Angehefteter Tweet

Ap3

925 posts

Ap3

@InfiniteSqueeze

HODL $GME $BBBY - Fight against greed and corruption - MGGA MAGA

Beigetreten Kasım 2024

486 Folgt169 Follower

Ap3 retweetet

Ap3 retweetet

English

Ap3 retweetet

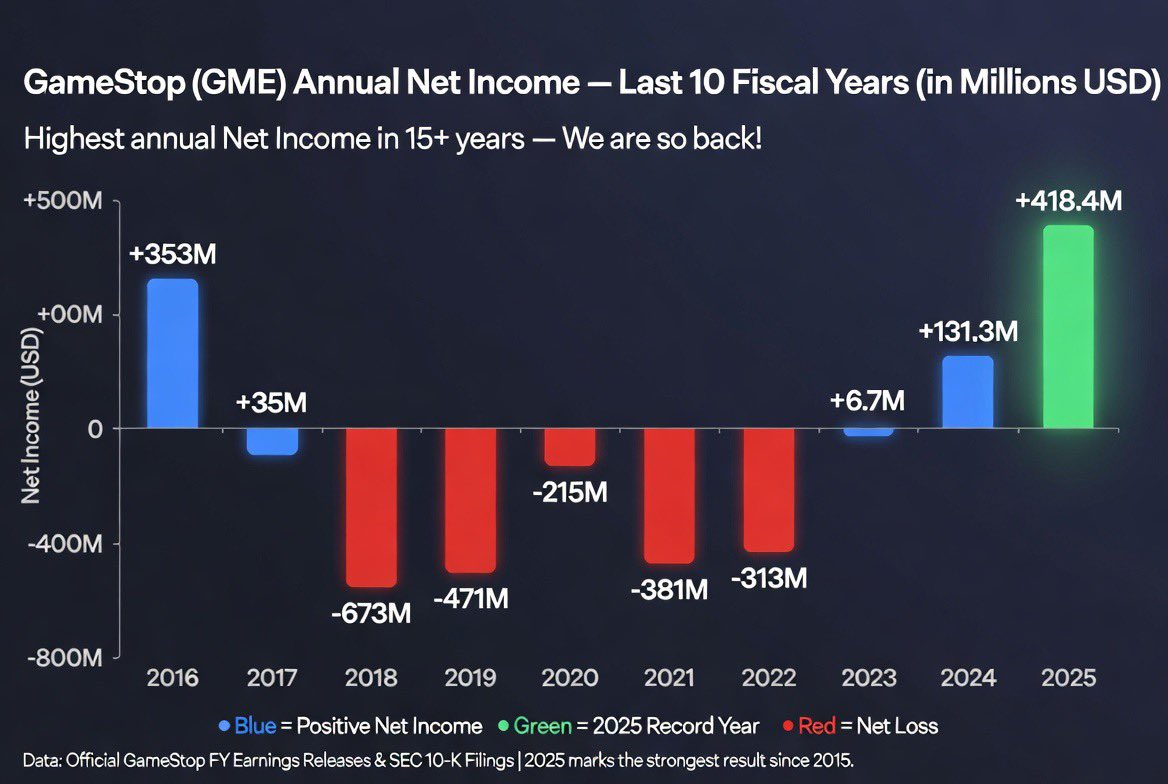

$GME NET INCOME TURNAROUND IS OFFICIALLY INSANE 🌊

2019: –$470.9M

2020: –$215M

2021: –$381M

2022: –$313M

2023: +$6.7M

2024: +$131M

2025: +$418.4 MILLION !!

From bleeding nearly half a billion to printing record profits in just 3 years.

The transformation is WORKING. 💎🚀

English

Ap3 retweetet

GameStop FY 2025 Results:

Net sales: $3.6 billion

Net income: $418 million

Full results: investor.gamestop.com/news-releases/…

$GME

English

If Ryan has $GME buy any version of BBBY, I am out.

English

Ap3 retweetet

The biggest due-diligence of my life is now live at bbbwhy.com.

It covers the $BBBYQ bankruptcy strategy, my theory on who $GME's target acquisition is, how @ryancohen exactly is going to build the next Berkshire, as well as WHEN I think this is all going to happen and MUCH MORE.

Peace out, I'm going to go rest my brain. Enjoy. Share.

The best is yet to come. 💛

English

Ap3 retweetet

Ap3 retweetet

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

English

Ap3 retweetet

Why is $JPM displaying GameStop Corp's logo as a black pirate flag? 🏴☠️ $GME

English

Ap3 retweetet

@BRKmystery @amitisinvesting @arny_trezzi Buffett gained control of Berkshire Hathaway by hiding his purchases through many different brokers. When he had enough he showed up in person and took control. That is not available to us wannabes these days.

