Tweet épinglé

mgb

14.1K posts

mgb

@MyrtleBeachWeek

- low level economist - purveyor of beach houses - cancer survivor - will tilt wind-powered electron generators

North Myrtle Beach Inscrit le Nisan 2009

2.5K Abonnements2.1K Abonnés

English

@MyrtleBeachWeek @asuka_aryan @Selkis_2028 That’s not what Asuka is saying. Asuka is saying that Jewish people want to erase White people.

Nice strawman, though.

English

Larry Fink is Jewish. Every single time that you find the source of an anti White agenda you will find a long list of Jews such as those that are amongst the top executives at BlackRock.

Harrison H. Smith ✞@HarrisonHSmith

The Woke Era was literally created, enforced, and implemented by Blackrock. They used it to drive a generation of White men out of the establishment, and after ten years, the effects are irreversible and so they are pretending to oppose it. Larry Fink is a criminal.

English

2008 had the entire fiasco tied to all of the homes, so a foreclosure avalanche ensued.

Private credit collapse destruction will fall primarily on the now-gated off investors.

How is the Private Credit fund investors' loss more contagious than something like a major market correction with similar size losses?

Owen Gregorian@OwenGregorian

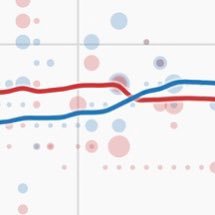

Subprime Crisis 2.0: Will Private Credit Be The Trigger? | Tyler Durden, Zerohedge We have recently tackled the rising stress in the Private Credit markets. Here are a few of our previous warnings: - Fitzpatrick: Soros CEO & CIO Warns of a Reckoning - Private Credit Stress: Will The Fed Backstop Exuberance Again? – RIA - Is Private Equity A Wolf In Sheep’s Clothing? After 30 years of watching credit cycles expand, distort, and collapse, I’ve learned one reliable rule: “When enough people start drawing comparisons to 2008, it’s worth stopping to check whether the analogy holds up — or whether fear is doing the analytical work for them.” Right now, judging by the amount of commentary on social media, the stress in the private credit market has everyone’s attention. Most of the commentary being generated makes the immediate jump from private credit firms “gating” exits to the onset of the next subprime crisis in the financial system. Those claims are certainly alarming and generate many clicks and views, but the question is whether those claims are based on facts rather than opinions. Just recently, Goldman Sachs CEO David Solomon flagged the risk of private credit in his annual shareholder letter. Lloyd Blankfein, who piloted Goldman through the Global Financial Crisis, warned publicly that the financial system appears to be “inching toward another potential catastrophe.” Meanwhile, Goldman’s own research arm published a note concluding that private credit stress is “unlikely to generate large macroeconomic spillovers on its own.” So which is it? A repeat of the subprime crisis of 2008, or a painful but contained credit cycle? The honest answer most likely sits somewhere in between, and understanding exactly where private credit differs from subprime tells you a great deal about how worried you should actually be. Let’s revisit 2008. What Made The Subprime Crisis So Catastrophic It is hard to believe that we are rapidly approaching the 20-year anniversary of the “Great Financial Crisis” that nearly destroyed the financial system as we knew it. There are many investors and commentators in the markets today who only know about the event from reading history books. Having lived through it, it is a different reality. Crucially, the 2008 subprime crisis wasn’t simply a mortgage problem. It was a leverage-and-derivatives problem that started in mortgages. That distinction matters enormously when you’re sizing up today’s private credit stress. At the heart of the crisis was a product called the collateralized debt obligation, or CDO. Banks packaged pools of subprime mortgages into tranches, which were rated by agencies using flawed models. Those CDOs were then re-sliced into “CDO squared” structures, layering additional complexity and opacity on top of already opaque assets. The real acceleration came when synthetic CDOs entered the picture. Unlike cash CDOs, which required actual mortgages, synthetic CDOs referenced mortgages through credit default swaps. Journalist Gregory Zuckerman found that while roughly $1.2 trillion in subprime loans existed in 2006, synthetic structures created more than $5 trillion in exposure referencing those same loans. The CDS market alone reached a peak notional value of $62.2 trillion by year-end 2007. That is not a typo. But the derivatives machine required raw material to function, and Wall Street’s insatiable hunger for collateral triggered what historians of the crisis now call the “race to the bottom” in mortgage underwriting. To keep the CDO assembly line running, originators needed volume. That demand for volume led to a collapse in underwriting standards. By 2006, no-money-down mortgages were commonplace. - NINJA loans, “No Income, No Job, No Assets,” were extended to borrowers who could not remotely service the debt once introductory teaser rates reset. - Stated-income loans, in which borrowers self-reported earnings with no verification, became the industry norm rather than the exception. - Adjustable-rate mortgages were sold to buyers who qualified only at the teaser rate and had no capacity to absorb resets of 3 to 4 percentage points two years later. The Mortgage Bankers Association later estimated that subprime originations reached $600 billion in 2006 alone, up from roughly $160 billion in 2001. Most importantly, the loans were designed to be sold, not held. In other words, the originator of the loan bore