Tweet fijado

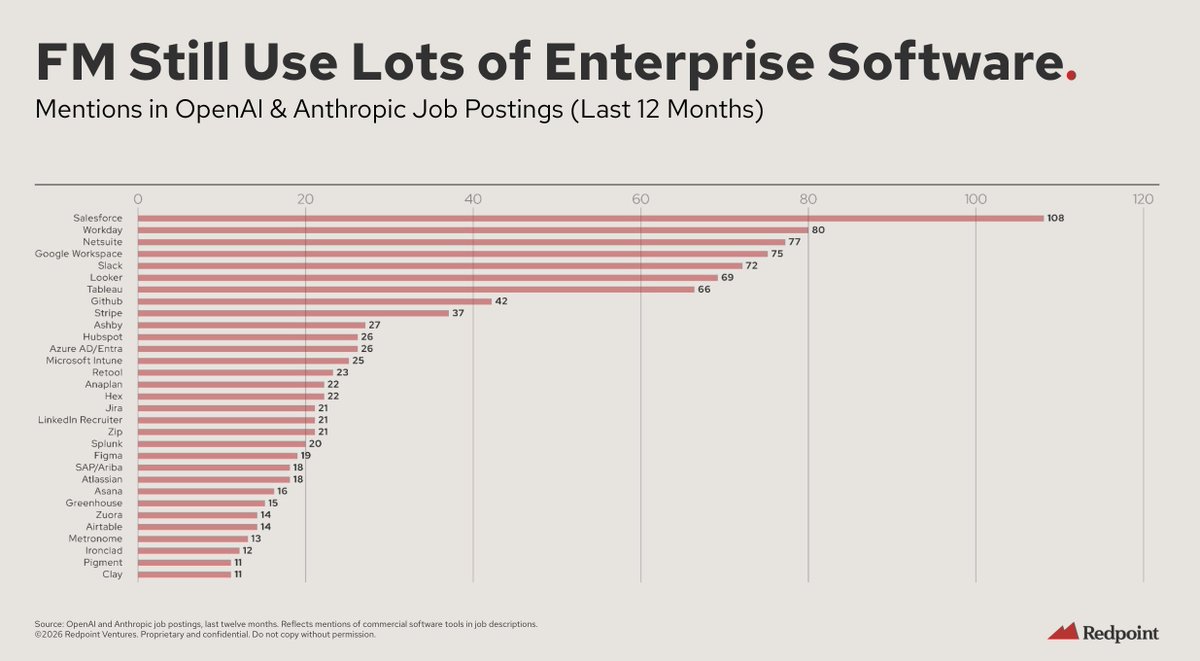

Wild Prediction: While Anthropic is paving the path and leading the charge in enterprise AI, the long term winner will be $MSFT. They already own distribution and it's only a matter of time until they leverage OAI to build competing enterprise services. Distribution always wins.

English