Pinned Tweet

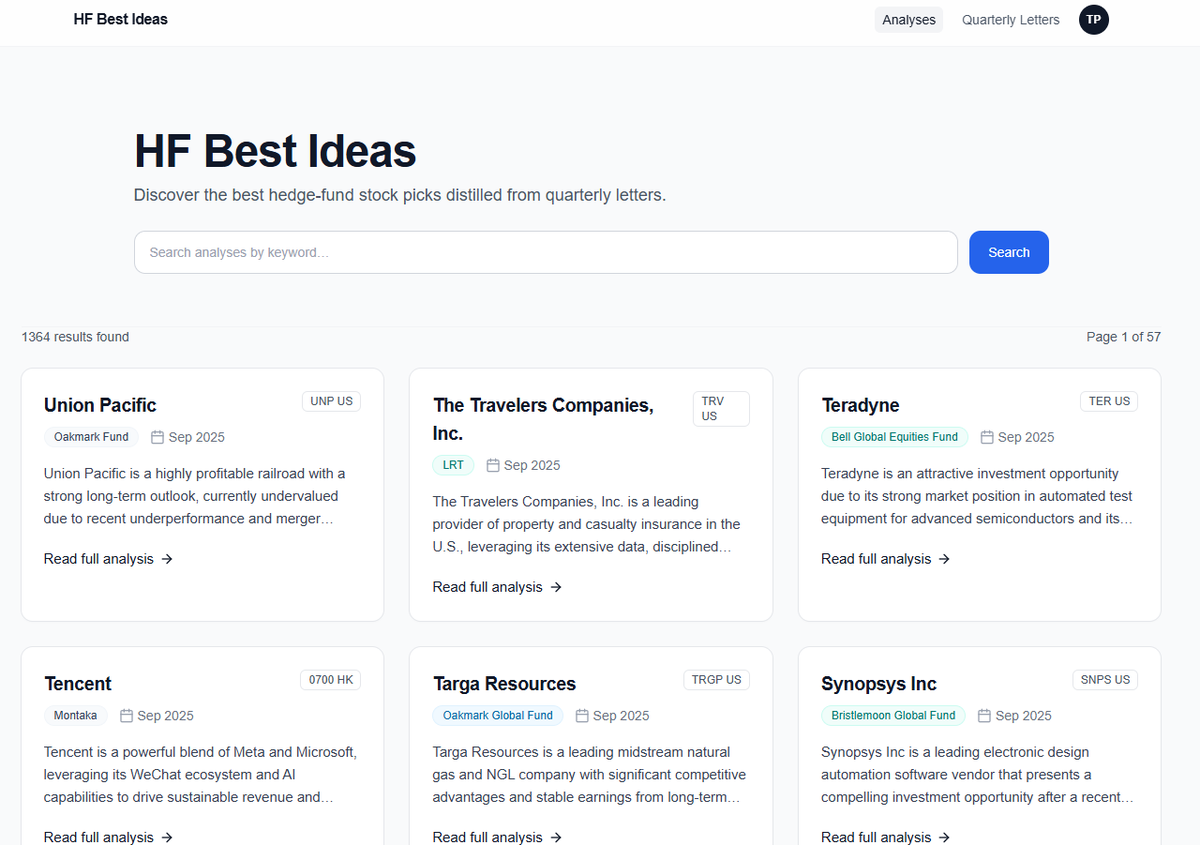

HFBestIdeas.com is now live.

It’s free (for now), you just need to create an account.

Two main features:

1️⃣ Access to 1,000+ quarterly fund letters

2️⃣ Around 500 stock pitches extracted from fund letters each quarter

English

Stock Analysis Compilation

4.4K posts

@StockCompil

I compile hedge fund pitches Database: 1500 pitches & 1300 fund letters ↓ https://t.co/P8lwLZf1zW Newsletter : https://t.co/iamuv6oatz