On parle à la TV de 60000 morts en 48h en Iran à la suite de la répression, ca fait 1250 mort/h.

Y a forcement des photos satellites des charniers, creusement des tombes ? Morgues etc etc ? Merci de poster vos sources.

@GlobalCollapse If the SEC determines there were material TOS violations that AppLovin failed to disclose to investors, this will become a securities fraud case rather than just a data privacy matter.

Pretty dismissive tone on your side though, no idea why.

Applovin' $APP

1) Primary biz mobile adtech w 84% margins & still restrict clients.

2) Expanding to mobie web, international, and opening enrollment.

3) Using AI to create ads for clients, both as a service and to increase rev from #1

4) Expanding to social media to boost #1

@mikeaxolotl CEO Scott Lang explained for last earning call that they will release after the approval (that happened on 18th) the implications of the 5/5 approval. Guess they will revisit the whole pipeline value and gives more guidance.

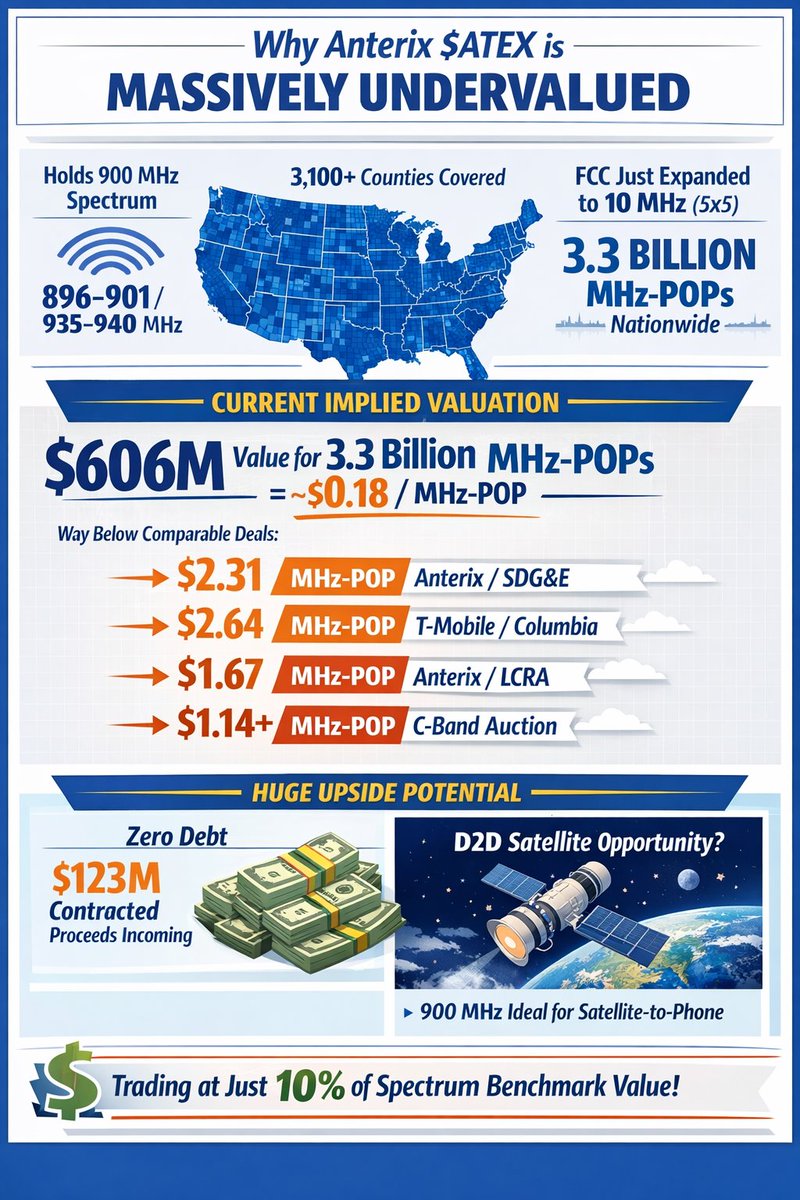

Started a position in $ATEX. I believe the market is being incredibly blind with this one, its insanely undervalued.

Anterix controls nationwide licensed 900 MHz spectrum (896–901 / 935–940 MHz) covering ~330M people, spectrum that aligns with 3GPP Band 8, one of the most widely supported low-band frequencies used by phones globally.

As many of the Space mob / $ASTS investors know,

this matters because lower band spectrum (<1 GHz) commands a premium due to:

• Superior range

• Better building penetration

• Lower infrastructure cost per coverage area

• Critical importance for nationwide and rural coverage

It is the most scarce and strategically valuable tier of spectrum.

On Feb 18, the Federal Communications Commission approved expansion from 6 MHz to 10 MHz nationwide (+67%).

The stock has barely reacted.

At current prices, the entire nationwide portfolio trades at just ~$0.18/MHz-POP.

Compare this to market transactions transactions:

Anterix’s own sales:

• $2.31/MHz-POP, sale to San Diego Gas & Electric

• $1.67/MHz-POP, sale to Lower Colorado River Authority

• $1.30/MHz-POP, sale to Evergy

Other low-band / major spectrum comps:

• $2.64/MHz-POP, T-Mobile purchase from Columbia Capital (600 MHz)

• $2.21/MHz-POP, T-Mobile purchase from Comcast (600 MHz)

• ~$1.67/MHz-POP, utility spectrum acquisition by Grain Management (800 MHz)

Even higher-frequency spectrum, which is inherently less valuable, cleared at:

• $0.86/MHz-POP, 600 MHz auction

• $0.68–$0.74/MHz-POP, 3.45 GHz auction

• $1.14–$1.29/MHz-POP, C-Band auction

Yet $ATEX sits at $0.18/MHz-POP.

