@VladBastion Cyclicals always look cheap on peakish earnings

English

Quality Capital

242 posts

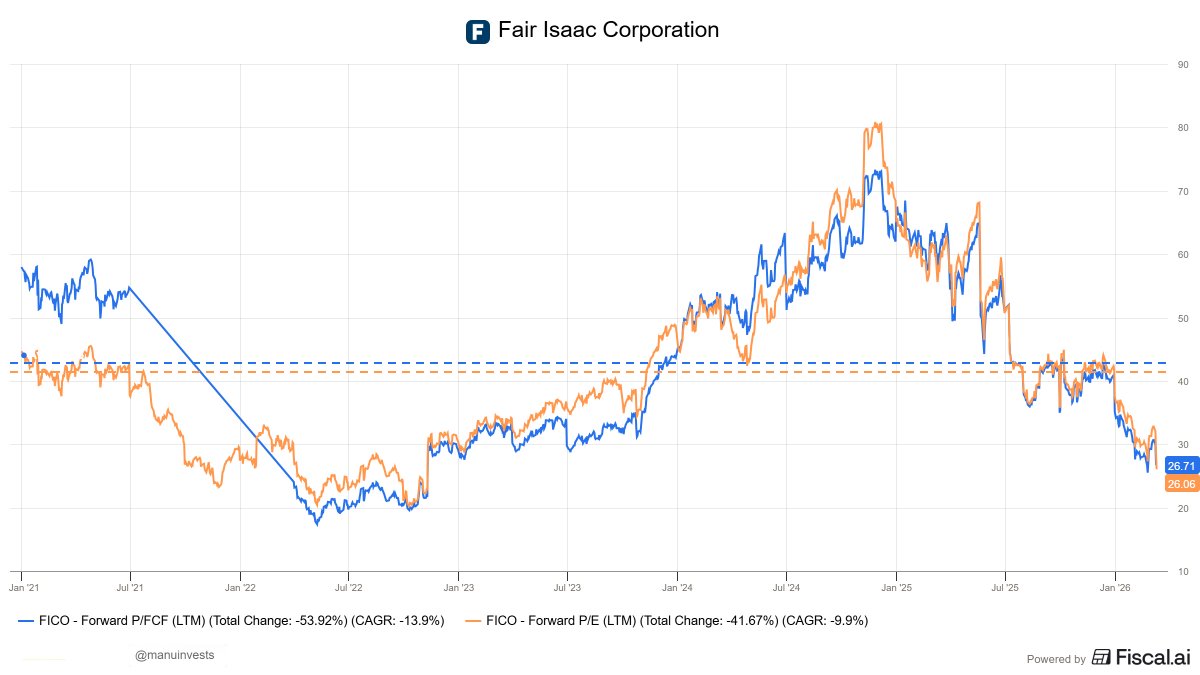

Bristlemoon just published a 16k+ word report on $FICO, the credit score monopolist that has increased its mortgage scores prices by 800% over the last three years. We explore how entrenched FICO is in the US credit ecosystem and whether the company still has pricing power...

Bristlemoon just published a 16k+ word report on $FICO, the credit score monopolist that has increased its mortgage scores prices by 800% over the last three years. We explore how entrenched FICO is in the US credit ecosystem and whether the company still has pricing power...

Can anyone give me a valid $FICO bear argument other than the government will regulate them to the ground (whatever that even means)

I just $FICO is really expensive for what they do.