orwellvalley@orwellvalley

Well here's an update on the situation...

Mortgage paid off.

Security not included.

I live in a flat I 'own'.

I pay high service charges for a very modest home.

No mortgage.

No bank.

No lender breathing down my neck.

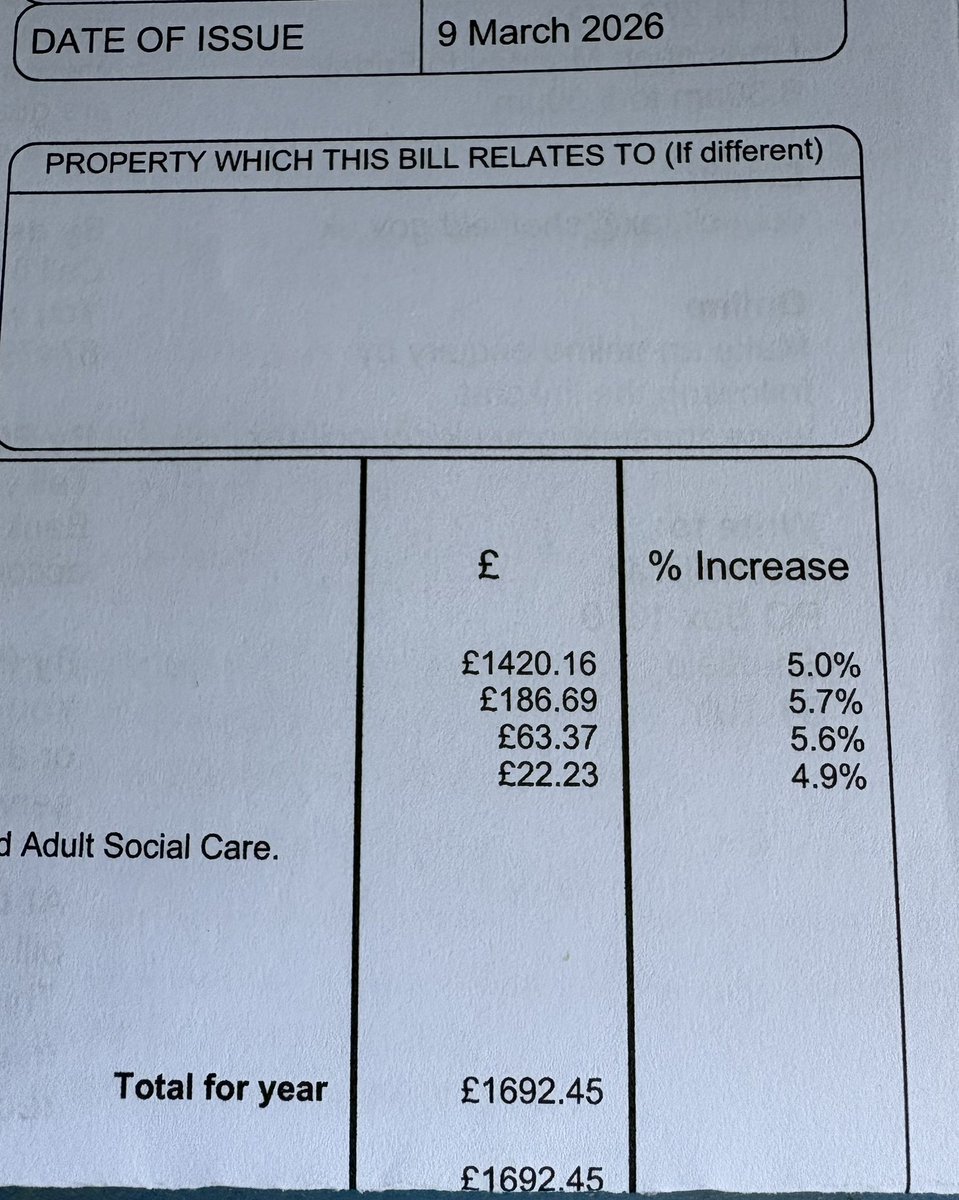

And yet by the end of April, I’m expected to find £9,000 immediately - with another ~£4,000 due in September.

Not for something new.

Not for something optional.

But for historic costs tied to a building I bought in good faith - assuming it was structurally sound, properly converted, and fit to live in.

I tried to be reasonable.

I offered a repayment plan. £50 a month. ON TOP of £425 service charge for an unsaleable equity shedding cupboard in Bolton.

£50 a month? Not perfect - but real. Sustainable. Honest. The response?

A flat rejection. Pun intended.

Not adjusted. Not discussed. Not negotiated.

Rejected.

Because the lease says payment is due “forthwith” - immediately - and anything else simply doesn’t fit the system.

And then comes the part that really tells you everything.

I’m told they can’t offer a repayment plan because:

• They’re not authorised to provide credit

• And doing so would breach their charitable aims

Read that again.

Helping someone spread payments over time - to avoid financial collapse - would somehow conflict with being a charitable organisation.

So instead, the "charitable" approach is:

• Demand the full amount immediately

• Reject any realistic repayment proposal

• Proceed with debt recovery if unpaid

• And ultimately threaten forfeiture of the lease

Debt Collection first. Then ultimately Yep - forfeiture, they've mentioned we'd be in breach of the lease. So yes they can do that.

The legal mechanism where you can lose your home entirely. A home you’ve already paid for.

There’s even a quiet warning built in.

Interest at 3% above base rate hasn’t been applied yet…but might be from April if the balance isn’t cleared.

So the pressure isn’t just financial.

It’s escalating. Timed. Engineered to close in.

And this is all happening within a system where service charges are only supposed to be payable if they are “reasonably incurred.” Well, That’s the theory.

The reality?

Years after major works.

After tribunal proceedings.

After residents have already stretched themselves to breaking point…

We’re still here. Surviving from week to week - just.

Still paying.

Still absorbing the consequences of decisions we never made. These are leaseholders who had to wait til pay day to find £100 towards our legal defence.

This is the part people don’t understand about leasehold until they live it.

You don’t really own your home.

You carry the liability.

You absorb the risk.

You fund the failures.

But control?

That sits somewhere else entirely. And you feel it flex. It reduces every week to a fight or flight response.

Right now, the cost of simply remaining in my so-called mortgage-free flat is pushing towards the equivalent of a second mortgage.

Except unlike a mortgage:

• No negotiation.

• No flexibility.

• No safety net.

Just a demand.

• £9,000 by April.

• £4,000 by September.

Mortgage: paid.

Security: none.

If you want to see how detached decision-making can become from real human impact…

Try being a leaseholder.