Gabriel Neo

35 posts

Gabriel Neo

@GabrielNeo9

You can find all my research and articles here: https://t.co/7QtrfIw9H9

Beigetreten Nisan 2020

86 Folgt20 Follower

LG Innotek Eyes Intel “EMIB” Substrate Supply Chain… Supplies Samples to SK Hynix

LG Innotek is pushing to enter the semiconductor substrate market for EMIB (Embedded Multi-die Interconnect Bridge), Intel’s most advanced packaging technology. It has been learned that the company is currently collaborating with SK Hynix, including supplying EMIB substrate samples. However, the industry’s assessment is that because the development difficulty of this substrate is very high, whether it actually reaches commercialization remains to be seen.

According to the industry on the 2nd, LG Innotek is collaborating with SK Hynix to enter the substrate supply chain for Intel’s 2.5D packaging.

2.5D is an advanced packaging technology that inserts a thin film type interposer between the semiconductor and the substrate. Compared with conventional packaging that uses only a substrate, it can connect circuits at higher density, so demand is rising in the AI and HPC fields.

Intel devised its own technology called EMIB to improve cost efficiency in 2.5D packaging. Instead of a widely spread interposer, EMIB connects chip to chip using a small silicon bridge. Because bridges only need to be placed where chip to chip connection is required, chips can be laid out more flexibly and efficiently.

Currently, EMIB semiconductor substrates are known to be supplied by four companies: Japan’s Ibiden and Shinko Electric, Taiwan’s Unimicron, and Austria’s AT&S.

This substrate is based on the existing high performance semiconductor substrate, flip chip ball grid array (FC-BGA), but it is assessed as having greater technical difficulty because a silicon bridge must be embedded inside the substrate. FC-BGA is a package substrate that connects the semiconductor chip and the substrate using flip chip bumps (a method that flips the chip over).

It has been learned that LG Innotek is currently supplying EMIB FC-BGA samples to SK Hynix and jointly carrying out technology development. For SK Hynix, a memory company, the collaboration with LG Innotek offers the advantage of being able to understand the characteristics of high bandwidth memory (HBM) optimized for EMIB.

A substrate industry official explained, “LG Innotek is expanding its points of contact with memory and AI chip design companies in order to enter the substrate supply chain for Intel EMIB,” adding that “it is showing strong determination to enter the high value added semiconductor substrate market.”

However, whether LG Innotek will enter the EMIB substrate supply chain is still viewed as unclear. This is because the samples LG Innotek supplied to SK Hynix are only at an early stage, such as engineering samples (ES).

As a latecomer in the FC-BGA industry, LG Innotek is assessed as having lower technical capability than its competitors. In fact, LG Innotek has not yet entered the server FC-BGA field, which requires high specification and large area technology. The need for enormous investment, such as building a dedicated line, in order to mass produce EMIB substrates is also a major challenge.

A semiconductor back end industry official explained, “Intel EMIB substrates are already in a situation where overseas companies have solidified the supply chain, and Japan’s Ibiden also recently announced the construction of a dedicated line worth more than 2 trillion won,” adding that “for LG Innotek to enter the market, it must clear both technical and market hurdles.”

English

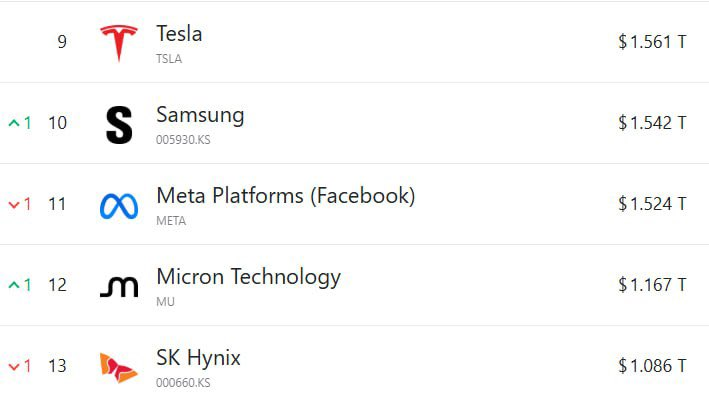

@DeepValueBagger I think you missed the part where Samsung overtook Meta...

