Tweet fijado

the most bullish thing in the entire $QS Q1 investor letter wasn't a battery metric. it was a customer saying "we tested you against the competition and want to keep going."

ir.quantumscape.com/static-files/6…

English

Highly Regarded Star 🪨

374 posts

@SpongeQuant

Starfish on @X | NYC M&A | $RDDT $BABA $QS Long strong businesses, occasionally buy degenerate calls. Building a Fintwit win-rate tracker with unemployed SWEs

The most consequential event of an entire company’s history. Got released today with a photonics player. Making them the functional standard laser for CPO, Pluggables, and SiPH. For companies like $NVDA, $AVGO, $AMD, to $MRVL using the foundry. Does anyone know the name?

$MRVL Jensen just said Marvell will be the next trillion dollar company

Chipmaker CXMT Is Cleared for Chinese Mainland's Biggest IPO in Four Years buff.ly/A6EAeUu

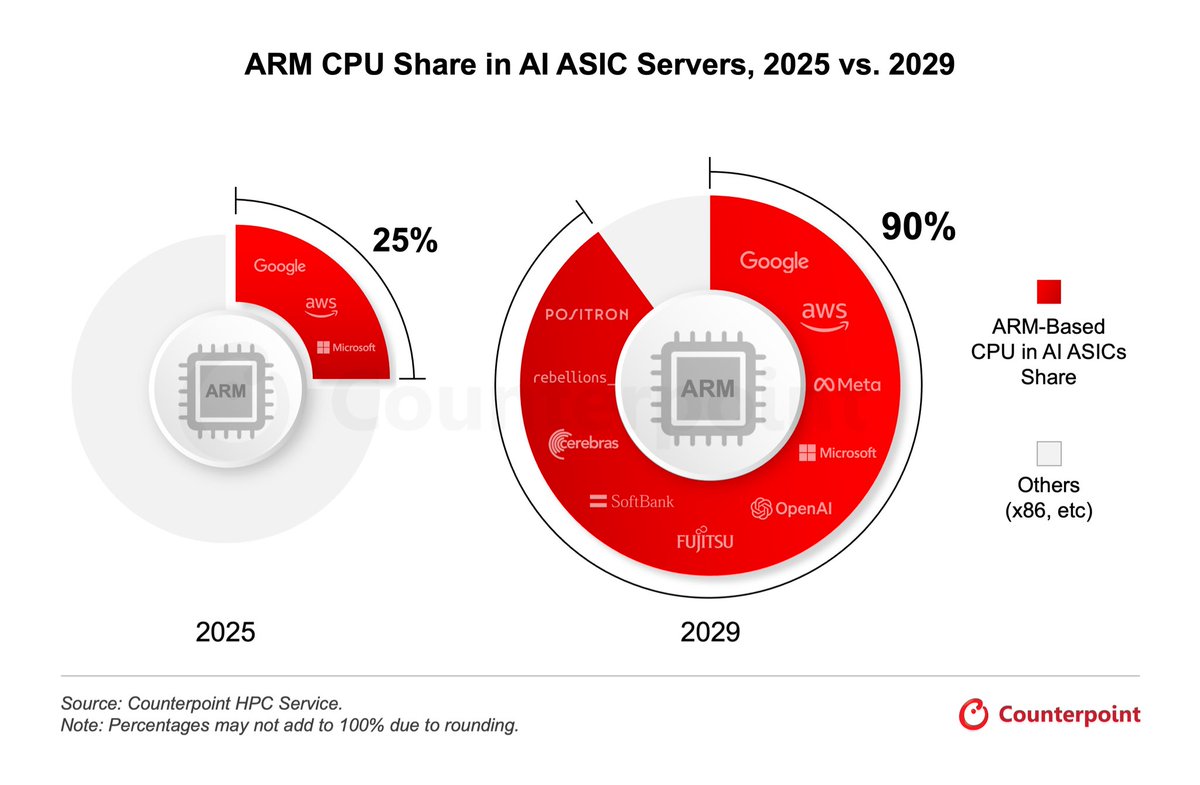

Bullish on $ARM, given the new bottleneck shifting back to CPUs. MS shows stuff like Orchestration/RAG requiring CPUs. But I'm predicting parts of localized inference to be handled by CPUs more and more... as models like Gemma get lightweight in the future. Not every robot needs to be able to solve the mysteries of the universe. Data centers will need an astronomical amount of traditional CPU compute (AWS Graviton, $GOOGL Axion, and $MSFT Cobalt), which are all ARM based. $META + OpenAI are also buyers of the AGI CPU. And AI will flow down to edge. $15B annual revenue target.. Starting to look reasonable?

$QS: My one post summary of @QuantumScapeCo 👇 PROVEN TECHNOLOGY + Two major innovations: anodeless architecture (at manufacturing) and proprietary solid ceramic separator + Cathode agnostic + The only NO-COMPROMISE solid state battery solution which makes no sacrifices on the 5 main factors of battery design: Energy, Fast Charge, Life, Safety, and Cost + QSE-5: ~5 Ah cell with energy density 844 Wh/L capable of <15-min fast charge (10 to 80% State of Charge) + A0 Sample tested by Volkswagen's PowerCo for >95% energy retention at >1,000 full cycle equivalents + Safety: Solid-state ceramic separator is nonflammable and noncombustible + Cost (at scale): Eliminates anode host material and related manufacturing costs. This removes dependency on China-dominated graphite anode supply chain. + Operates at low pressure of <3.4 atm. No external pressure system required! + Implemented QSE-5 battery cells into a modified Ducati V21L race motorcycle in September 2025 + Cobra process