no long-term risk and had every incentive to close as many transactions as possible, regardless of quality. That single misalignment of incentives was the original sin of the entire subprime crisis. What compounded the damage beyond even that was systematic, institutionalized fraud at the origination and securitization level. The Financial Crisis Inquiry Commission documented widespread “robo-signing,” where bank employees executed thousands of mortgage documents per day without reviewing them. They affixed signatures and notarizations to paperwork they had never read. Countrywide Financial, Washington Mutual, and others were found to have misrepresented loan quality in the representations and warranties they made to investors purchasing MBS tranches, fraudulently inflating the apparent collateral quality of the pools they sold. Appraisers faced pressure, and in many cases direct financial incentive, to hit predetermined valuations that supported loan amounts the underlying properties could never justify. The FBI reported that mortgage fraud suspicious activity reports increased by more than 1,400% between 2000 and 2007. When losses eventually surfaced, investors discovered they had purchased securities backed not just by bad loans, but by fraudulently documented ones. That distinction made recovery values nearly impossible to model and turned settlement litigation into an industry unto itself for a decade afterward. JPMorgan alone paid $13 billion in 2013 to resolve government claims over mortgage securities, and that figure represented only a fraction of industry-wide settlements. When housing prices began falling, that entire structure detonated in both directions simultaneously. Banks that held CDO tranches faced mark-to-market losses. Banks that sold CDS protection, AIG being the most famous, faced collateral calls they couldn’t meet. Here is the most crucial point. These instruments traded freely in liquid markets, so price discovery occurred in real time, compressing the panic into a matter of weeks. The interconnection was total. Twelve of the thirteen largest U.S. financial institutions were at risk of failure, according to then-Fed Chair Ben Bernanke. That’s what systemic risk actually looks like. Private Credit Stress Is A Different Animal The private credit market now stands at roughly $1.7 to $2 trillion in deployed capital, a figure that has grown rapidly since banks retreated from middle-market lending after the Global Financial Crisis. That growth is precisely what generated the current stress. Redemption requests have surged across major platforms. Blackstone’s BCRED fund saw record redemptions of $3.8 billion in Q1 2026, exceeding its 5% quarterly buyback limit. Apollo, Blue Owl, and Morgan Stanley’s North Haven fund have all imposed withdrawal restrictions. That gating of withdrawals led to an obvious decline in inflows across retail private credit funds. Those inflows fell to roughly half their 2025 pace, according to Goldman Sachs estimates. So far, the catalyst is concentrated in software companies, which represent an estimated 15% to 25% of many private credit portfolios. They are under pressure as AI disruption fears potentially erode their earnings power and their ability to service debt. The headline default rate sits around 2% as of 2025, but Goldman Sachs Asset Management’s own research acknowledges that figure understates the true level of stress. When you include liability management exercises and distressed exchanges, the real rate approaches 4% to 5%. That’s meaningful deterioration. It’s not catastrophic, but it’s real. J.P. Morgan’s analysis showed that for senior direct lending to produce negative total returns, default rates would need to exceed 6% while recovery rates would collapse below 40% simultaneously. Those numbers have historically appeared only during COVID and the Global Financial Crisis itself. That’s a high bar — but it’s not an impossible one. However, that would require a deterioration in macroeconomic conditions, a continuation of the Iran conflict oil shocks, and a contraction of consumer spending, which could certainly amplify risks. As shown below, the current structural comparison between the subprime crisis and the private credit sector today is markedly different. The Importance of the Gating System The most structurally significant difference between 2008 and today is also the one that generates the most debate. Unlike the subprime crisis, private credit funds can gate their exits. When Blackstone caps BCRED redemptions at 5% per quarter, it’s not a failure of the fund; it’s the mechanism working as designed. In 2008, there was no such circuit breaker. MBS and CDOs traded continuously in secondary markets, meaning every forced seller found a bid at a lower price, triggering more mark-to-market losses, which in turn triggered more forced selling. The feedback loop was instantaneous and brutal. Gating slows that process considerably. LPL Research noted that while gating makes for terrible headlines, it prevents the forced liquidation that accelerated subprime losses. Goldman Sachs estimates that retail private credit inflows will remain in net outflow throughout 2026 and likely into 2027, a slow bleed, not a cliff. That’s a very different contagion profile. That said, gating is not a cure. It transfers the problem in time, not away from investors. Those sitting in redemption queues face a multi-year wait to exit positions that may continue to deteriorate. The opacity of private credit portfolios and manager-reported valuations means stress can accumulate invisibly until it can’t. “The key risk in private credit is not what is visible, but what remains hidden.” – The Daily