Just today

English

@jukan05 I mean he has to say what he has to say to pump $NVDA

English

@aleabitoreddit Nah don't doubt yourself...

Shunsin will limit up tomorrow as well 😏

English

I had higher expectations for Shunsin tbh.

It’s been close to a month and a half and it’s only up 39.96%.

Maybe I’m not as good with Taiwanese optical stocks.

Serenity@aleabitoreddit

Taiwan $NVDA CPO supply chain ide #1: Shunsin (6451 TWSE) - Photonics Packaging at ~$1.4B MC. It's a subsidiary of Foxconn. And Foxconn is ODM for $NVDA. It's almost like Celestial got listed by $MRVL and got a free piggy back ride? Some personal est. 2027 fwd ~20 P/E, that compresses harder into 2028, 2029. Shunsin's optical division openly lists their markets as "CPO 51.2T/102.4T" and "Pluggable XCVR 800G/1.6T. Markets themselves as "Supported by Foxconn's vertically integrated supply chain for fast project ramp" If you look at $TSM COUPE for $NVDA, they don't assemble final fiber arrays/racks, Foxconn does. So $NVDA's CPO networking gear probably goes through Shunsin's alignment and bonding machines? And $GOOGL, $META optical switches probably end up thorough them too since they scaled Vietnam CPO facilities (speculative). Basically you get a free Foxconn piggy-back ride with this company at low forward multiples. Disclosures: I am personally long.

English

@Blinklebloop @zephyr_z9 Limit up today, didn't manage to get in

English

I really do think Sakai Chemical 4078.T is a big winner here. @zephyr_z9 has mentioned the name multiple times.

It's not expensive. Especially when you factor in the growth in the MLCC market.

EV/EBITDA 7.6x

P/E adj. 18x

P/B 0.97

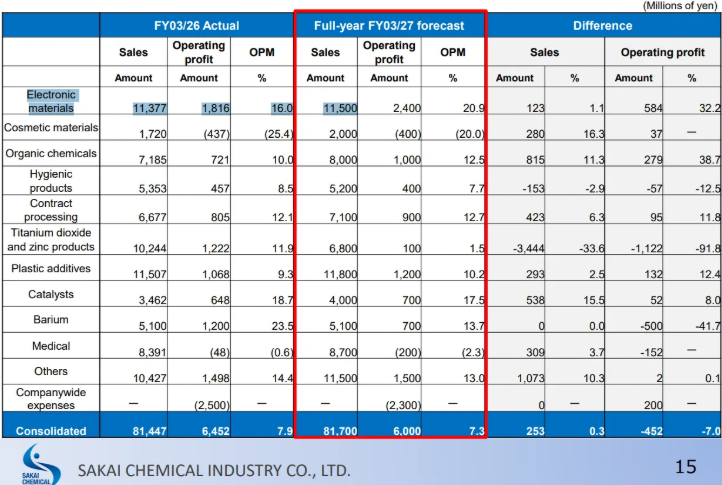

Operating profit holds 40% exposure to MLCC through Sakai's "Electronic Materials" Segment. Or 29% of operating profit before unallocated companywide costs.

「当社電子材料のほとんどがMLCC用途」

“Almost all of our electronic materials are for MLCC applications.”

— Sakai Chemical Integrated Report 2024.

Electronic Materials is probably 99% exposed to MLCC currently. Highest margin segment.

