@BickerinBrattle That's why you find exposure pre-IPO and sell on the the actual offering. Buy the rumor sell the news, as ever.

Then you can round trip and an buy again when the lockup creates a cheaper price.

English

Murph | Modern Macro Technician

206 posts

@MatthewNMurphy

Macro investing through a technical lens. Regime, Liquidity, Trend, Momentum, Reversion. Price is the final arbiter.

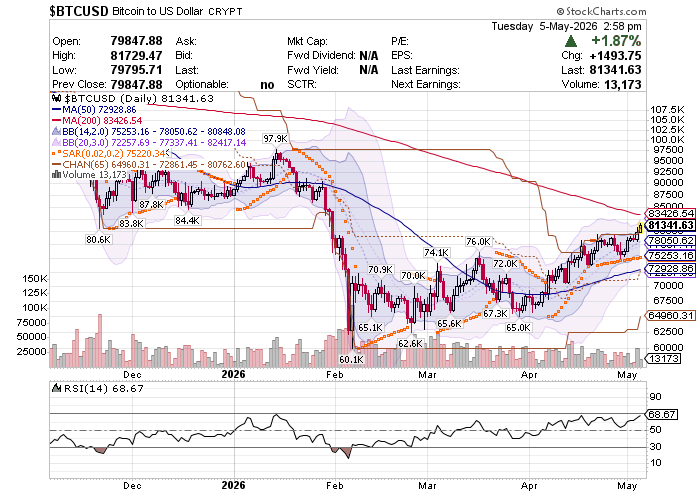

"They are not going to be able to raise rates." Jordi Visser (@jvisserlabs) ran capital at Weiss Multi-Strategy Advisers as CIO. 30 years on Wall Street. Built one of the first volatility-arbitrage frameworks for systematic hedge funds. Managed billions through three crises, never had a thesis-driven blow-up year. "Interest payments on US debt are now bigger than what we spend on defense. Over a trillion dollars a year. This is what Bitcoin was made for." We cover: — Why the Fed is mathematically trapped and how the trillion-dollar interest math forces every policy decision from here — Why "bubble talk" is intellectually lazy: PE goes UP in bubbles, not down, and right now PE is contracting while earnings grow 27% — The AI-agents-eat-tokens thesis: why agentic AI doesn't care about dollars and what that means for compute-backed assets — Why belief is harder than fundamentals: fundamentals come and go, belief systems don't, and which belief is breaking in 2026 — The Bitcoin call no other macro guy on Wall Street will make publicly: new all-time highs before year-end — Why most hedge funds will underperform Bitcoin this cycle and the structural reason it has nothing to do with crypto — The single chart that made Jordi go from skeptic to allocator and why it hasn't reversed — What the 2020-2026 monetary regime actually was, named correctly for the first time Thanks to Jordi for coming on @new_era_finance. Highlights: 00:00 - Intro 00:42 - Bitcoin Lagging 03:16 - AI Investment 07:14 - Price vs Narrative 12:15 - Market Dynamics 21:28 - AI Trading 25:24 - AI Democratizes Wealth 36:26 - Crypto Transition 39:40 - Elliott Waves 44:08 - Banana Zone 49:37 - Fundamentals vs Technicals 55:14 - Ethereum Future