Economy Goldman Sachs economist Manuel Abecasis concluded that, even in an adverse scenario, private credit stress would only drag on GDP by 0.2% to 0.5%. His reasoning is straightforward: the private credit sector holds about $1.7 trillion in levered loans, or roughly 4% of all credit to the private non-financial sector. That’s is not nothing, but it’s not the $62 trillion CDS market either. Goldman also notes that bank lending to businesses has actually accelerated recently, providing a partial offset if private credit tightens. Blankfein’s view carries different weight precisely because he’s been through the real thing. He warned that private credit assets “can be hard to analyze, may feature hidden leverage, and can become tough to sell.” He’s right that opacity and illiquidity create conditions where problems compound before they surface. The question is whether those conditions, combined with a still-manageable scale, produce systemic contagion or simply painful losses for a subset of investors. “Private credit stress is unlikely to generate large macroeconomic spillovers on its own.” — Goldman Sachs Economist Manuel Abecasis, March 2026 I’m inclined to side with Goldman’s macro conclusion. However, with a caveat that matters. The base case holds only so long as private credit problems don’t compound with a broader recession, a sustained oil shock from the Iran conflict, and a sharper-than-expected deterioration in software company cash flows. Any two of those three conditions occurring simultaneously change the calculus. Goldman’s own research acknowledges this. The bigger risk isn’t private credit alone. It’s private credit stress coinciding with the wider tightening of financial conditions. What Investors Should Pay Attention To The structural differences between today and the subprime crisis are real and important. There’s no synthetic subprime CDO chain multiplying private credit losses to a $5 trillion notional exposure. Most critically, the investor base is primarily institutional, not retail money market funds holding fraudulently rated paper. Fund-level leverage is modest, and the gating mechanism, whatever its imperfections, prevents the instantaneous price cascade that made the subprime crisis so destructive. What this most closely resembles is a normal credit cycle playing out in an untested asset class. Not a systemic collapse, but not a benign correction either. Goldman Sachs Asset Management’s own European research found that “stress events are likely to remain elevated relative to the last decade,” concentrated in smaller companies and cyclical sectors. That pattern will probably hold in the U.S. as well. Three things would change my view and warrant genuine alarm. - First, if default rates push past 8% in tech-heavy private credit portfolios as AI disruption accelerates. - Second, if bank credit facilities to private credit managers get pulled at scale, triggering forced asset sales. - Third, retail penetration of private credit grows, as institutional investors sell, leaving less-sophisticated money to hold the bag. None of those conditions is inevitable. All of them are possible. The subprime crisis analogy fails on the specifics. But the lesson from the subprime crisis isn’t about CDOs. It’s about what happens when credit markets expand rapidly, underwriting discipline erodes under competitive pressure, and opacity masks deteriorating loan quality. On those broader conditions, the warning is more relevant than the Goldman bulls would like to admit. That is why we continue to underweight risk for now until we have better clarity about the future. Key Catalysts Next Week This is the most structurally loaded week of the quarter. The calendar stacks a Q1 close, a Q2 open, and a full employment gauntlet into five sessions, with markets still metabolizing whatever the Fed just delivered.. Tuesday is the pivot. Consumer Confidence is the marquee release, and it’s the first full-month reading that captures the Iran conflict, the tariff widening, and February’s payroll shock in a single survey. The prior print of 91.2 was already soft. The Expectations component, which the Conference Board flags as a recession signal below 80, is the number to watch. A sharp drop would validate the stagflation fears the Fed just tried to navigate around. Chicago PMI and Case-Shiller Home Prices round out the morning, and then Q1 closes at the bell. Expect elevated volume as pension funds and mutual funds finalize window dressing and mark final positions, totaling roughly $62 billion on the buy side. Wednesday flips the calendar to Q2 and immediately delivers a triple shot: ADP private payrolls, ISM Manufacturing, and JOLTS. After February’s -92,000 NFP shock, the ADP print will either stabilize the labor narrative or accelerate the deterioration thesis. ISM Manufacturing is the tariff passthrough read, the Prices Paid subindex will tell us whether producers are eating costs or passing them through, while New Orders reveal whether demand is contracting under policy uncertainty. JOLTS completes the picture with the openings-to-unemployed ratio that the Fed uses to assess labor market slack. Friday is the week’s anchor: March Nonfarm Payrolls. February was distorted by a Kaiser Permanente strike and severe weather, giving bulls a one-month excuse. If March payrolls bounce back above 100,000, the “transitory weakness” camp wins. If they print flat or negative again, the labor market deterioration becomes undeniable, and the pressure on the Fed to act, despite sticky inflation, becomes immense. ISM Services PMI that morning adds the services-sector inflation read alongside Wednesday’s manufacturing data. zerohedge.com/markets/subpri…