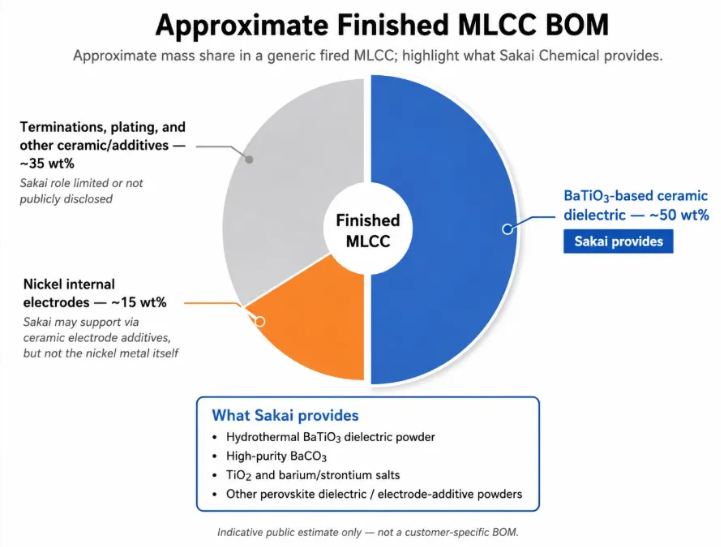

The core material is BaTiO₃ which is the highest BOM that goes into an MLCC. Around 50% of the cost.

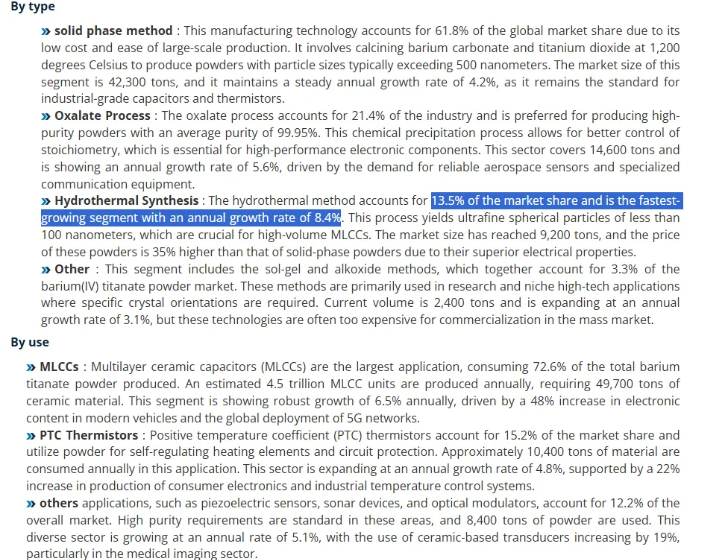

The market for BaTiO₃ consists of

-Hydrothermal. 13.5% market share.

-Oxalate. 21.4% market share.

-Solid-state. 61.8%

Hydrothermal and Oxalate are used in the high-end MLCC because the processes produce very fine, highly uniform particles.

Sakai is using Hydrothermal.

That's most likely 40% operating exposure to what @zephyr_z9 describes as an AI Server market growing at 80% annually.

Zephyr@zephyr_z9

What's happening in the MLCC market First off, MLCC as a whole is a $15B market. MLCCs for servers were a $1.3B market in 2025 ($600m for AI servers, $700m for general servers) The AI server MLCC market is growing at 80%+ CAGR, and the general server MLCC market will also accelerate due to agentic AI increasing CPU demand (around 30%-40% CAGR) We will see negative growth in the smartphone/mobile MLCC market for at least 2026-27. Humanoids are another future high-growth market for MLCCs Book-to-bill ratio for most MLCC suppliers is over 1 now Reasons for price hikes- High Nickel & Silver are affecting all segments There is a supply-demand mismatch in the high-end (high capacitance, high voltage) segment, which is used in autos & servers High-end MLCC lead time is over 20 weeks Spot/distributor prices have increased by 20%-40% for low capacitance & consumer device MLCCs due to hoarding and double booking, especially in China OEM contracts have not seen large price hikes yet What's happening now: Rapid capacity expansion happening across the industry Murata expects blended ASP prices to remain flat (ASP going down in consumer electronics, expansion in AI server market) Tier 1 players like Murata, Taiyo Yuden, SEMCO building capacity to serve AI server MLCC market This will create opportunities for Tier 2/3 and Chinese suppliers to expand in the mid to low end market (Macronix effect) Future: MLCC production equiment & raw materials suppliers will be the biggest beneficiary of this CAPEX boom MLCC producer stocks have performed well, and it is finally spilling to raw material/equipment producers I expect them to outperform MLCC producers now

English

@aleabitoreddit Sakai Chemical should be the better MLCC materials pure play here. Sakai uses the hydrothermal synthesis method to produce high-capacitance MLCCs for AI servers. While NCI's oxalate method produces coarser particles for mid-range MLCCs

English

@JonahLupton @SupremeFireCPG More interested in if $KEEL will ever get a customer. Companies only go for the best neoclouds, I don't have enough technical specs to know if $KEEL makes the cut. No customers means no proven product -> still a speculative buy for me

English

@SupremeFireCPG I haven’t spent much time looking at $KEEL since I already own several others in this space including $NBIS $IREN $CIFR $CRWV $BRUN $SHAZ

How much contracted power does $KEEL have??

