English

Upstream Ag

541 posts

@UpstreamAg

Essential news & analysis for agribusiness leaders◾️◾️◾️ |⬇️Weekly Newsletter|

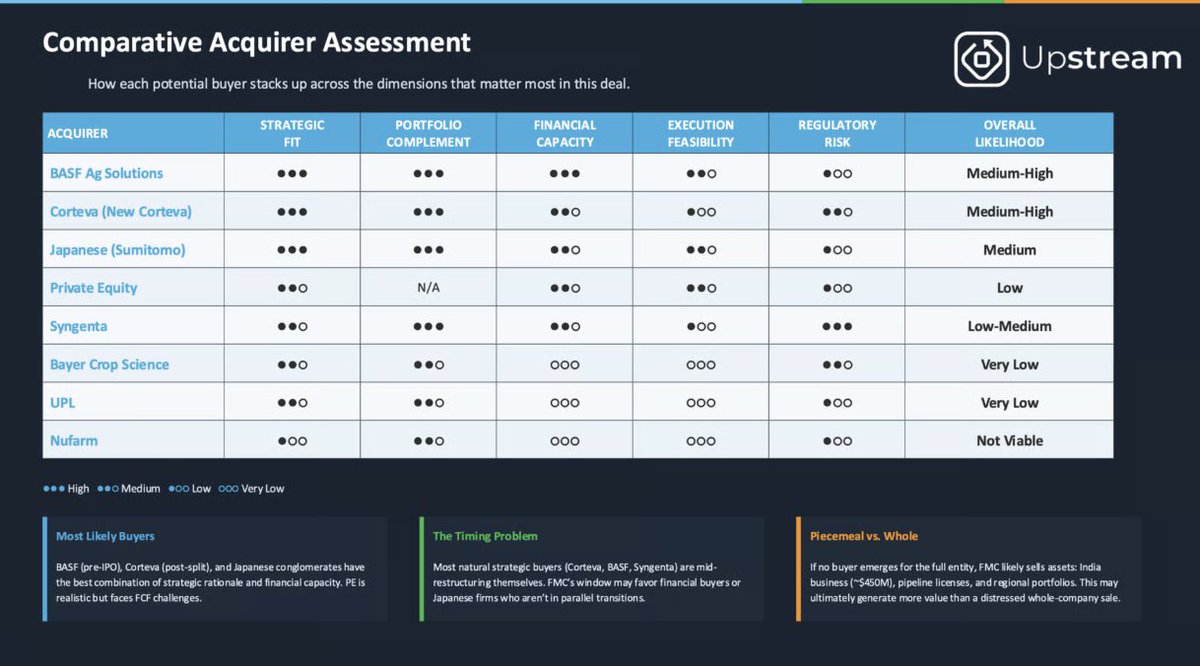

Upstream Ag Professional - Week of October 19th 2025 ◼︎◼︎◼︎ This week's essential news and analysis for agribusiness leaders includes: 1. The Danger of Dominant Logic: What Pioneer Hi-Bred's Blind Spot Reveals About Disruption in Agriculture A look at disruption as a tax on not innovating vs. outright being "Blockbustered." 2. @AscribeBio Closes $12 Million Series A A detailed look at the product, the strategy, the fundraising process and the future of a biocontrol leader. 3. @ecorobotix Crosses Over $200 million Raised: A look at Revenue, Business Model, GTM and Paths to Exit 4. Agtech trends: bundling, unbundling, LLMs and more with @tenaciousvc own J. Matthew Pryor and @svnoles Nolet with @UpstreamAg 5. Momentum and Milestones: @NewLeaf_Sym Aims to Double Sales Next Year A look at layered crop protection and COGS enabling GTM in biocontrol. 6. Q3 2025 AgTech Venture Capital Investment and Exit Round Up by Image below. 7. Commercializing Ag Products: From R&D to Farm Gate and tying it into Upstream Ag Insights Competing on Analytics and the Future of Ag Input Commercialization @DamianPMason 8. Integrated insights from The Pacesetter Pod on Agribusiness 2026 M&A Outlook with Scott Porter of Cascadia Capital Partners with Capital Allocation Lessons from Henry Singleton + more! upstream.ag/p/upstream-ag-…