English

2008 had the entire fiasco tied to all of the homes, so a foreclosure avalanche ensued.

Private credit collapse destruction will fall primarily on the now-gated off investors.

How is the Private Credit fund investors' loss more contagious than something like a major market correction with similar size losses?

English

Subprime Crisis 2.0: Will Private Credit Be The Trigger? | Tyler Durden, Zerohedge

We have recently tackled the rising stress in the Private Credit markets. Here are a few of our previous warnings:

- Fitzpatrick: Soros CEO & CIO Warns of a Reckoning

- Private Credit Stress: Will The Fed Backstop Exuberance Again? – RIA

- Is Private Equity A Wolf In Sheep’s Clothing?

After 30 years of watching credit cycles expand, distort, and collapse, I’ve learned one reliable rule:

“When enough people start drawing comparisons to 2008, it’s worth stopping to check whether the analogy holds up — or whether fear is doing the analytical work for them.”

Right now, judging by the amount of commentary on social media, the stress in the private credit market has everyone’s attention. Most of the commentary being generated makes the immediate jump from private credit firms “gating” exits to the onset of the next subprime crisis in the financial system. Those claims are certainly alarming and generate many clicks and views, but the question is whether those claims are based on facts rather than opinions.

Just recently, Goldman Sachs CEO David Solomon flagged the risk of private credit in his annual shareholder letter. Lloyd Blankfein, who piloted Goldman through the Global Financial Crisis, warned publicly that the financial system appears to be “inching toward another potential catastrophe.” Meanwhile, Goldman’s own research arm published a note concluding that private credit stress is “unlikely to generate large macroeconomic spillovers on its own.”

So which is it? A repeat of the subprime crisis of 2008, or a painful but contained credit cycle? The honest answer most likely sits somewhere in between, and understanding exactly where private credit differs from subprime tells you a great deal about how worried you should actually be.

Let’s revisit 2008.

What Made The Subprime Crisis So Catastrophic

It is hard to believe that we are rapidly approaching the 20-year anniversary of the “Great Financial Crisis” that nearly destroyed the financial system as we knew it. There are many investors and commentators in the markets today who only know about the event from reading history books. Having lived through it, it is a different reality.

Crucially, the 2008 subprime crisis wasn’t simply a mortgage problem. It was a leverage-and-derivatives problem that started in mortgages. That distinction matters enormously when you’re sizing up today’s private credit stress.

At the heart of the crisis was a product called the collateralized debt obligation, or CDO. Banks packaged pools of subprime mortgages into tranches, which were rated by agencies using flawed models. Those CDOs were then re-sliced into “CDO squared” structures, layering additional complexity and opacity on top of already opaque assets. The real acceleration came when synthetic CDOs entered the picture. Unlike cash CDOs, which required actual mortgages, synthetic CDOs referenced mortgages through credit default swaps. Journalist Gregory Zuckerman found that while roughly $1.2 trillion in subprime loans existed in 2006, synthetic structures created more than $5 trillion in exposure referencing those same loans. The CDS market alone reached a peak notional value of $62.2 trillion by year-end 2007. That is not a typo.

But the derivatives machine required raw material to function, and Wall Street’s insatiable hunger for collateral triggered what historians of the crisis now call the “race to the bottom” in mortgage underwriting. To keep the CDO assembly line running, originators needed volume. That demand for volume led to a collapse in underwriting standards. By 2006, no-money-down mortgages were commonplace.

- NINJA loans, “No Income, No Job, No Assets,” were extended to borrowers who could not remotely service the debt once introductory teaser rates reset.

- Stated-income loans, in which borrowers self-reported earnings with no verification, became the industry norm rather than the exception.

- Adjustable-rate mortgages were sold to buyers who qualified only at the teaser rate and had no capacity to absorb resets of 3 to 4 percentage points two years later.

The Mortgage Bankers Association later estimated that subprime originations reached $600 billion in 2006 alone, up from roughly $160 billion in 2001. Most importantly, the loans were designed to be sold, not held. In other words, the originator of the loan bore no long-term risk and had every incentive to close as many transactions as possible, regardless of quality.

