Angehefteter Tweet

People of all ages, colour, creed & religion united to speak for justice & freedom

#freepalestine

English

MP 🇵🇰 🇵🇸

4.2K posts

@MP4FMPK

delusions of grandeur suit me just fine. #economy, #investing, #cricket & baba to a 7 year old angel

Suppose I have PKR 1 billion and want to earn profit only from debt instruments (from a tax perspective) over a period of three months(before 30th June 26), while retaining some flexibility to utilize a portion of the funds for working capital needs of a business. What options are available to maximize profitability in the current scenario, especially when fixed-income yields are rising? -Negotiate with a bank to obtain the highest possible return on a savings account. -Invest in short-term (three-month) T-bills. Note: If liquidated early to meet fund requirements, the resulting gain may be subject to capital gains tax, which I would prefer to avoid. -Enter into a term deposit arrangement with a bank after negotiating competitive rates. Any other viable options? Please share your input for learning and discussion. Plz ignore other options of investment and tax benefits in other cases as we have only option of debt instruments to get only profit on debt from tax planning point of view.

If you are a salaried person in Pakistan, your taxes are deducted at many different points during the year, and each deduction is properly recorded in the FBR system. For example: Monthly salary: Your employer deducts withholding tax every month and deposits it directly with the government under section 149. Vehicle token Taxes: These taxes are paid through proper challans and are fully traceable and relevant collecting authority deposits the same into Govt treasury under section 231B/234. Utility bills: Electricity, mobile, telephone, and internet bills include withholding taxes that are automatically deducted and reported/deposited to FBR under different sections of income tax ordinance. Foreign transactions: Advance tax under section 236Y is also deducted at source. And there are no of other withholding tax transactions. Since all these taxes are collected in advance, submitted electronically, and in most cases appear in the filer’s IRIS account with proper CPR numbers, the government already knows exactly how much tax a salaried person has paid. Their own system verifies everything. Because of this, there should be no reason to delay refunds or force taxpayers through long application submission procedures—especially when salary is the only source of income. The system already holds all the data; it simply needs to match the tax paid with the actual tax due and automatically issue the refund to the bank account provided in the taxpayer’s FBR profile—just like many other countries do. But in Pakistan, instead of automatic refunds, taxpayers still have to file separate refund applications, wait for months or even years, and deal with unnecessary hurdles. With such a complete and data-rich system already in place, what we truly need now is transparency, automation, and an efficient refund mechanism, so taxpayers receive what is rightfully theirs without delays. @FBRSpokesperson @CMShehbaz Let’s start this year by implementing automatic refunds for salaried individuals whose only source of income is salary, and then gradually expand it to everyone.

If salaried, speak to HR and provide details of: VPS investment Advance tax on internet/credit card etc Charitable donations (recognised) HR can then adjust tax on salary (but are not required to) and you can avoid refund delays. Section 149(1) + rule 42 of the ITO

OUR FISCAL NIGHTMARE FROM MICHAEL BURRY’S LENS Michael Burry warned: The moment your interest payments exceed tax revenue, your country becomes a Ponzi scheme. Welcome to FY26: - Federal interest payments: Rs 8.3–8.8 trillion - Total federal net revenue (after NFC): Rs 7.5–8.0 trillion Let that sink in: We can’t even pay interest without borrowing more. The federal government is now: - Borrowing to pay interest - Borrowing to run the state - Borrowing to survive It is not sustainable.

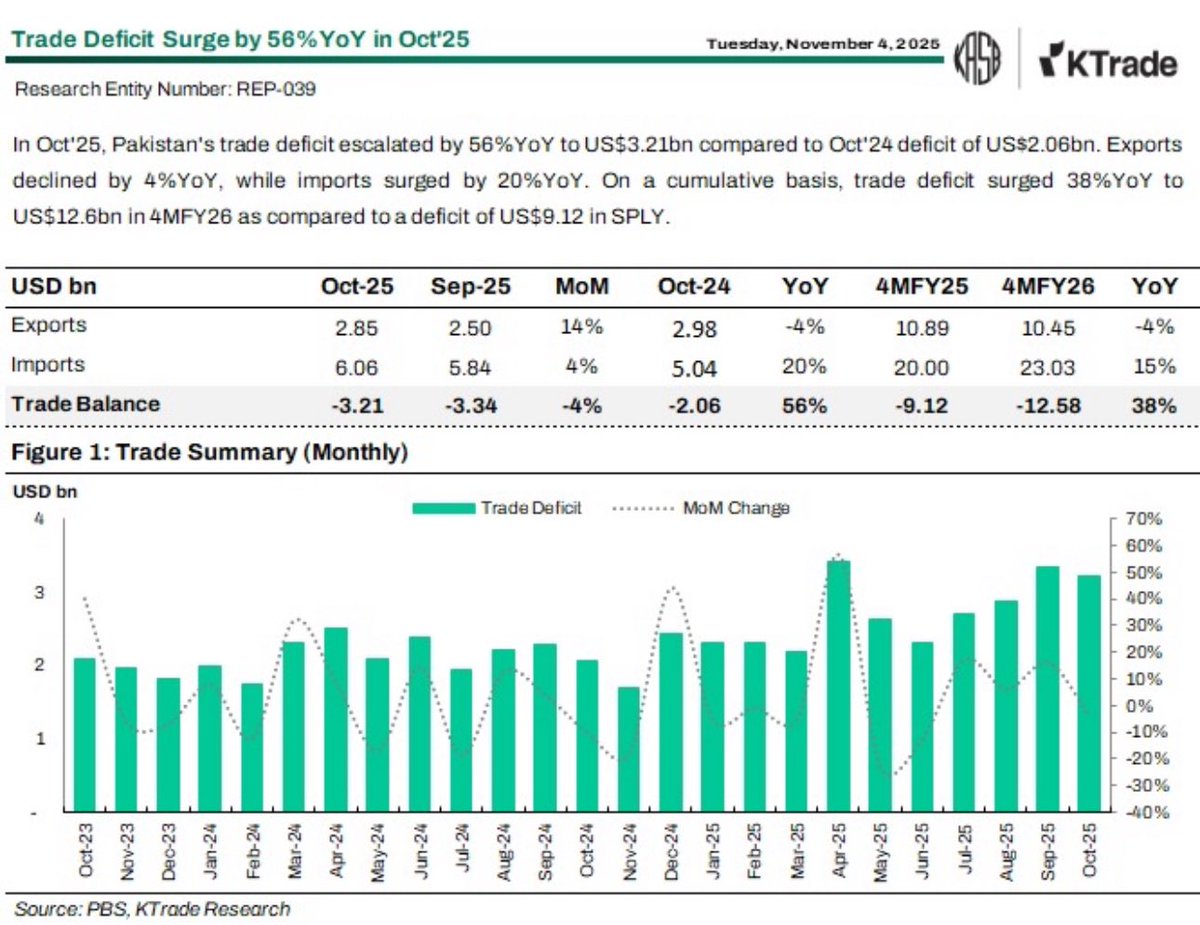

A trade deficit in itself means nothing. As long as imports are contributing to future productivity & you can fund the gap with mostly non debt dollars. If there are no inflows to offset higher import payments then reserves should feel the impact during Nov. 2/3