@MagnusSigurdss $UPST is now a cheap stock on fundamental value of its earnings. So the stock will start to attract value investors. Momentum/tech investors will come back only after it is up 100% from here.

English

Pat MacNeill

4.4K posts

mesh-llm: pool compute to run open models. built by @michaelneale at block: docs.anarchai.org

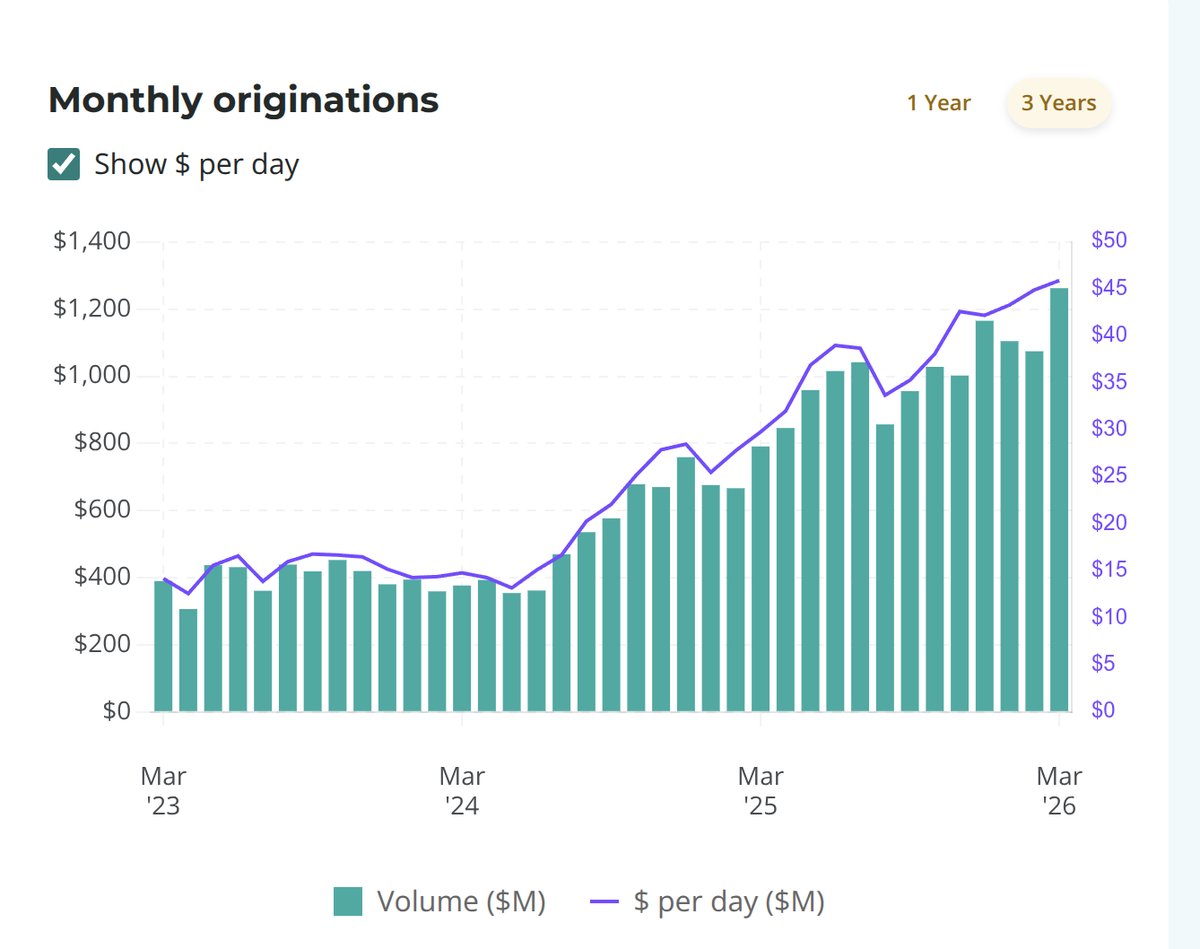

⚡️Preliminary UpstartIQ March Originations and 1Q26 Revenue Estimates #UTPI / $UPST Upstart will be posting March origination data this Friday (the 3rd of the month). I believe March originations will come in ~ $1,154M, up 7.3% MoM, up 45.6% YoY. Here's how I arrive at that estimate (view graphics): 1) Originations ($M) per day is simply monthly origination volume / number of days in the month (this is different from the normalized metric Upstart provides) 2) I estimate that Originations ($M) per day will grow directly in line with the growth of Trustpilot Reviews per day. 3) I then apply this growth rate in MoM reviews per day (-3.1% from Feb to Mar) to Originations ($M) per day and multiply it by the 31 days of March. That puts me at $1,154M in expected origination volume for March. Obviously, the 1:1 ratio/relationship between Trustpilot reviews per day growth and Origination ($M) per day growth is overly simplistic, so please take that with a grain of salt. It did prove rather accurate in February, however ($1,069M est. vs $1,075M actual). Now that I have all of the monthly origination volume for 1Q26 (the reported January and February numbers, plus my March estimate), I can attempt to calculate Upstart's take rate per month by dividing monthly fee revenue by monthly originations. Because Upstart does not provide fee revenue by month (instead only providing it for the quarter), each month's revenue from fees is a pro rata share of the respective quarter's fee revenue. This is not a perfect methodology. monthly fee revenue / monthly origination volume = take rate %. You can see that take rate has been trending down (11.9% in July 2024 -) 7.6% December 2025), reflecting management's commentary towards the intentional dynamic of reducing take rates to achieve larger market share, pass savings along to the borrower, plus the dynamic of lower margins for new products Auto & HELOC. For 1Q26 (January - March) I had previously assumed that Take Rate would trend down slightly from the already subdued level of December 2025. I think that was too overly conservative. While December's take rate was 7.6%, the blended average for 4Q25 was still 8.3%, as compared to 9.1% in 3Q25, 8.6% in 2Q25, and 8.7% in 1Q25. For 1Q26, I am choosing to apply a blended 8.07% take rate across all three months in the quarter. This