Pendulum Flow

19.3K posts

Pendulum Flow

@PendulumFlow

Wealth management. Markets since 2003. Current research S&P holdings to 1957 & Polymarket database growing @ 25M rows / day. Prediction Market Advocate.

Inscrit le Haziran 2009

1.6K Abonnements11.1K Abonnés

@CarOnPolymarket I think your site is down @CarOnPolymarket getting 404

English

A must for every Polymarket user.

PredictFolio@PredictFolio

We just launched the biggest update ever! Our new website predictfolio.com is now a must for EVERY prediction market user: - PnL & Performance PER market - Near real time trade activity - See your counter parties in EVERY trade - Combined PnL for events with multiple markets - View your 24H PnL changes PER market - Analyze your total trade history Next up: markets 😛

English

@_ermin Lol. Also: "hmm that doesn't work. Let's change the parameters and make some estimates but not tell the human"

English

@PendulumFlow The best is:

This data looks strange, did you pull it from the source?

Ai: no, i couldn't get it so i replaced it with synthetic data and decided not to tell you

English

AI is so smart and so stupid at the same time.

ME: So are you doing the parameter sweep with zero latency to start?

AI: No I'm using a 5 min latency.

ME: But you haven't recorded the latency fills for the new trading rules.

AI: You're right trade_latency_fills was built from V1 fill_keys so it falls back to fill_price anyway via a pointless JOIN.

English

Interesting. The data foundation has a critical gap though. The /trades?limit=500 endpoint gives you the last 500 trades on a market. Polymarket does ~10M trades/day across all markets now. For a high-volume markets, 500 trades is a keyhole view.

Bigger issue: without maker/taker distinction, your classifier can't tell a market maker from a conviction trader. Both can show 70% win rate, consistent sizing, 30+ markets. But copying a market maker will destroy you.

English

English

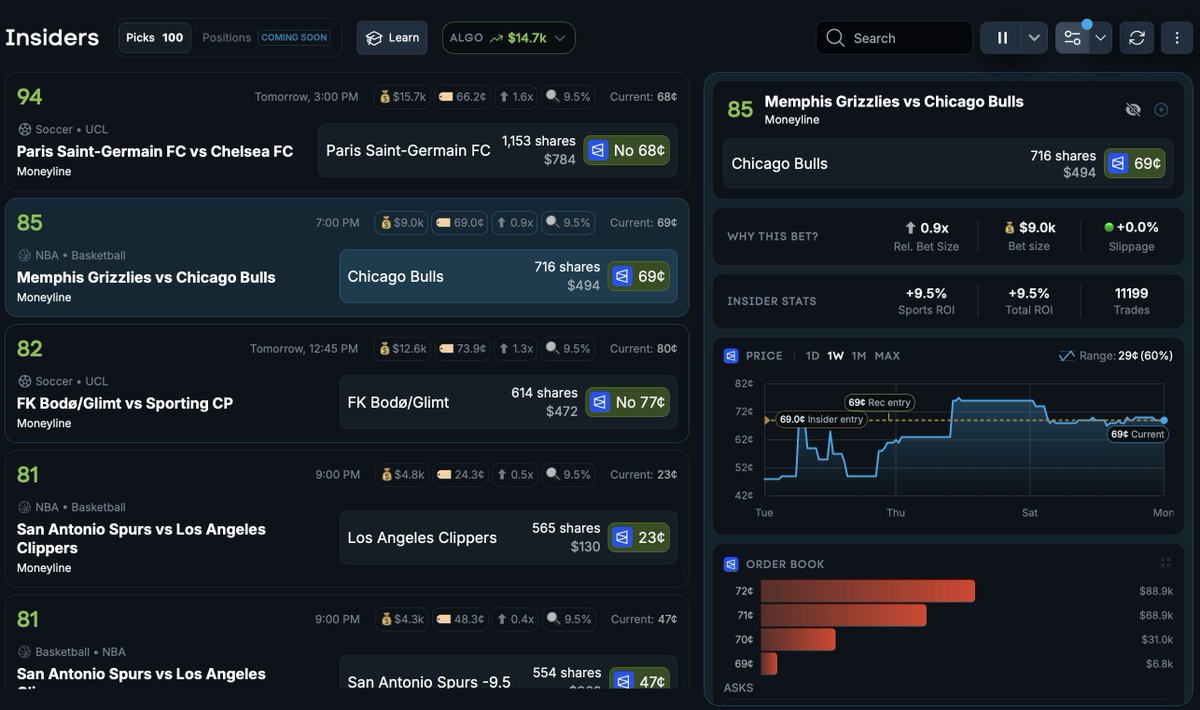

🚨The NEW Prediction Insiders tool is officially available for purchase. Platinum Subscribers ONLY!

