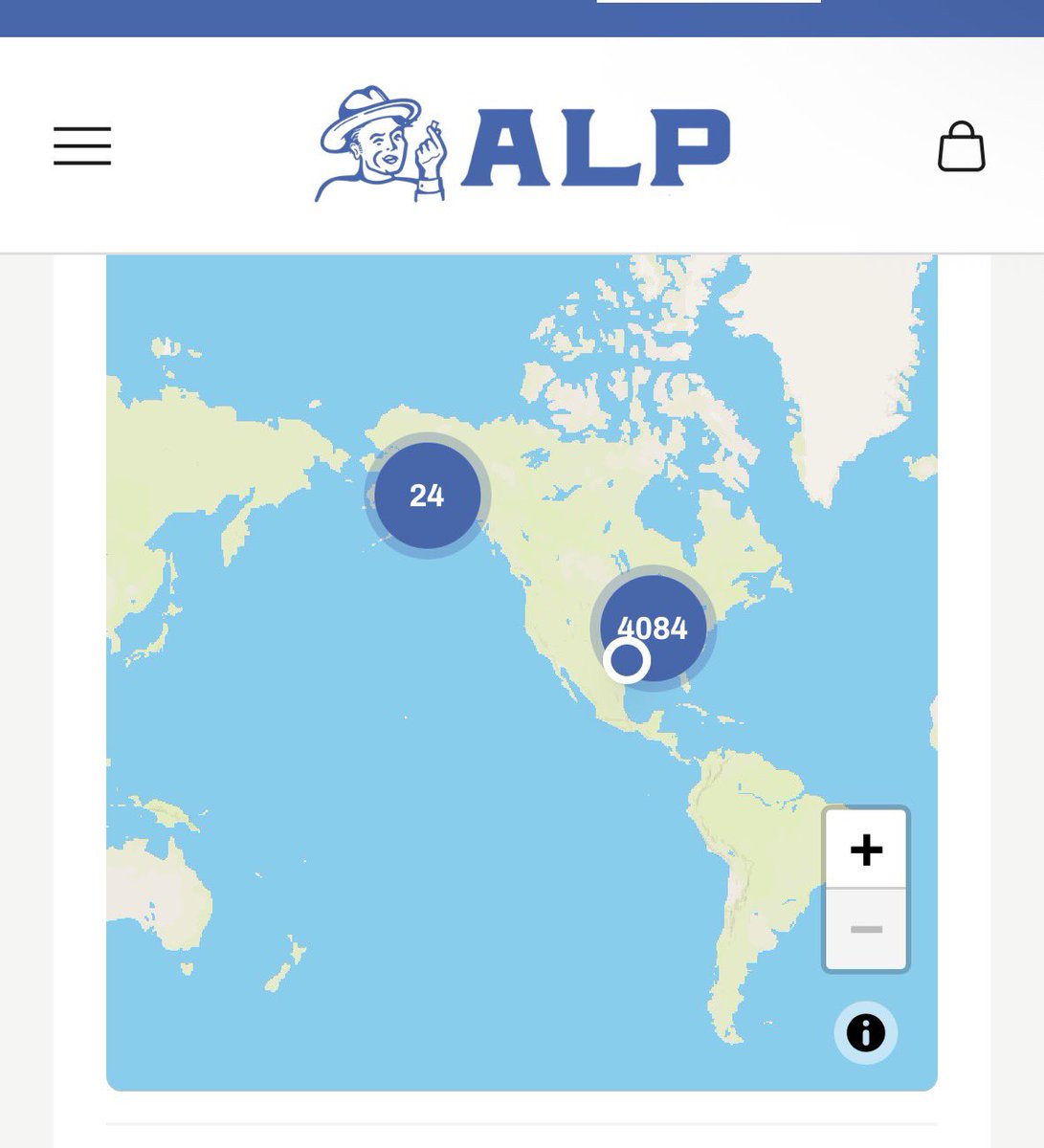

@OnodaCapital No concerns on the Trump <> Tucker feud right now effecting ALP's approval?