That single misalignment of incentives was the original sin of the entire subprime crisis.

What compounded the damage beyond even that was systematic, institutionalized fraud at the origination and securitization level. The Financial Crisis Inquiry Commission documented widespread “robo-signing,” where bank employees executed thousands of mortgage documents per day without reviewing them. They affixed signatures and notarizations to paperwork they had never read. Countrywide Financial, Washington Mutual, and others were found to have misrepresented loan quality in the representations and warranties they made to investors purchasing MBS tranches, fraudulently inflating the apparent collateral quality of the pools they sold.

Appraisers faced pressure, and in many cases direct financial incentive, to hit predetermined valuations that supported loan amounts the underlying properties could never justify. The FBI reported that mortgage fraud suspicious activity reports increased by more than 1,400% between 2000 and 2007. When losses eventually surfaced, investors discovered they had purchased securities backed not just by bad loans, but by fraudulently documented ones. That distinction made recovery values nearly impossible to model and turned settlement litigation into an industry unto itself for a decade afterward. JPMorgan alone paid $13 billion in 2013 to resolve government claims over mortgage securities, and that figure represented only a fraction of industry-wide settlements.

When housing prices began falling, that entire structure detonated in both directions simultaneously. Banks that held CDO tranches faced mark-to-market losses. Banks that sold CDS protection, AIG being the most famous, faced collateral calls they couldn’t meet. Here is the most crucial point. These instruments traded freely in liquid markets, so price discovery occurred in real time, compressing the panic into a matter of weeks. The interconnection was total. Twelve of the thirteen largest U.S. financial institutions were at risk of failure, according to then-Fed Chair Ben Bernanke.

That’s what systemic risk actually looks like.

Private Credit Stress Is A Different Animal

The private credit market now stands at roughly $1.7 to $2 trillion in deployed capital, a figure that has grown rapidly since banks retreated from middle-market lending after the Global Financial Crisis. That growth is precisely what generated the current stress. Redemption requests have surged across major platforms. Blackstone’s BCRED fund saw record redemptions of $3.8 billion in Q1 2026, exceeding its 5% quarterly buyback limit. Apollo, Blue Owl, and Morgan Stanley’s North Haven fund have all imposed withdrawal restrictions. That gating of withdrawals led to an obvious decline in inflows across retail private credit funds. Those inflows fell to roughly half their 2025 pace, according to Goldman Sachs estimates.

So far, the catalyst is concentrated in software companies, which represent an estimated 15% to 25% of many private credit portfolios. They are under pressure as AI disruption fears potentially erode their earnings power and their ability to service debt. The headline default rate sits around 2% as of 2025, but Goldman Sachs Asset Management’s own research acknowledges that figure understates the true level of stress. When you include liability management exercises and distressed exchanges, the real rate approaches 4% to 5%. That’s meaningful deterioration. It’s not catastrophic, but it’s real.

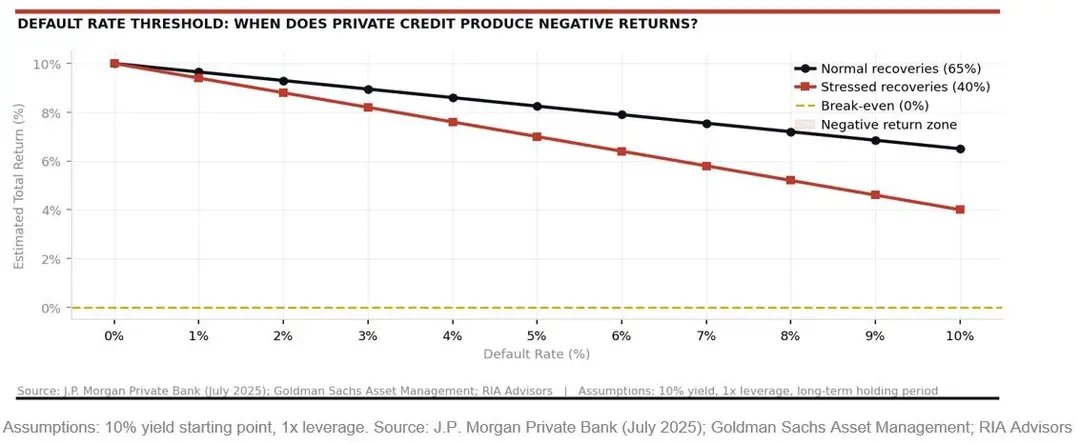

J.P. Morgan’s analysis showed that for senior direct lending to produce negative total returns, default rates would need to exceed 6% while recovery rates would collapse below 40% simultaneously. Those numbers have historically appeared only during COVID and the Global Financial Crisis itself. That’s a high bar — but it’s not an impossible one. However, that would require a deterioration in macroeconomic conditions, a continuation of the Iran conflict oil shocks, and a contraction of consumer spending, which could certainly amplify risks. As shown below, the current structural comparison between the subprime crisis and the private credit sector today is markedly different.