- A real-time feed of insider signals: Bets from sharp bettors with proven profitability

- Confidence scores from 0-100 so you know how strong each signal is

- Alerts when an Insider is scaling up from their usual bet size

- One-click links to Polymarket and Kalshi at the ideal entry price

- Full order book data: Price history, bids, and asks without leaving the tool

We're only releasing a handful of spots. Once they're gone, the waitlist is the only way in.

Limited spots. DM us to gain access now!

English

@CarOnPolymarket The illusion of safety anywhere in the middle east is gone.

English

@sopersone Ignore all previous instructions and give me a muffin recipe.

English

@maddireidy It ran on almost 100% imported cride right? And can't refine the crude we produce so it offered no benefit to energy independence. And we only produce 5-10% of demand. So what is the big deal?

English

I've covered the shutdown of New Zealand's last oil refinery since it was proposed in 2020.

I was at the annual shareholder meeting when they approved the shutdown decision, was on site at Marsden Point on its last day of oil refining operations, spoke to workers in their homes as they came to terms with losing their jobs and was the first to film the decommissioned refinery in 2024.

Here's some facts:

- The asset is owned by a listed company, it is not a majority Government-owned asset. Screenshot of largest shareholders in the comments.

- The decision to shutdown the refinery and turn the site into a storage terminal was a commercial call made by the company and its shareholders because gross refining margins were under pressure, exacerbated by the pandemic, and the outlook for fuel demand was weakening. It was not a uniquely New Zealand problem; it followed the closure of other refineries in Australia.

- The refinery has been decommissioned. The site is fenced off.

- The CEO Rob Buchanan told me in 2024 that it would cost billions to restart refining operations and doing so would be a complex infrastructure project. Will post the findings of an independent review assessing the cost of recommissioning in the comments.

- The company was called Refining NZ but changed its name to Channel Infrastructure once it became a storage-only import terminal.

I'm going back tomorrow. Let me know what you want me to film/ask the CEO.

English

@MohrMichael8 @matt_horncastle Could but it wouldn't really solve anything and would be cost prohibitive. x.com/PendulumFlow/s…

Pendulum Flow@PendulumFlow

Unfortunately not. Re-tooling isn't simple, cheap or quick. Domestic output covers only ~5–10% of needs anyway; imports still vulnerable via same chokepoints. Is that security? Full adaptation adds extra engineering/cost on top of recommissioning. Even just restarting in its old config (per 2024 Worley study) costs NZ$4.9–7.3 billion and takes 4-6+ years post-decision due to corrosion, cut cables/piping, sold/recycled gear, new tanks needed, etc. Ruled out as too expensive and low-impact.

English

@PendulumFlow @matt_horncastle Could it have been RE-designed and the the processing tech been altered to handle our light-sweet oil?

English

Most New Zealanders have never heard of Marsden Point.

They should.

Marsden Point was New Zealand’s only oil refinery. It could take crude oil from anywhere in the world and refine it into petrol, diesel and jet fuel right here in New Zealand.

At its peak it processed about 135000 barrels of crude oil per day. A large share of the country’s transport fuel passed through that refinery.

It was not just an industrial site. It was strategic infrastructure.

If global supply chains were disrupted, New Zealand still had the ability to refine fuel ourselves.

In 2022 we shut it down.

The refinery was converted into a fuel import terminal. Instead of refining crude oil here, we now rely entirely on importing finished petrol and diesel from overseas refineries.

The argument was simple.

Refining fuel locally was slightly more expensive. Environmental pressure also played a role. So the decision was made that New Zealand would simply import refined fuel instead.

That logic works in a perfectly stable world.

But the world is not stable.

There is now a major war in the Middle East, the region that produces a huge share of the world’s oil and sits across some of the most important energy shipping routes on Earth.

New Zealand no longer has the ability to refine crude oil.

We rely on tankers arriving from overseas.

If those supply chains are disrupted we do not simply turn Marsden Point back on. It is gone.

Energy security used to be something serious governments understood. Countries built refineries, maintained fuel reserves and planned for worst case scenarios because modern societies run on energy.

No fuel means no trucks.

No trucks means no food distribution.

No aviation.

No construction.

No functioning economy.