Tucker said on a podcast a few weeks ago the CIA is building a case against him for being in contact with certain ppl in Iran before the war started

English

$TPB will go +75% if they just do any of the following:

1. Have Tucker call RFK

2. $1M to the ballroom

3. Don Jr on the board

But they’re a top decile slimy management team so can’t go big

Hiroo Onoda@OnodaCapital

People really think the RFK FDA gonna take nicotine pouches off the shelves?

English

@hcapinvesting Agree there won't be a full NP ban and ALP+FRE being in fast-track is a positive, but I fear this Trump <> Tucker feud could influence the decision on ALP.

English

$TPB: (3/3) The bottom line for me is that the fact that TPB was included in the fast-track program together with PM, Altria and BAT is a huge validation point. It’s hard to envision a full NP ban. End result could be that only these get approved while independent brands do not

English

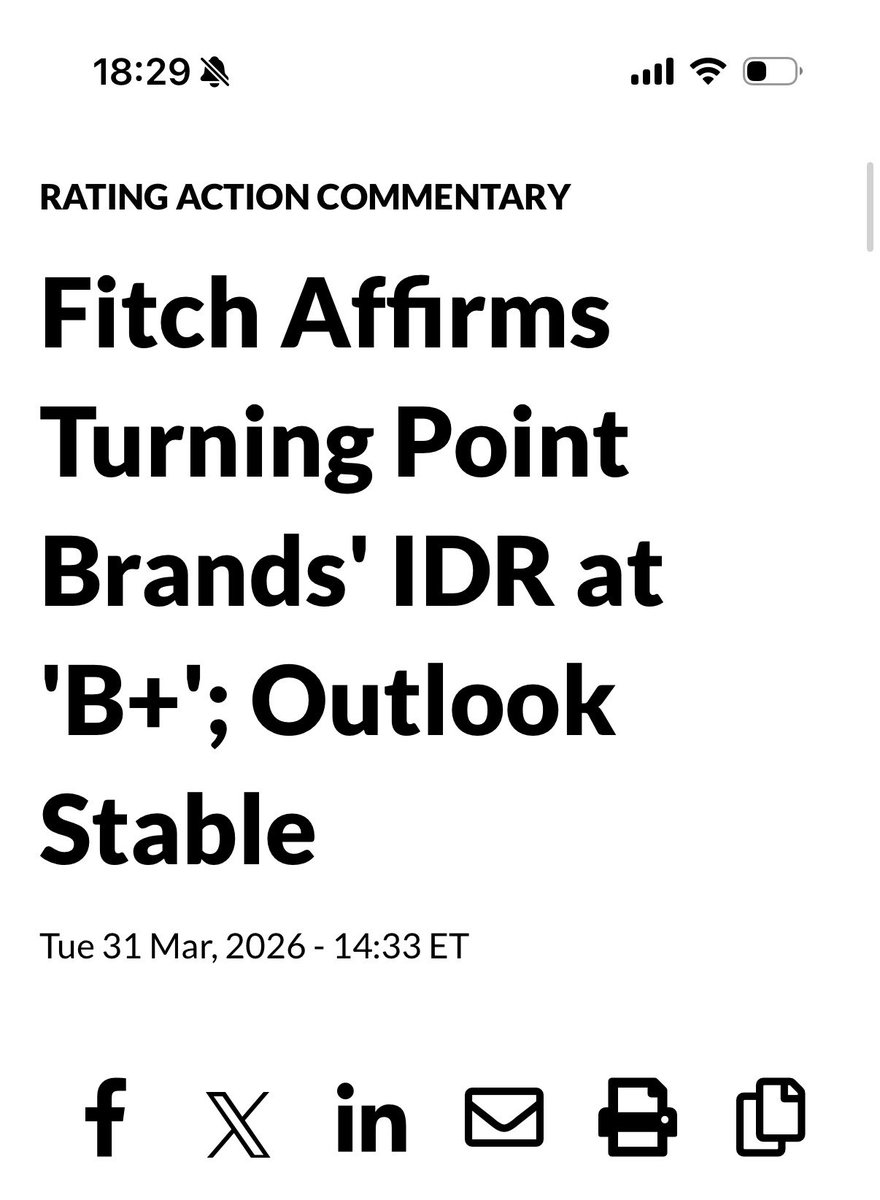

$TPB: (1/3) TPB being hit with a little bit of a triple whammy the last 24h: Reuters article creating uncertainty around FDA approval, France imposing ban on nicotine pouches effective today and Fitch rating adding more weight to legislative risk as product mix shifts

English

@anonymouskeepit and i think a 12x multiple is generous when you see how it traded b4 NP

English

@anonymouskeepit what's your math on getting to $45 / share on base biz? I'm more like $2.50 base biz EPS 12x = $30

English

Is $TPB not a buy here? Legacy business is ~$45 a share which means the market is valuing the Modern Oral business at ~$500M or just ~2.5x 2026 net revenue that's growing >100% yoy. FDA report just says delay vs denial. Delay means they can still sell but just can't advertise.

English

@lazereater @themateuszcaban Also the current Trump <> Tucker feud puts ALP directly in the crosshairs. I've sold out for now.

English