The Importance of the Gating System

The most structurally significant difference between 2008 and today is also the one that generates the most debate. Unlike the subprime crisis, private credit funds can gate their exits. When Blackstone caps BCRED redemptions at 5% per quarter, it’s not a failure of the fund; it’s the mechanism working as designed. In 2008, there was no such circuit breaker. MBS and CDOs traded continuously in secondary markets, meaning every forced seller found a bid at a lower price, triggering more mark-to-market losses, which in turn triggered more forced selling. The feedback loop was instantaneous and brutal.

Gating slows that process considerably. LPL Research noted that while gating makes for terrible headlines, it prevents the forced liquidation that accelerated subprime losses. Goldman Sachs estimates that retail private credit inflows will remain in net outflow throughout 2026 and likely into 2027, a slow bleed, not a cliff. That’s a very different contagion profile.

That said, gating is not a cure. It transfers the problem in time, not away from investors. Those sitting in redemption queues face a multi-year wait to exit positions that may continue to deteriorate. The opacity of private credit portfolios and manager-reported valuations means stress can accumulate invisibly until it can’t.

“The key risk in private credit is not what is visible, but what remains hidden.” – The Daily Economy

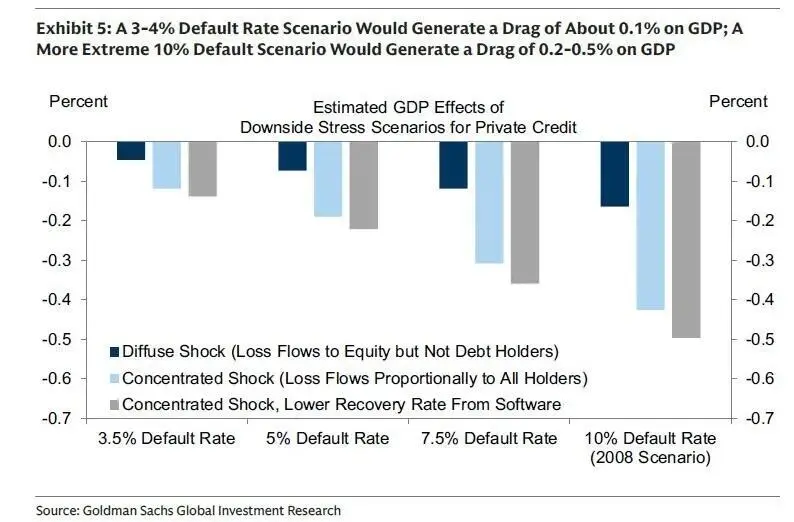

Goldman Sachs economist Manuel Abecasis concluded that, even in an adverse scenario, private credit stress would only drag on GDP by 0.2% to 0.5%. His reasoning is straightforward: the private credit sector holds about $1.7 trillion in levered loans, or roughly 4% of all credit to the private non-financial sector. That’s is not nothing, but it’s not the $62 trillion CDS market either. Goldman also notes that bank lending to businesses has actually accelerated recently, providing a partial offset if private credit tightens.

Blankfein’s view carries different weight precisely because he’s been through the real thing. He warned that private credit assets “can be hard to analyze, may feature hidden leverage, and can become tough to sell.” He’s right that opacity and illiquidity create conditions where problems compound before they surface. The question is whether those conditions, combined with a still-manageable scale, produce systemic contagion or simply painful losses for a subset of investors.

“Private credit stress is unlikely to generate large macroeconomic spillovers on its own.” — Goldman Sachs Economist Manuel Abecasis, March 2026

I’m inclined to side with Goldman’s macro conclusion. However, with a caveat that matters. The base case holds only so long as private credit problems don’t compound with a broader recession, a sustained oil shock from the Iran conflict, and a sharper-than-expected deterioration in software company cash flows. Any two of those three conditions occurring simultaneously change the calculus. Goldman’s own research acknowledges this. The bigger risk isn’t private credit alone. It’s private credit stress coinciding with the wider tightening of financial conditions.

What Investors Should Pay Attention To

The structural differences between today and the subprime crisis are real and important. There’s no synthetic subprime CDO chain multiplying private credit losses to a $5 trillion notional exposure. Most critically, the investor base is primarily institutional, not retail money market funds holding fraudulently rated paper. Fund-level leverage is modest, and the gating mechanism, whatever its imperfections, prevents the instantaneous price cascade that made the subprime crisis so destructive.