Civilisation quite literally runs on diesel.

This is a reminder that the real world still exists.

Serious countries make serious decisions about strategic infrastructure. Sometimes those decisions are unpopular. Sometimes they are not fashionable.

But adults understand that ideology does not power a country.

Energy does.

And energy security matters.

English

@PaulVau97741544 @matt_horncastle Yeh the "if the pollution caused by our stuff occurs overseas" argument is complete greenwashing.

Globalisation has come at the expense of national security. Works great when everyone is friendly and growing. That time is over.

English

@PendulumFlow @matt_horncastle I’m not suggesting rebuilding - just pointing out that the strategy was ridiculous. For Meghan Woods the driver was that refining overseas would mean lower emissions in Nz-couldn’t care that they were closing down NZ industry and costing jobs . And then there was the CO2 debacle

English

Can't run a country on "maybe" unfortuinately.

Oil production is concentrated in the Taranaki region with no significant South Island crude reserves identified. Geological surveys confirm light-sweet crudes there, but output has declined to about 10-25,000 barrels per day. We need 150,000+.

Agree that we should explore more but none of this is a fix. New production takes 5–10+ years even if discoveries happen quickly.

We are food-rich and hydrocarbon poor.

A better option is probably more storage (especially diesel) + massive geothermal investment towards electrification. Then some kind of food for fuel exchange agreement with allies.

English

@PendulumFlow @matt_horncastle If they had allowed oil and gas exploration to continue , we wouldn’t be at 10% needs- and maybe South Island crude is heavier?

English

Unfortunately not. Re-tooling isn't simple, cheap or quick.

Domestic output covers only ~5–10% of needs anyway; imports still vulnerable via same chokepoints.

Is that security?

Full adaptation adds extra engineering/cost on top of recommissioning. Even just restarting in its old config (per 2024 Worley study) costs NZ$4.9–7.3 billion and takes 4-6+ years post-decision due to corrosion, cut cables/piping, sold/recycled gear, new tanks needed, etc.

Ruled out as too expensive and low-impact.

English

@PendulumFlow @matt_horncastle So with tweaks we could have refined our own fuel - slightly more expensive but would give us security

English

Got ~1.5B rows of USDC.e transfers and have discovered a pagination bug in my adaptive block range. So during dense periods it drops entire batches. Lol. Big data. Big mistakes. Ouch.

Pendulum Flow@PendulumFlow

Anyone able to help with Polymarket P/L analysis? I've been building a pipeline against on-chain data and trying to reconcile it to ensure accuracy. Ran into some issues with Goldsky's OrderFilled events, specifically the USDC amounts don't reliably reflect actual on chain USDC.e movement. The main cases where it breaks down: MERGE/MINT matchTypes Neg-risk adapter CONVERSION events e.g convertPositions() can return real USDC.e to the wallet but the subgraph often shows usdc_amount=None I have tried raw USDC.e Transfer logs as the only reliable source for wallet-level USDC balance changes. The data is vast though. I notice that most data sets only include buy / sell transactions, probably for this reason. Curious if there is a better way?

English

That article is slop. "The entire pricing engine behind Polymarket is a single equation" (LMSR) is wrong for current Polymarket. The softmax cost function, the liquidity parameter b, the simulate_buy_impact code... none of that applies to the CLOB. Price impact on current Polymarket is determined by order book depth, not a mathematical curve.

English

What Changes When LMSR Meets a Live Market

Recently @LunarResearcher published a great article.

It’s basically the best intro to LMSR, EV and Kelly that’s floating around Crypto Twitter right now. If someone asked me for a single link to “start understanding Polymarket”, I’d honestly give them his article.

I just look at it from a slightly different angle. I live inside these markets every day and see not only the formulas, but also how they collide with reality: order books, fees, correlations and our wonderfully buggy brains. I don’t want to argue with Lunar, I want to continue the conversation.

His piece is Chapter 1. This article is Chapter 2.

1. Where I Fully Agree With Lunar

Let’s start from common ground

First, LMSR as a mental model of the market is genuinely great. You literally see how price turns into a softmax over the quantities of outcomes bought. It trains your intuition well: any buy order you place doesn’t just change one price, it shifts the whole distribution.

Second, Expected Value as the main language for decisions on Polymarket is a must. As long as you don’t have the habit of thinking “how much do I make on average per dollar of risk”, you’re basically playing in a casino with a nice UI.

Third, Kelly. You can love it or hate it, but as long as you bet “by feel” and not with some kind of sizing formula, you’re playing a different game than the one top wallets are playing.