@lazereater @themateuszcaban yeah but doesn't this put ALP and FRE approvals completely at risk now that fast-track is slowed down?

English

@ContrarianCurse It's time for you to get stuck in long here on memory. It's fkn time

English

$MU k now its getting more interesting.

For context, in 2018 FY EPS was $12, and street is at $98 for CY27. Y'all need to understand how retarded that is, even if this is a unprecedented cycle

That being said, by end of 2027 you will be around $200/share in BV if this pans out. Let's say it misses and ends at $175 to be conservative

Bull case is then that HBM is a narrower band for margins (maybe oscillates between 30-60% due to customer concentration, offset by need to secure supply and desire to dictate specs) while the rest keep the old attributes. Capital destruction phase of the cycle gets eliminated and capital gets returned at higher rates than the past. I don't think its a tough bull case. I can see it

Doubt with that possibility in the ether, the investor base here now having an avg IQ of 52 that we get below BV again, so let's say a 1.2x = $210 floor. You guys give me another day or two like this and improve the skew, I'm prob in

English

reminder that Lamb Weston (the Atlassian of potatoes) reports this week

English

@ContrarianCurse dude it's a structural chokepoint through 2029, maybe even 2030

English

$MU getting to 500,$600+ isn't going to come from larger earnings or GMs at this point.. you may never see these levels again

Its going to come from a structurally higher floor for margins

English

@MoodyWriter13 Based on your checks the over shipping / inventory glut view is not true either?

English

The only thing I can confirm here is the near-term RF-SOI cycle pressure. The rest is factually wrong or heavily distorted. GlobalWafers has zero qualified customers for its tech, which can’t deliver sub-100nm thin films for photonics. The Siltronic comparison is laughable.

