Sabitlenmiş Tweet

I have added my own bit on the valuation side of $SOI

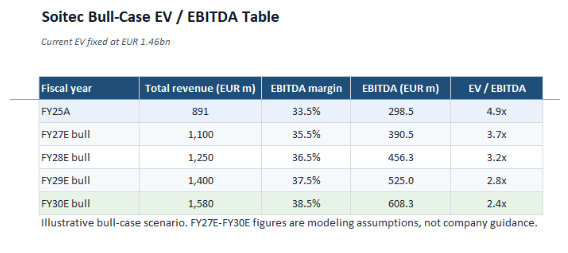

I think its an extremely compelling investment. EV/EBITD currently at 6.5X !!!

Exposure to the photonics theme at a fraction of the price, in a company with a near monopoly to the tech.

This will be a story for next year and beyond.

Davy@Blinklebloop

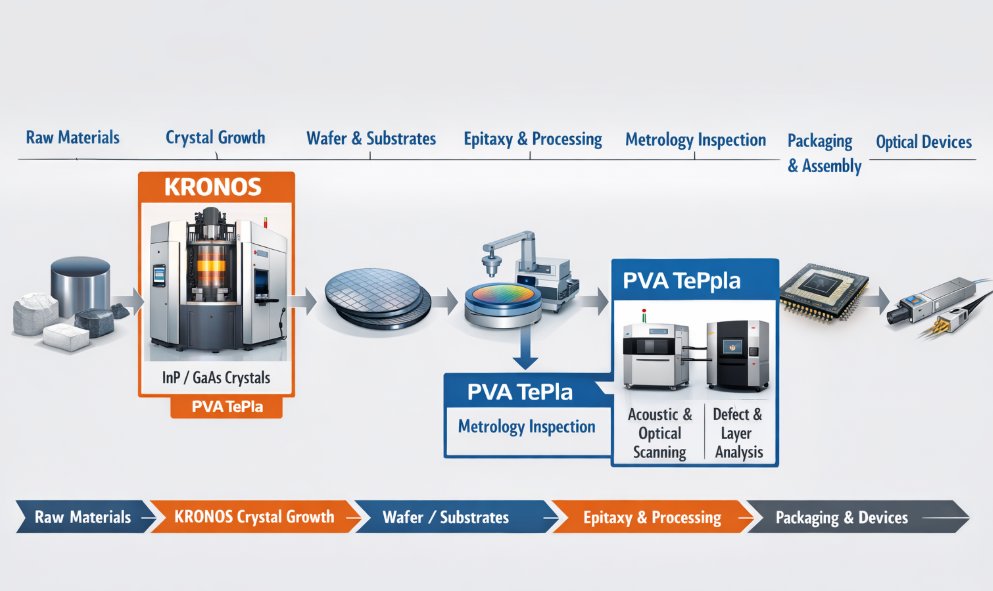

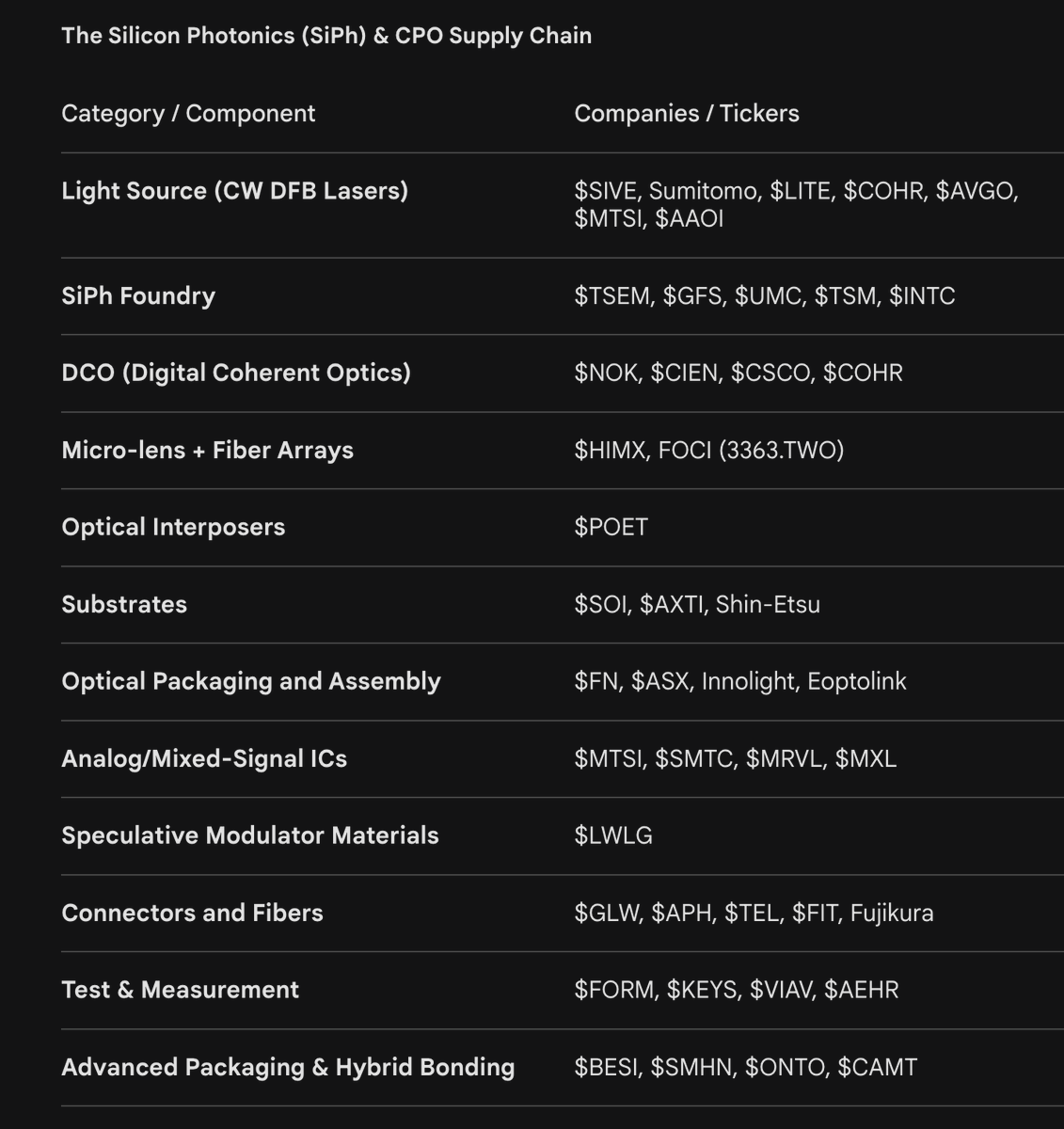

This is a brilliant find by Jason. SOITEC, trading at EV/EBITDA of 6.5~ Near monopoly on the Smart-Cut technology used to make SOI wafers- which are used to make PICs, which are used to make transceivers (think $AAOI, $LITE, $COHR). It’s not often you get exposure like this in a bombed out industry. I have added my piece on the valuation, which I think is highly compelling. Nice work Jason! Glad I started reading your work! jasonschips.substack.com/p/the-soitec-s…

English