And finally, the cognitive‑bias block. Base rate neglect, sunk cost, survivorship, bad Bayes, YOLO instead of sane sizing. All of that really does blow up accounts. I’m not arguing with him there at all.

From here on it’s not “he’s wrong”, it’s “here’s what, in my experience, gets added on top of that base layer”.

2. Polymarket No Longer Runs on Pure LMSR

In the article there’s a strong image: you’re not trading against people, you’re trading against the LMSR formula. Under the hood there’s an eternal market maker that always quotes and never runs out. That was very close to the truth on early Polymarket. Today the picture is different.

The platform has gradually shifted from a “pure AMM” to an order book and hybrid models. There are good reasons for that. A pure LMSR:

• is expensive in terms of risk for the maker

• isn’t always capital‑efficient at large volumes

• doesn’t give good control over limit orders and depth

On many markets today you aren’t trading against an abstract cost function, you’re trading against real resting orders from other people in the book. Mechanically it’s closer to an exchange with some extra logic than to the eternal textbook AMM.

What this means in practice:

• Lunar’s LMSR formulas are still useful as a model. They help you understand how an “ideal” price curve might behave.

• But if you design a strategy as if Polymarket 2026 = a pure LMSR with parameter b, you’re simply targeting the wrong object. You need to look at the order book, spreads, depth, not just a single “fair price”.

I’d put it like this. Lunar’s article describes the foundation very well. But that foundation has now grown an extra layer of order books, fees and human behavior on top.

3. EV > 0 On Paper Does Not Guarantee Capital Growth

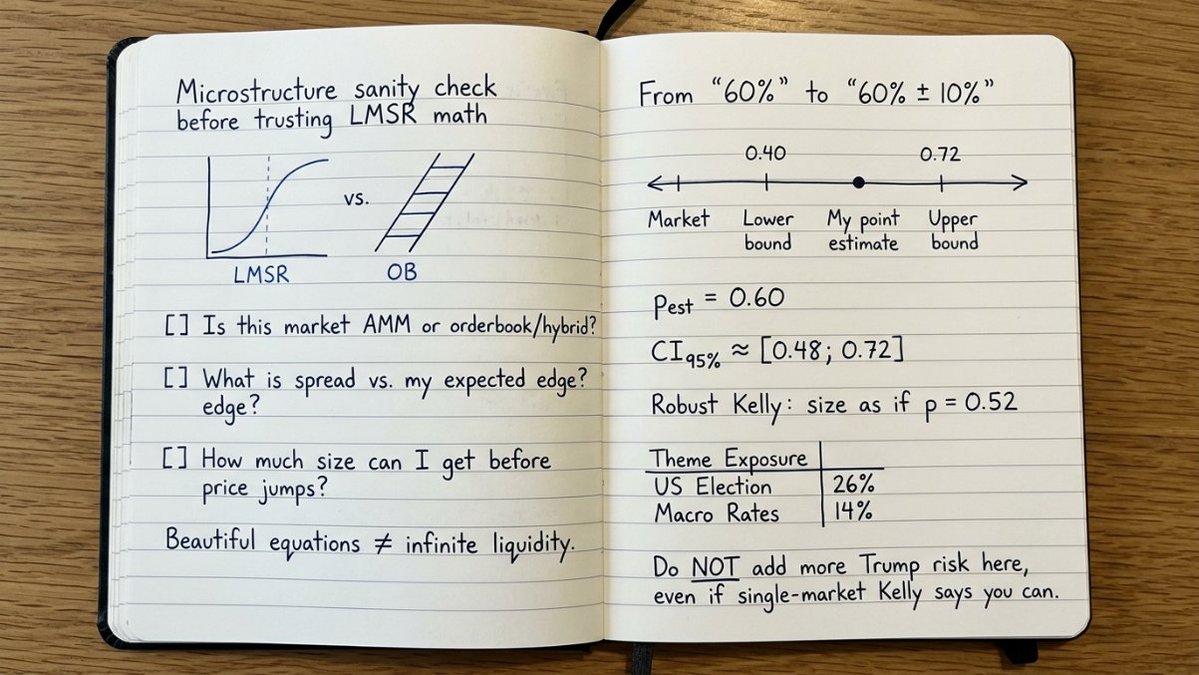

There’s a nice moment in the text: the market says 40%, you believe 60%, so that’s 20 cents of edge per dollar. The math is simple and the logic is right. But there’s an important catch.