English

@RJCcapital $GME has transformed from a practically dead company into a $500M+ annual FCF and $9B cash on hand company

Yet the market cap is currently $10.5B at $23.5 per share

That’s some Deep Fucking Value

GIF

English

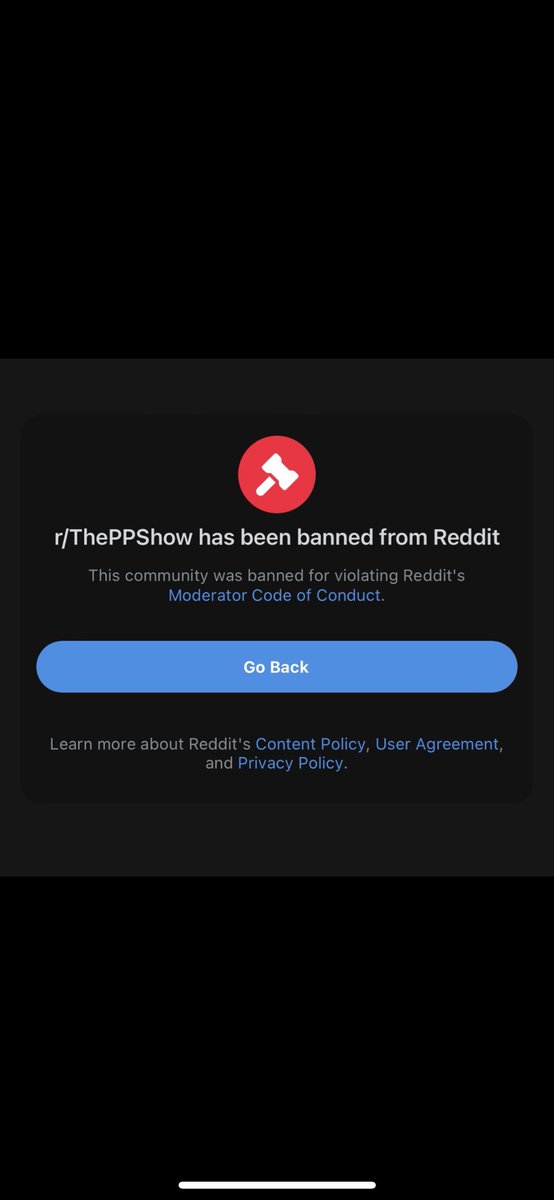

@LJenkins69420 November 21, 2023

The day r/ThePPShow was banned and confirmed our suspicions that Reddit was compromised.

All because we were interested in $BBBY stock

And then the great migration to X

Never forget how far we’ve come!

English

Pulte’s phone dies on ThePPShow

New Teddy books drop less than a minute later

Just think about how insane that is...

English

Ap3 retweetet

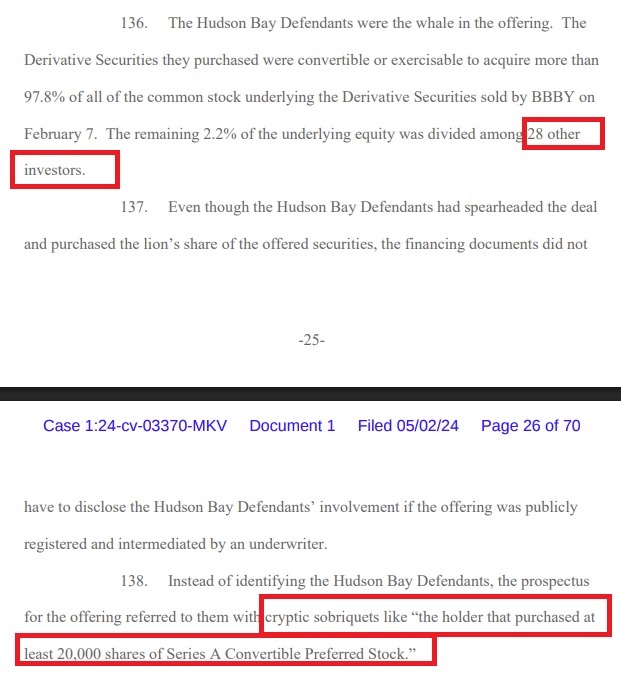

no sir I need to correct here: the 739m tso was not revealed until the 10-K which was filed one month *after* the share ledger was filed with the court and the 10-K tso was dated to the day after the ledger filing (May 9) even though it only reported financials until February 25.

then in September, *after plan confirmation* there was an 8-K filed that the tso was going to be changed to 782m even though there had been no issuances and it was back-dated to July. that’s how I realized that a settlement happened after confirmation.

also worth noting there were never enough preferred issued from the equity raise to ever get to 782m as revealed in the ledger.

as an aside I believe that is one of the main reasons why so much about the tso was redacted in the lawsuit by the plan man against HBC. the tso was not what it should have been between February and July of 2023.

they got caught.