Silicon Capital@SiliconCapital8

$SOI — Sharing the Short Case I’m Hearing, Help Me Stress-Test It Soitec’s stock has been marching to the beat of its own drum lately, and unfortunately, not in harmony with the rest of my photonics stock investment portfolio ($TSEM, $AAOI, $GLOFO, $AXTI, $LITE, $COHR, etc). After a few rounds of conversations with institutional fund contacts, I managed to stitch together the short case on $SOI that’s currently making the rounds. Most short theses I run into sound smart but don’t survive reality checks. This one felt more credible than most, though I’d love to pressure-test that view with others. Since X seems to be a main venue for $SOI and photonics discussion, I figured I’d start here. Curious to hear what the community thinks, especially where you agree, disagree, or see blind spots in the short case that seems to be pressuring the stock. $SOI Soitec short thesis: 1/ Smartphones: When Memory Gets Tight, RF SOI Gets Squeezed Historically, 60–80% of Soitec revenues have ridden on the smartphone train, while photonic SOI, the supposed future cavalry, still contributes only ~10–15% to revenues. Translation: when smartphones catch a cold, Soitec ends up on life support. The shorts are pointing to SemiAnalysis’s recent warning that “smartphone builds could fall as much as 50% YoY in 2027 due to memory shortages” (youtu.be/PLdT0lzf3Ks). OEMs locked in 2026 memory allocations back in 2025, but 2027 capacity remains frustratingly unsecured, forcing handset makers to trim builds and quietly push any real recovery further into the distance, likely 2028, maybe even 2029 (trendforce.com/news/2026/03/1…, eu.36kr.com/en/p/372552137…). Meanwhile, memory suppliers aren’t exactly offering reassurance. Hynix now suggests the shortage could stretch beyond 2030 (cnbc.com/amp/2026/03/20…). At that point, it stops looking like a temporary bottleneck and starts resembling a structural headache. No handset recovery means no RF SOI demand rebound, and that likely keeps mid-single-digit annual RF SOI price declines grinding away at margins, the slow, methodical erosion kind, not the dramatic cliff-drop kind. Even under generous assumptions, the math refuses to cooperate. Soitec is expected to be only marginally profitable in 2026, and even if smartphone volumes decline a milder 30% in 2027, offset by a heroic 50% photonics growth assumption, roughly 2x management’s own 20–30% guidance, the result still points to negative revenue, earnings, and profit growth. The shorts point to May 23rd earnings which could be the moment where reality meets expectations. A new management team eager to rebuild credibility may decide the fastest path forward is to reset mobile expectations downward, loudly, clearly, and all at once. 2/ Competition from Global Wafers confirmed, Soitec might not be a monopoly after all For years, the bull case quietly assumed Soitec had the SOI crown more or less locked down. The shorts, however, are now asking whether that crown was ever as secure as advertised. Enter GlobalWafers, one of the world’s heavyweight silicon wafer producers and a key supplier to TSMC, Tower, and GlobalFoundries, armed with a deep R&D wallet and, apparently, a willingness to go off-script. The company has terminated its Soitec license and plans to ramp 300mm photonic and RF SOI wafers from 2027 onward using its own IP. CEO Doris Hsu didn’t exactly whisper the message either. She stated last week that GlobalWafers can “make SOI wafers without Soitec IP” and is already moving through customer qualification (mins 1:09:09: finance.yahoo.com/quote/6488.TWO…). Adding fuel to the narrative, GlobalWafers has just completed a new U.S. SOI facility in Missouri, backed by government support (nist.gov/chips/globalwa…). In other words, this isn’t just a PowerPoint ambition, it’s bricks, mortar, and capex already sunk into the ground. If GlobalWafers successfully enters the market around 2027, after wrapping up customer qualifications this year, the implications stack quickly: pricing pressure, market share erosion, and royalty risk, arriving as a three-course meal, not separate appetizers. And perhaps the more uncomfortable question lurking beneath the surface: if GlobalWafers can walk away from licensing fees, what stops other Soitec licensees, like Shin-Etsu, from eventually asking the same question? Because once one player proves the exit door exists, others tend to check whether it’s unlocked. 