What this most closely resembles is a normal credit cycle playing out in an untested asset class. Not a systemic collapse, but not a benign correction either. Goldman Sachs Asset Management’s own European research found that “stress events are likely to remain elevated relative to the last decade,” concentrated in smaller companies and cyclical sectors. That pattern will probably hold in the U.S. as well.

Three things would change my view and warrant genuine alarm.

- First, if default rates push past 8% in tech-heavy private credit portfolios as AI disruption accelerates.

- Second, if bank credit facilities to private credit managers get pulled at scale, triggering forced asset sales.

- Third, retail penetration of private credit grows, as institutional investors sell, leaving less-sophisticated money to hold the bag.

None of those conditions is inevitable. All of them are possible.

The subprime crisis analogy fails on the specifics. But the lesson from the subprime crisis isn’t about CDOs. It’s about what happens when credit markets expand rapidly, underwriting discipline erodes under competitive pressure, and opacity masks deteriorating loan quality. On those broader conditions, the warning is more relevant than the Goldman bulls would like to admit.

That is why we continue to underweight risk for now until we have better clarity about the future.

Key Catalysts Next Week

This is the most structurally loaded week of the quarter. The calendar stacks a Q1 close, a Q2 open, and a full employment gauntlet into five sessions, with markets still metabolizing whatever the Fed just delivered..

Tuesday is the pivot. Consumer Confidence is the marquee release, and it’s the first full-month reading that captures the Iran conflict, the tariff widening, and February’s payroll shock in a single survey. The prior print of 91.2 was already soft. The Expectations component, which the Conference Board flags as a recession signal below 80, is the number to watch. A sharp drop would validate the stagflation fears the Fed just tried to navigate around. Chicago PMI and Case-Shiller Home Prices round out the morning, and then Q1 closes at the bell. Expect elevated volume as pension funds and mutual funds finalize window dressing and mark final positions, totaling roughly $62 billion on the buy side.

Wednesday flips the calendar to Q2 and immediately delivers a triple shot: ADP private payrolls, ISM Manufacturing, and JOLTS. After February’s -92,000 NFP shock, the ADP print will either stabilize the labor narrative or accelerate the deterioration thesis. ISM Manufacturing is the tariff passthrough read, the Prices Paid subindex will tell us whether producers are eating costs or passing them through, while New Orders reveal whether demand is contracting under policy uncertainty. JOLTS completes the picture with the openings-to-unemployed ratio that the Fed uses to assess labor market slack.

Friday is the week’s anchor: March Nonfarm Payrolls. February was distorted by a Kaiser Permanente strike and severe weather, giving bulls a one-month excuse. If March payrolls bounce back above 100,000, the “transitory weakness” camp wins. If they print flat or negative again, the labor market deterioration becomes undeniable, and the pressure on the Fed to act, despite sticky inflation, becomes immense. ISM Services PMI that morning adds the services-sector inflation read alongside Wednesday’s manufacturing data.

zerohedge.com/markets/subpri…

English

@phurstclass @redpillb0t That's your psychosis talking.

Do think Trump placed the guy that priced these parts? Or is it possible the rip off scam was always there?

English

@redpillb0t When you have a President who is totally corrupt do not be surprised if oligarchs and their companies gleefully follow him and are as corrupt as he is.

English

Home Depot must have been closed that day…

The US Air Force pays $90,000 for a bag of bushings that normally cost under $100

Our tax-dollars flushed down the drain.

English

@MC_Fox97 @John69149375 @GigglingGanon That sums it up. He told Linda she was going to get-it, and what did she go and do?

Well, she got-it. And she went and got two other people killed because of her not taking warning.

I vote not guilty.

(Satire)

English

@John69149375 @GigglingGanon Just because he has a breaking point, doesn't make him weak. Literally everyone has a breaking point. You aren't invincible

English

If fed up were ever a person this is them.

This guy recounts his actions to the police on his wife and his mother and father in law.

He takes full responsibility for his actions that he in detail breaks down for the authorities. Basically he snapped. 👀

English

@LevineJonathan @EmmaJoNYC Everything's an act with them.

Reminds of the time they sent Tim Waltz on a bird hunt with a camera crew. It was clear he'd never handled a shotgun before, and who the hell goes hunting with a camera crew? 😒

English

I can't imagine having to think this way

Obama was black and won in 2008 and NOBODY on the right calls him a DEI president because we all saw how Hillary and Co. threw EVERYTHING at him — no "his turn" or "glass ceiling" BS for him

You put everyone through the same wringer and whoever wins should be the nominee — done

English

@JohnnyAGI The first non violent event ever. That Being the case, we must conclude the Antifa chapters were not given contracts. No pay, no play

English

I am so confused.