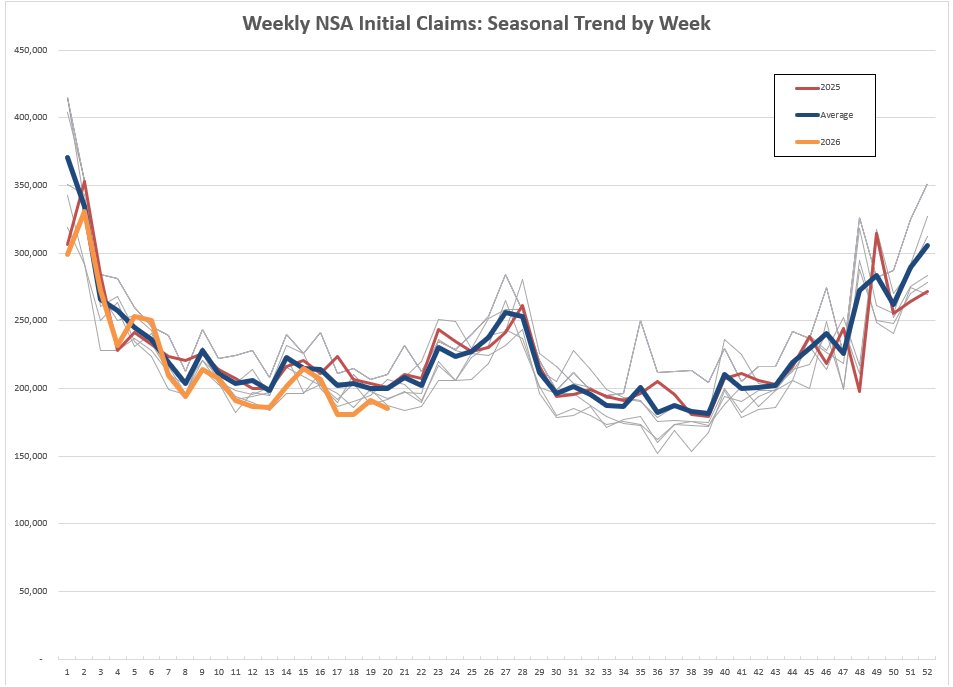

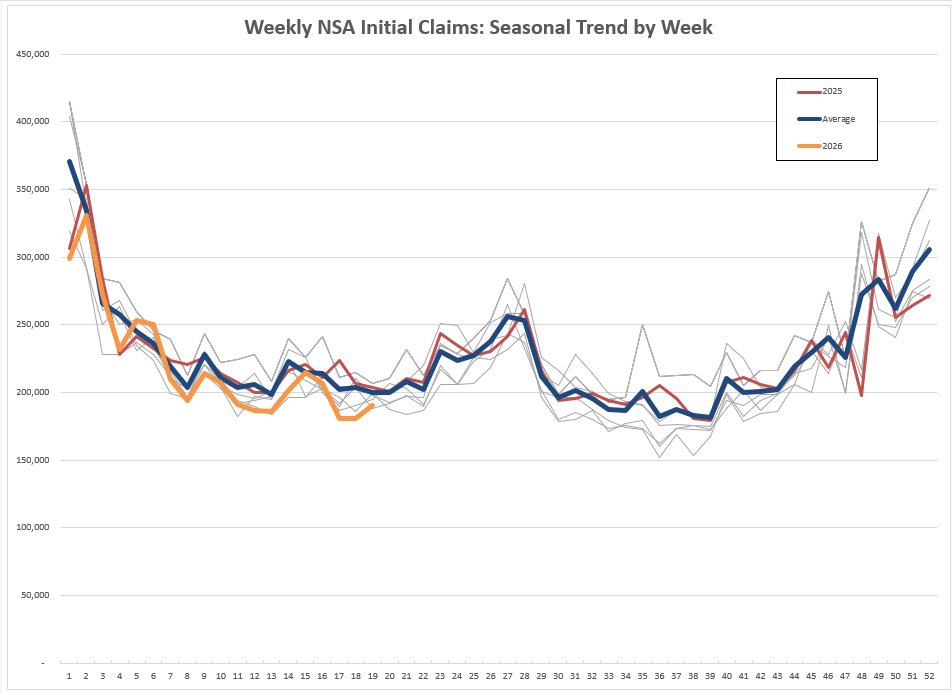

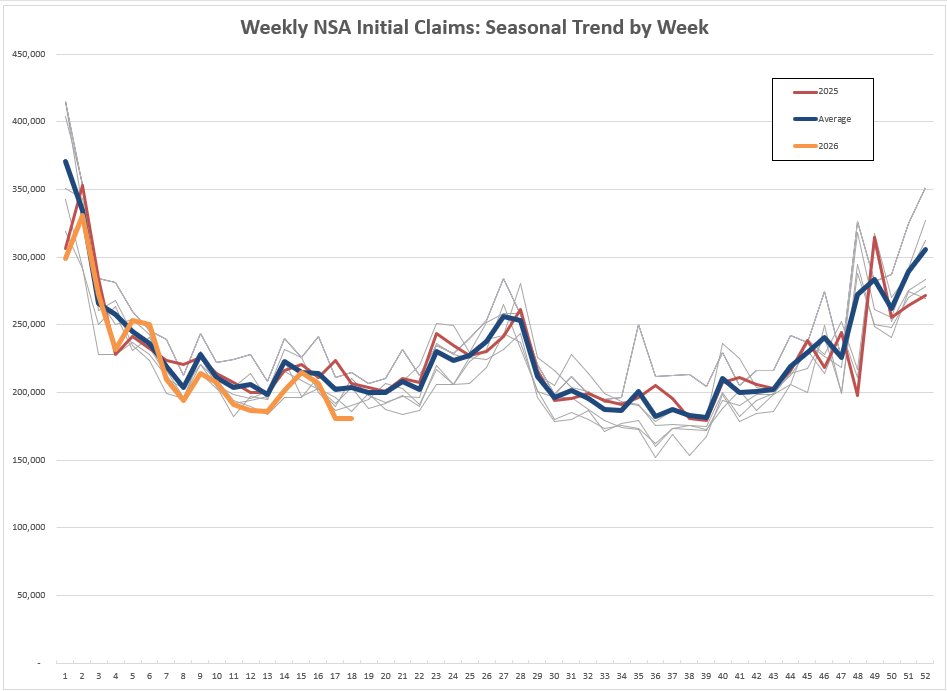

NSA Initial Claims remain clean as a whistle at 185k

Two takeaways from May’s BofA fund manager survey: first, equity allocations surged by a record amount on the month, and second, 40% of respondents see a second wave of inflation as the biggest tail risk. The two ideas are connected: stocks are increasingly seen as an inflation hedge

Welcome to the most asymmetric trade in modern financial history. The thread below lays out why. The opportunity exists because capital has chased the AI trade while ignoring the physical assets AI requires to run — assets that have quietly become the best-performing asset class of the decade. Since October 2020 when we first called for the commodity super cycle: QCI Total Return +217%, GSCI Total Return +205%, Gold +140%. NASDAQ trails at +130%. S&P 500 at +85%. The top three are all commodities. Yet oil cannot get out of its own way while copper and the broader atom complex prints fresh highs . That is the dislocation. That is the trade. Get long. Buckle in. Hang on for the ride. Forgive the longer posts in this thread — attempting to mimic my old 10-bullet commodity takes. On to it.

Deficit spending (public + private) seems to be sufficiently strong to support high levels of aggregate demand/petroleum consumption at current prices.