3/ Silicon Photonics: Growth Story… With a Side of Inventory Hangover Silicon photonics is supposed to be the shiny new growth engine. The shorts, however, suspect the tank may already be half full, and not in a good way. According to their customer checks, Soitec may have spent the past year quietly pushing discounted photonic SOI wafers into the channel, arguably faster than customers actually needed them. The goal, they say, was simple: keep factory utilization looking healthy while waiting for the smartphone market to wake back up. That strategy works, until customers start sitting on more wafers than they can realistically use. If major SiPho customers like Tower Semiconductor (TSEM) and GlobalFoundries stocked up ahead of their own production ramps, the result could be an inventory glut now working its way through the system. And when inventory digestion replaces fresh orders, growth stories tend to lose a bit of their shine. This dynamic may also help explain a subtle but telling disconnect: Soitec management is guiding only 20–30% photonics SOI per year growth going forwards, even as the broader silicon photonics market is expanding north of 35% per year. In theory, a supplier tied to a booming end market should be keeping pace, or even outrunning it. When it isn’t, the natural question becomes: is demand slowing, or are customers simply working through stock they already bought? 4/ Better Yields, Worse News: When Customers Get Smarter, Suppliers Sell Less A classic semiconductor irony: when customers get better at their jobs, suppliers sometimes get paid less. Today, leading photonic SOI customers like Tower and STMicro are believed to be running at roughly ~50% yields on their SiPho chips manufactured on SOI wafers. In plain English, that means you need to make about two chips to sell one, with the other half quietly heading for the scrap pile. It’s inefficient, messy and, somewhat perversely, good for wafer demand. But that math doesn’t stay ugly forever. As silicon photonics processes mature, yields typically march toward the industry comfort zone of 80–90%. That’s great news for chipmakers, investors, and margins on the customer side. The catch? Higher yields mean fewer wafers needed per finished chip. So while customers celebrate fewer defects and better margins, Soitec faces the less festive reality that every incremental yield improvement quietly trims wafer demand at the margin. It’s the kind of headwind that doesn’t show up overnight, but compounds steadily as processes mature. Because in manufacturing, efficiency is wonderful, unless your business model depends on inefficiency. 5/ The CPO bull case may be running ahead of the physics Bulls are underwriting a huge SOI payoff from CPO (why I bought initially), but shorts think that thesis gets stress-tested at the 400G/lane jump around 2027. 200G/lane scale-out works on SiPho/SOI. At 400G/lane, modulators may need new substrates if SOI can’t keep up. Lab demos from vendors such as TSEM and COHR exist, but scaling to high-volume manufacturing is still TBD. Tellingly, Lumentum’s new 400G/lane production platform uses indium phosphide, not SiPho on SOI. TFLN gets floated as the fix, but substrate supply makes that feel more like a 2030s story. Meanwhile, VCSEL and EML alternative scale up CPO architectures (Broadcom, Coherent) don’t depend on SOI at all. At minimum, the CPO outlook for Soitec looks murkier than bulls suggest. 6/ Soitec still trades like it’s special, while its peers trade like they’ve seen reality Even at ~€51, Soitec sits at ~1.3x P/B, a noticeable premium to peers like Siltronic and Wolfspeed (normalized for asset write down due to recent bankruptcy) trading 0.5–0.9x P/B despite similarly weak profitability. Given the impending risk of mobile softness, potential SiPho digestion, a CPO story that may be less near-term than marketed, and rising competition from Global Wafers, Soitec’s premium valuation starts to look shaky. If Soitec were valued like its unprofitable peers of 0.5-0.8x P/B, the implied $SOI share price range lands around €25–€35/share, or roughly 30–50% downside.

English

Some of the highest quality businesses in the world are trading at extremely cheap prices. Ignore the MSM. One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend.

One of the best times in a long time to buy quality.

Ignore the bears.

English

Sleep late to watch Suzuka or wake up early to watch the Candidates?

English

@blondesnmoney 20-30x PE. Consumer biz will be insignificant. AI biz volumes are tied to tokens, which is a secular grower. So long as you have the oligopoly playing nice on supply and propping up margins, it's HDD 2.0. $600-$900 stock.

English

If $MU earnings normalize at $30 a share in 2029 where will it trade

English

@evrgn11112231 @borrowed_ideas This is from the LLM, not sora. If these numbers are true, this is a strong confirmation on proof of concept and these dollars will ramp much further. other LLMs will take note and before you know it the competition for digital ad $$ will become extremely fierce for meta

English

thoughts on last week and how I'm thinking through my portfolio: mbi-deepdives.com/last-week/

English