represents a ~63 bps decline from the 8.7% blended average of 1Q25, or a decline of 7.2% YoY. When you apply my take rate assumptions (8.1% Jan, 8.1% Feb, 8.0% Mar), you arrive at monthly fee revenue taken as take rate * monthly originations ($). When adding those estimates together, I am arriving at a revenue from fees estimate for Upstart in 1Q26 at ~ $269M as compared to $265M in 4Q25. Remember, the first quarter of the year is always seasonal and almost always has lower revenue than that of the fourth quarter. As for net interest income, Upstart has guided for $100M for 2026. My assumption (a pure guess) is that NII will look something like $31M -) $27M -) $23M -) $19M (totals $100M) as they make progress reducing their balance sheet over the year. When you add together the $269M and $31M NII estimates, that yields $299.9M in 1Q26 total revenue. Net interest income is doing a bit of heavy lifting here, but the quarter is also seasonal. This would put total revenue up 1.3% QoQ (1Q25 saw -2.6% QoQ, 1Q24 -8.9% QoQ) and would represent 40.6% YoY growth. The average analyst estimate for 1Q26 today sits at $298.5M, so Upstart is right in line with what's expected in this scenario. For those who prefer the more 'old school' UpstartIQ method, I am also arriving at a rough estimate of $300M for 1Q26 revenue. In this scenario, I am assuming that once again net interest income comes in around $31M (versus $31M in 4Q25), Servicing Platform Revenue of $44.2M (up 3% QoQ - the same growth rate seen in 4Q25) which brings total non-core revenue to $75.2M. With 3,229 1Q26 Trustpilot Reviews and a Review Rate assumption of 0.67% (flat versus 4Q25), I arrive at 481,940 loans originated. Applying a Revenue per loan of $467.90 to that (down 4% QoQ, effectively the same decline experienced from 3Q25 to 4Q25), yields $225.5M in total core revenue. Adding together the $75.2M and $225.5M estimates total $300.7M in 1Q26 revenue, closely aligning with my previous $299.9M estimate. These are not necessarily my final estimates, but it's how I'm thinking about the quarter today. I will be closely monitoring review trends in April leading into ER to try and get a gauge for how 2Q26 is trending. Right now, despite the tumultuous headlines, I am not seeing any direct impact on Upstart visible in 1Q26. Of course, I can be totally wrong on that. Believe it or not, I am not an insider lol. But back in 3Q25, I sounded the alarm when #UTPI fell rapidly, and it turned out Upstart had tightened their models. As of today, I am not seeing anything in the data that is overly concerning. 🫡

English es obviamente un lingua romance al core e would be vastly meliorated by le removal of le barbaric Germanic elements.