English

$KEEL is primed for takeoff!

After parading to near its 52-week high of $6.60 on massive volume and closing at ~$5.68 today with strong momentum, the CEO just dropped that the team has already met with 129 investors since the May 11 Q1 call — nearly matching all of 2025 combined — and is now slamming the brakes to “get back to work.”

With permitting secured, 3 power leases targeted this year, and investor frenzy off the charts, a major contract or deal announcement looks imminent.

This could be the spark that sends $KEEL parabolic. Positioning now in @keelinfra_ will prove as prescient as our early moves into $CIFR $IREN $WULF $APLD $HUT , all trading under $5 not that long ago — the 3x execution phase is here! 🚀

English

@aleabitoreddit I swear, space stocks are like the SPACs of 2026. All trade on 100x revenue now...

English

@amitisinvesting Just because a bear case has already been "discovered", doesn't mean it cannot cause a lot more damage. Using your own example: many in 2007 did see the housing correction, some paid attention to subprime stress, but very few actually saw the collapse of the financial system.

English

You know what I’ve started to really think about…

In 2008, those that called the housing crisis had something that the entire stock market did not have: data around the housing crisis.

Now, the data was available to the entire market, but only a few people chose to deeply study it and interpret what could happen.

In today’s AI driven stock market, the only way for there to be a 2008 like crash is if there is something underneath the surface that the market is completely ignoring.

That would have to be the smoking gun that someone finds out about and can then use to determine what would crash the entire rally.

But…isn’t everyone already looking for that?! Like, aren’t people obsessed with trying to find out how the bubble pops?

We have people daily dedicating every bit of their research to find out how this breaks. Every argument, whether it’s circular funding or capex slows down or higher inflation etc is theorized about daily.

It’s almost like we have so many people afraid of the dot com bubble happening again that there is an OVER emphasis on all the things that can go wrong (which is healthy) and as a result, every massive bear case is already out there…already discovered…already priced in.

Which means that if every market participant is analyzing every single thing that could go wrong, there is going to need to be a REALLY good and original bear argument for things to go bad.

Everytime you hear a bear case, it should be more original and something you haven’t thought of because if not, it might have already been discovered and not actually be a bear case.

English

@amitisinvesting "Data available to entire market"-> not really. The problem wasnt housing prices or even subprime stress, but the financial architecture built onto them, which was opaque to outside investors. Like how deeply CDOs had been sliced, re-sliced, and packaged again into CDO-squareds.

English

@aleabitoreddit $ARM and other PC OEMs like Dell, Asus should also benefit here.

English

Hot take: Given $MSFT laptops/PCs are now likely using $NVDA hardware.

They might have a shot of taking down $AAPL.

Only if Windows OS UI weren’t a flaming pile of garbage compared to how clean Apple OS is.

You would think a $3T company would know better UI design by now?

English

@dividendology "Berkshire compounded and outperformed for the next few decades." -> lol no.

Still living in the 2010s?

No discredit to Buffett here, it's really hard when you're managing hundreds of billions.

English

20 months leading up to the Dotcom peak:

Nasdaq: +290%

Berkshire Hathaway: −45%

Every newspaper headline was about Buffett had lost his touch.

Then everything fell apart.

The Nasdaq lost 78%.

Berkshire compounded and outperformed for the next few decades.

English

@MMMTwealth Best not to take the 471M/month at face value, management has a terrible track record.

But yes it would still be cheap even if revenue ramps up to just half of what is projected.

Now it's just about how far-fetched the 471M/month value actually is.

English

$AAOI is very quickly becoming attractive again here at $12.7B market cap with 2027/2028 set to be huge ramp up years.

-> Mid-2027: $471 per month in revenue.

-> Fair to assume 2028 could be ~$6B (when added in CATV revenue as well).