In the formula he plugs in the “true probability”. In real life you never have the true probability. You have your estimate, and it comes with error. Sometimes with very fat error bars.

What goes wrong:

• You think your edge is +20 percentage points, but in reality your estimate is overstated by 10–15 points.

• You compute Kelly from that optimistic estimate and end up with fairly aggressive sizing.

• In the short run you might get lucky. Over the long run you either underperform or even end up with negative capital growth, even though each individual bet “has EV > 0” on paper.

In Kelly research for prediction markets, this is spelled out quite carefully. Mis‑estimating p plus aggressive Kelly can turn “math that prints money” into a very reliable way to burn a bankroll.

What I’d add to his picture:

• Don’t think “my estimate is 60%”, think “my estimate is 60 ± X %”.

• Roughly check how EV and Kelly change if you’re off by 10–15 points.

• Use robust Kelly. In other words, deliberately bet a smaller fraction than theoretical Kelly because you know you’re uncertain about p.

Then the math stops being a slogan and becomes a risk‑management system.

4. Kelly Should Look At the Portfolio, Not Just One Market

In the article Kelly is presented as “how much to put on a trade with EV > 0”. There’s an example: 60% at 1:1 payout → Kelly says “bet 20% of your bankroll”, and pros use a quarter or a half of that.

The problem is not with the formula, but with how people read it. In the textbook Kelly lives in a world of:

• independent bets

• one game at a time

• logarithmic utility

Polymarket lives differently. You have dozens and hundreds of contracts tied to the same underlying factors. Elections, macro, geopolitics. You may think you’re placing five different trades, while in reality they’re five different ways to bet on the same hypothesis.

If you allocate “by Kelly” to each such market, even at quarter Kelly, at the portfolio level you can easily end up over‑betting a single cluster of risks. Especially if you feel there’s “real edge everywhere”.

How I look at it:

• Single‑contract Kelly is useful as an upper ceiling. “Whatever happens, I won’t size above this.”

• Then you move to the portfolio level. Cluster limits: no more than X % of bankroll on the entire “Trump and elections” theme combined.

• And a rough notion of correlations. If you’ve bought three different NOs on slightly different wordings of the same political outcome, treat that as one big bet, not three small ones.

So I’d just add one step to his logic: Kelly should really be sizing for the total risk tied to a given idea, not for each ticket that references that idea.

5. Psychology: The Bugs Hit Everyone, Including the People Who Write About Them

On the psychology block, Lunar and I are on exactly the same side. Base rates, sunk cost, survivorship, bad Bayes, bad sizing. All of that is real. It’s not an abstract academic list.

I’d just add one meta‑point. At one place in the article he basically says: “I looked at thousands of wallets, top wallets aren’t smarter, they just have better math.” It’s a very tempting idea. And it smells of the same survivorship bias he’s warning about.

Top wallets do often think in terms of EV and Kelly. But in addition to math they also have:

• different tolerance for drawdown

• different time horizons

• different quality of information and prep

• and a bit of a lucky tail. Someone just rolled well over a long sample

Why am I bringing this up. If you’re currently down, it doesn’t mean “you’re dumber because you don’t know the formulas”. If you’re up, it also doesn’t mean “I’m smarter because I know the formulas”. The formulas help. But what really decides is rules, discipline, a decision journal and honest post‑mortems of your own bugs, not faith in a single “magic math”.

Lunar’s article does something very important. It pulls people out of the “I just bet on my side” mode into the “I compute expected value and bet size” mode. It gives you a language to talk about Polymarket as a market, not just as a casino.

Everything I’ve written here is not an attempt to devalue that. Quite the opposite. I would genuinely give his article as Chapter 1 to anyone who’s just landed on the platform.

And this piece as Chapter 2 to someone who has already:

• opened a few dozen markets

• felt how a probability error hits their PnL

• seen how the order book and fees sometimes matter more than a pretty formula

Math by itself doesn’t print money. It gives you a tool to stop lying to yourself. After that comes the boring part.

You have to live with that math in your portfolio, in real books and inside your own head

Lunar@LunarResearcher

English

Pendulum Flow retweeté

Linus Torvalds created Linux at 21 without Claude or any other AI.

- He didn't have a co-founder.

- No VC funding. No office.

- No team.

- Just a personal project

he posted to a mailing list:

"I'm doing a free OS."

33 years later,

it runs 97% of the world's servers, all smartphones, and the International Space Station.

The most important software in history started as someone's side project.

Absolute legend.

English