English

Ap3 retweetet

@OgSpaceJam22 @mikeal_man @ChrysanthTea @ThePPseedsShow @Q2024694202 “GameStop investors had fingered the hedge funds that allegedly tried to sink its stock”

lol apes fukt hedgies bigly

English

Ap3 retweetet

Too late, can’t buy any more legacy $BBBY shares!! That ship has long set sail

For those who want to FOMO in, there’s speculation legacy BBBY bonds may turn into shares. IBKR turned off the buy button for legacy bonds but E*Trade may still allow you to buy legacy $BBBY bonds? Can anyone confirm? That might be your only way to jump on board 🚀

English

Ap3 retweetet

what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.

jake2b@jake2b

I would like to renew the conversation about $GME and the "new class" shares that appeared the day before earnings on 9 September. I feel as though it was a hot topic for a moment and then was completely forgotten. a lot of folks had been asking why there would be a change, but did anyone ask how? Let's look into it a little more. I can only quote one post, but here's another that everyone should see: x.com/TheBronxViking… The Bronx Viking had called their broker and the response they received was stunning, in my opinion. "They acknowledged the name change to “GME class New” but did not see any reason for the change on their end(filings, news, disclosure, etc.) The name change gets fed to them and other brokerage from a vendor that supplies them with the quotes" emphasis mine. naturally, my first question would be HOW is it possible that a vendor supplying quotes has a change in classification of the #GME shares? I am going to go on a limb here and assume that the vendor did not suddenly choose to reclassify the shares on their own. so, what could have happened? I began looking into some of the "plumbing"—ugh, Gary—of how market data comes to brokerages. Schwab gave Bronx Viking a crumb by stating that they receive their quotes from a vendor. this explains why some brokerages around the world had the change and why others did not. perhaps, they are licensing with different vendors or maybe, some brokerage systems populate from feeds differently because they have their own computer systems—who knows, doesn't matter. the point being, if the vendor was supplying the "new class" of shares information, where did it come from so that their systems would have made the change? where did they get it from? this is why I started the post by saying, why is no one asking about the "how"..— because it certainly appears that the market data feeds and aggregators can only receive this change from only three sources: • the NYSE (exchange); • FINRA; or • the issuer now we're getting somewhere. let's look back at GameStop and their S-3 filed in May: I had mentioned it before and again, this is very strange. let me make the distinction: it is complete normal for their to be a legal opinion on a S-3 filing. it is completely not normal for the legal opinion to state "as to the legality of securities being registered." go check, this distinction is not present on other legal opinions for S-3 filings. I mean it makes sense, think about it—how could the securities not be legal? this is not an IPO, shares of GameStop already trade.. of course they are legal. so the only reasonable presumption for the addition of the legal language could be.. you guessed it. what if GameStop is preparing for a new class of equity securities? ones that are tokenized, backed by the blockchain, or otherwise considered a "digital asset"—this quoted from the agreement between GME and Jefferies, after all. of course they are going to do it, why else would it be in the share offering agreement between them? I believe that this explains the additional legal language found in the S-3 legal opinion header. so, what does that tell us? well, there are a lot of regulatory checks you have to satisfy to offer a new class of shares, a dividend, etc if you are a publicly-traded Company like GameStop. so of the three sources that the vendor could have received the "new class" moniker that was passed down to brokerages, I believe that we can eliminate the issuer as the source and the simplest reason is that they need regulatory approval first. — suddenly, a lot of things fall into place. Since GameStop told us that they plan on doing this, we know that they would have to file these "new class" with the regulators and NYSE. in order for the regulator and/or exchange to have pushed this new nomenclature to the vendor, which later supplied Schwab, it would suggest that the regulator approved it. we don't know this but really, it is just common sense. I want to circle back and remind everyone that we are speaking about blockchain-based, tokenized securities. this is what GameStop and Jefferies has outlined in their agreement which was made at the time the offerings began. we do not know if it is a conversion of old GME shares, a new kind of share, a dividend—but, we can reasonably speculate. because after all, it was the legacy GME shares in Schwab and other brokerages that had the change from "Class A" to "New Class". — speaking of exchanges, I would like to make sure everyone knows that GameStop trades on the NYSE. this is very important because the NYSE is owned by a parent company, called ICE (intercontinental exchange). well, guess what? the NYSE is ready for blockchain-based, tokenized shares. they've been ready since 2022, having made an investment in the outlier blockchain market tech that has the most regulatory approval by far and combined with the NYSE, well.. ..what if they just integrate tZero into the already existing NYSE system? this would be incredible, because the blockchain technology could leverage all of the existing exchange "plumbing"—settlement, delivery, transfer, etc. on the customer side, anyone would log into their existing brokerage account and own blockchain and non-blockchain securities side-by-side. no private keys, no learning about wallets and seed phrases. it would just.. work. the security would participate on the blockchain and the end-user would not have to. now, how is that for seamless integration? — "worry less, trust @ryancohen more." n.b. thank you @TheBronxViking and @DominosJack for your posts!

English