How in the world did "the violent left" assemble 8 million people in over 3,000 locations across the country without a single incident of violence?

No one even assaulted a police officer

I was told the left were violent and hated America. What gives? 🤯

English

@PollTracker2024 You don't have to reregister to vote unless you change address

English

Axios: More than 5 million voting-age Americans would have to drive an estimated hour or more to present their citizenship documents to register to vote, as would be required under the Safeguard American Voter Eligibility (SAVE) Act.

axios.com/2026/03/29/sav…

English

It seems like some Republicans are going to go down if the SAVE Act passes

Gunther Eagleman™@GuntherEagleman

🚨 Rep. Tim Burchett just WENT OFF on Senate Republicans “They need to get some new leadership over there, in my opinion!” Translation: Fire John Thune NOW! The RINOs have been weak, spineless, and useless for too long. REMOVE JOHN THUNE!

English

@wayotworld Black African Americans and migrants are in a civil war with white people across the world. This was all planned by the elites and fake news.

English

No. This is what mass formation psychosis looks like

WeThePeople🇺🇸🇺🇸@PrincessBravato

This is what democracy looks like. #NoKingsMarch

English

@swingsandmises @thedarkhorsepod I think it came from advancement of the critical studies. It always is about finding some injustice in literally everything.

English

That's literally not the essence of woke, this isn't a matter of opinion. "Woke" and "cancel culture" went hand in hand for many years, but what you're describing isn't woke. Woke is quite literally about "waking up" to certain perceived realities (like the woke right seem to think they have in recent months), it has nothing to do with cancellation, that was simply one of the tactics they utilized.

English

Bret Weinstein explains, "the essence of woke is cancellation."

"...There's banish, we're not gonna platform you because you've lost your mind and there's coercion. We're gonna get you back on board with the consensus. And those two things are basically a choice. Either you get back on board with the consensus or you're out."

From DarkHorse Episode 318.

English

@PrincessBravato The dems looted Ukraine according to declassified documents released today. They are a party complrtly propped up by fraud

English

A republican did that ,not dems. Why are you blaming dems? They want agents paid right now.

Acyn@Acyn

Johnson: And it is unconscionable to me that the Democrats would force some sort of negotiation at 3AM and go home for their holiday and think that we're going to go along with that. So we're going to do something different. We're going to do the responsible thing. Republicans are going to continue to govern.

English

What protection promise was made 2-3 centuries ago?

AUF1@AUF1TV

💥Dr. Gerd Reuther zerlegt heute 300 Jahre Impfgeschichte Kein einziges Schutzversprechen durch Impfungen wurde in drei Jahrhunderten eingehalten. Zu diesem Fazit kommt der ehemalige Chefarzt Dr. Gerd Reuther in der neuen Sendung von „Elsa AUF1“. Ein Gespräch, das polarisiert, sagt Elsa Mittmannsgruber und fügt hinzu: „Aber genau deshalb muss es geführt werden.“ 📺 Die ganze Sendung von „Elsa AUF1“ mit Dr. Gerd Reuther sehen Sie noch heute Abend bei auf1.tv. Nicht verpassen!

English

mgb retweeté

💥Dr. Gerd Reuther zerlegt heute 300 Jahre Impfgeschichte

Kein einziges Schutzversprechen durch Impfungen wurde in drei Jahrhunderten eingehalten. Zu diesem Fazit kommt der ehemalige Chefarzt Dr. Gerd Reuther in der neuen Sendung von „Elsa AUF1“. Ein Gespräch, das polarisiert, sagt Elsa Mittmannsgruber und fügt hinzu: „Aber genau deshalb muss es geführt werden.“

📺 Die ganze Sendung von „Elsa AUF1“ mit Dr. Gerd Reuther sehen Sie noch heute Abend bei auf1.tv. Nicht verpassen!

Deutsch

@poapoa62247176 @SharrellAnne2 @EdKrassen Disobeying orders is not treason by definition. But gaslighting troops to disobey is aiding the enemy- that's the definition of treason

English

@MyrtleBeachWeek @SharrellAnne2 @EdKrassen Disobeying military order generally not treason but insubordination or disobedience under UCMJ! Service member obligated to refuse illegal or unethical orders such as those targeting civilian infrastructure!ICC issued warrants for widespread strikes on electricity infrastructure!

English

Dear U.S. military personnel.

Bombing Iranian power plants would almost certainly constitute a war crime.

If Trump asks you to do it, call a lawyer.

Do NOT obey his illegal orders!

English