That means they've gone from $455M in revenue in FY25 -> potentially $6B in FY28... that's a 136% CAGR.

Absurd ramp up in revenue.

I ran a scan of those companies expected to hit more than 120% CAGR for the next 3 years and I think it's probably only these:

$NBIS

$ASTS

$IREN

$AUR

$ONDS

$USAR

$NN

Now $AAOI trades below 10x NTM sales right now.

Guess which of the above trade below 10x sales?

None.

Oliver | MMMT Wealth (CPA)@MMMTwealth

$AAOI - THE BULL CASE (numbers) Let me show you the numbers: On the earnings call, management said if the hyperscaler demand plays out like expected, $AAOI could reach a data center revenue production rate equivalent to $378M per month by Q2 2027 which would equate to ~$4.5B in annualized run rate. They also guided for 40% gross margins by Q3. P/S: $LITE trades at 14x FY26 revenue with 76% expected growth with mid 20% operating margins. $AAOI trades at 7.0x FY26 revenue with 112% expected growth with anticipated 40% operating margins. So if $AAOI's AI/hyperscaler segment even gets to ~75% the multiple of LITE (which it should based on numbers), then $AAOI is deserving of 9x sales multiple on FY27 revenue, you're already looking at $40.5B in equity value right there. This is excluding the lower multiple segment of $AAOI which is CATV/Broadband which management expects ~$300M / year business. Give that a 2.0x sales multiple and you can add another $0.6B or so to the valuation. I don't think 9x sales multiple on the data center revs is unlikely at all so based on those numbers (if you believe management), then $AAOI is a great buy here. Even if you assume $AAOI achieves only 50% of the $4.5B annualized AI revenue run rate, and the multiples therefore compress to say 6x/7x you're still looking at potentially 2x from here. That's not the full story but that's a clear picture of the bull case looking purely at the numbers.

English

@aleabitoreddit Very strong tailwinds for sure. Names like LG Innotek have already 5x this year.

English

@slabecry @aleabitoreddit Err..the big run part is subjective, no comment. Murata debuted their CPO components at ofc this year, but gonna assume "industry leader" you are saying is about MLCCs. On that, I don't really think it's cheap compared to peers except SEMCO, which now trades at absurd valuations.

English

Per Foxconn shareholder meeting:

CPO switch products expected to begin Q3. 10K units 2026, explosive grow to next year.

Aims/expected to be #1 globally.

Anyone remember which Foxconn subsidiary handles their advanced optical work?

cough.. cough.. Shunsin (6451).

Lot of these exponentially scaling volume shipments won’t show up in balance sheet yet, but will likely soon H2.

This is called frontrunning the next supercycle.

English

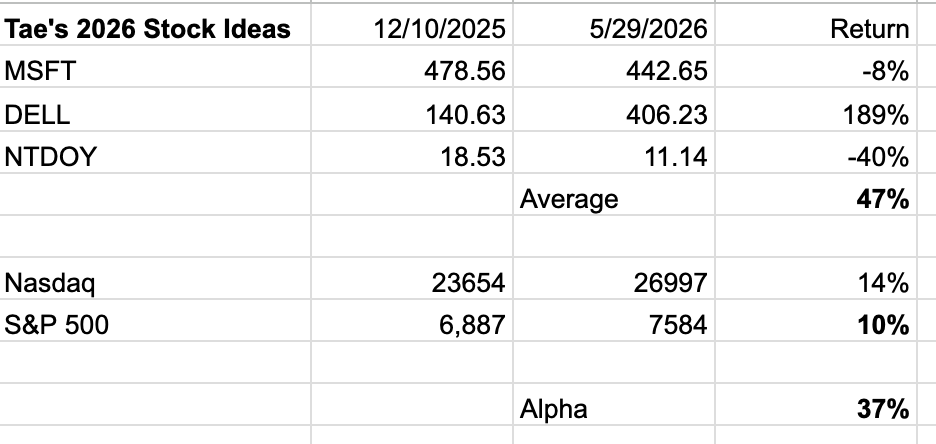

@firstadopter You're boasting about a good 2026...with 2/3 stocks in the negative?