shrunk ceramic baking process from many hours down to several minutes + Eagle Line, QS's pilot production line, has begun producing initial volumes of QSE-5 cells + 18-month cycles expected for new iterations of technology PARTNERSHIPS + Non-exclusive licensing agreement for up to 85 GWh with Volkswagen Group's battery subsidiary: PowerCo, including $130M of milestone payments + $130M of royalty prepayments + Joint Development Agreements with 2x Top 10 (by revenue) Global Automotive OEMs + Successfully completed technology evaluation phase with another Top 10 Global Automotive OEM, which will lead into another JDA + Total 4 out of the Top 10 Global Automotive OEMs will have a JDA or more advanced, with QS + Capital-light licensing agreement is a template for for all JDAs + OEM partners range from Japan, North America, and Europe + Ecosystem Partners: Murata in Japan and Corning in the US. Collaborations to pursue high-volume manufacturing of ceramic separators for QS’s solid-state battery technology + Agreements with other automotive OEMs: leading OEMs by global revenue, established global luxury OEM, premium performance OEM, and pure-play EV OEM + Agreements in other sectors: consumer electronics, stationary storage NON-EV APPLICATIONS + Corning: Consumer electronics, medical devices, military applications, and grid storage applications + AI data centers are transitioning to 800V DC designs and adopting power systems architecture and technology from the EV industry. A "natural fit for our no-compromise solid state battery". + Defense sector: "In addition, we have seen strong customer interest in our battery technology from global players in the military, aerospace and government sectors. Our battery technology unlocks step-change improvements to both energy density and power simultaneously; combined with the superior safety of our solid-state design, this is a highly attractive combination for these advanced applications. Our anode-free architecture also has supply-chain benefits. Conventional lithium-ion batteries require graphite that is almost exclusively sourced from China. In contrast, our battery design is graphite-free, eliminating a major pain point for defense applications." CASH/LIQUIDITY + Ended Q1 2026 with $904.7M + Cash runway plus expected customer billings are anticipated to be sufficient to the end of 2029 2026 ROADMAP + Demonstrate scalable production with the Eagle Line + Advance automotive commercialization + Expand into new high-value markets + Go beyond QSE-5