Also Alpha is excess return compared to the benchmark AFTER ADJUSTING FOR RISK, not just return - benchmark return. Can't say you have alpha until you show us your Sharpes and Sortinos.

English

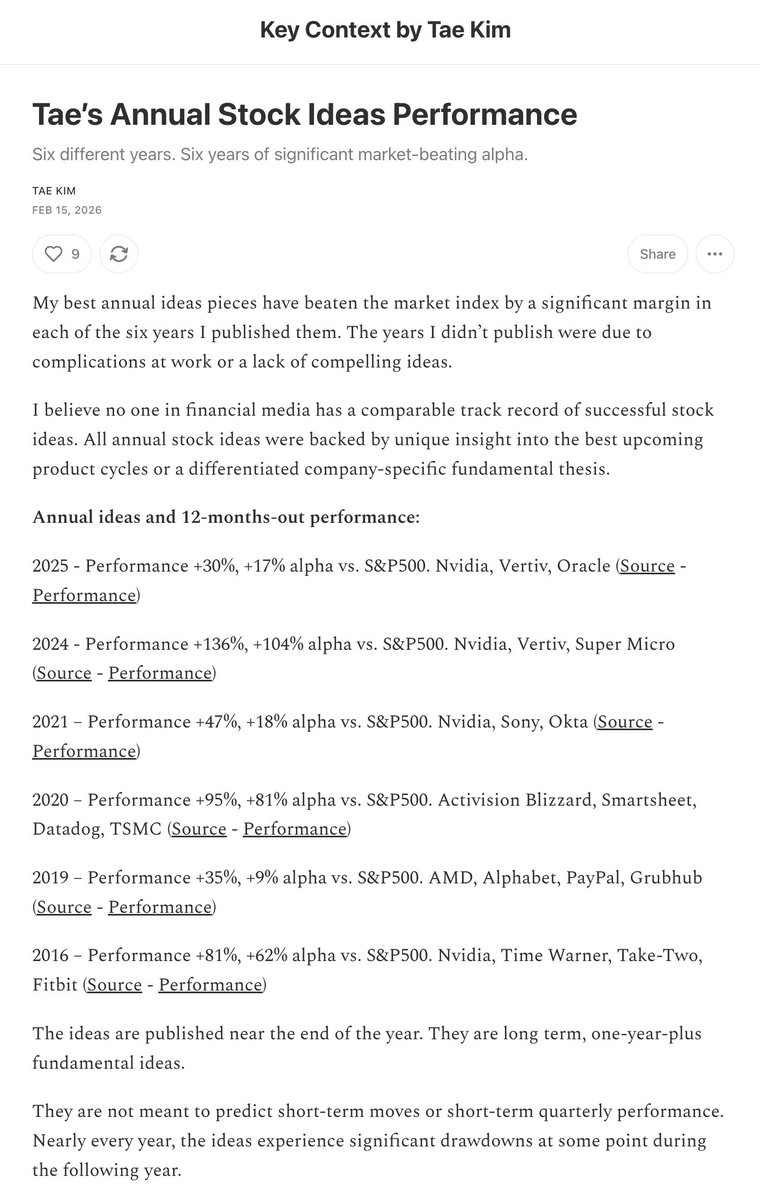

Thanks to $DELL I am now on track to crushing the market with my annual stock ideas for seven years running with big upside every single year.

Look at my prior years' annual stock ideas. 2026 is not an anomaly.

Plus, my Substack ideas during the last few months, including DELL, are even doing way better.

tae kim@firstadopter

My top 3 stock ideas for 2026: Microsoft, Dell and Nintendo. I’m also extremely bullish on OpenAI and AI enterprise adoption.

English

Co-Tech Development is a qualified mass producer of HVLP4 copper foil for AI server PCBs.

Goldman Sachs initiated coverage a few weeks ago with a NT$900 price target, a 50% upside from here.

First time sharing here so appreciate any support❤️

open.substack.com/pub/gabbyssand…

English

@insane_analyst Hynix leads in HBM, still the primary supplier for Nvidia H100, H200, B200

English

You have $100K and must invest it in one of these options. You have access to Korean equities thru IBKR. Bonus points for intelligent comment justifying your vote.

English