They also have a healthy looking balance sheet:

• Zero debt

• $123M+ contracted proceeds incoming

• Active strategic review

Optional upside:

FirstNet is currently working with the FCC to modify its terrestrial spectrum to enable satellite connectivity via AST SpaceMobile.

This establishes a precedent.

If similar waivers or rule expansions occur, Anterix’s nationwide single owner low-band spectrum could become one of the most strategic assets in telecom.

Liquidity also remains limited. With relatively low daily volume, it’s difficult for institutions to build large positions without moving the stock, which helps explain why the valuation gap can persist.

Even assigning zero value to satellite optionality, the spectrum alone appears dramatically undervalued based on confirmed private market comps.

Scarce low band spectrum.

Trading at a fraction of market value, this is an easy 3-4x without any strategic interest or speculation.

NFA*

@dallas_dia61451@RobEducated 60% capacity increase, fair value still 3x from there.

Need some deals to assess properly Mhpop value.

Business is fully derisk in case M&A still on the cards

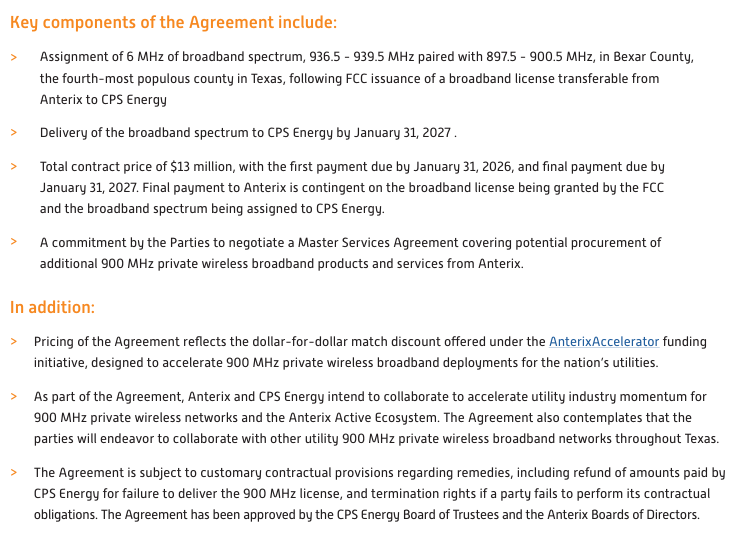

First $ATEX deal in a long time. $13m deal, but good spectrum valuation benchmark.

Worth noting this is a municipal utility and only covers a small portion of the total potential addressable area for them.

FRMI

Listed REIT-style “AI power grid” play (co-founded by Rick Perry), building Project Matador / HyperGrid, an 11 GW private power + AI campus in Texas.

1GW ambition: they explicitly guide to ~1 GW online by end-2026, ramping toward 11 GW of generation for AI data centers (nuclear + gas + solar + storage).

“First-mover advantage”: their SEC filings talk a lot about establishing first-mover advantage in nuclear power development for AI/hyperscalers and building what could become one of the largest nuclear power complexes for compute.

Tenant / hyperscaler angle: as of the latest public docs, they:

- Have an Advance in Aid of Construction agreement (USD 150M) with a first prospective client, very likely an AI/hyperscale-type tenant.

- Are in talks / LOIs with “many hyperscalers,” but have not yet disclosed a fully binding long-term lease publicly.

While I love the miner to HPC/ai transition names like $WULF $CIFR $IREN, I do believe the easy money has been made. I think it’s more likely we see 1-2x returns rather than 3-5x for these names in 2026. In the coming days (after I complete my position) I will be sharing a company ticker that will be part of the next iteration of this AI and power trade. I do believe they will be 3-5x this time next year. It’s a name nobody ever mentions, has a contract with a hyperscaler with first mover advantage and ambitions to deliver 1 GW of power. I can’t wait to share but in the meantime, feel free to drop some guesses but please no penny stocks.

I’m not sure I buy the “OpenAI will structurally erode Google’s ad business” thesis. Like it feels like a surface view with no real deep dive.

Google is still a ~$70B FCF machine growing ~5% YoY. OpenAI, even at ~$13B revenue run-rate, has massive COGS and is nowhere near free cash flow break-even. Microsoft absorbing infra cost doesn’t change OpenAI’s economic reality if anything it highlights the lack of scalability on the cost side to me.

Product-wise, Sundar explained during earnings the exponential trajectory of tokens consumed by their end-products and this is accelerating with Gemini Nano + Veo. Google is scaling inference and integrating it deeply into Search, Workspace, and Android. Gemini Ultra is ~$150/year, so Google already reconstructed a revenue line comparable to OpenAI’s subscriptions, but with far healthier margins. Need to see how both lines compare over time.

On the engineering side, Gemini Code Assist in VS Code is now good enough that I’ve shifted most of my coding from Codex to Gemini, but I still honestly use Claude a lot. Gemini chat is also noticeably faster than ChatGPT. And Google’s photo/video stack (Veo, Imagen) is miles ahead to me, i dont see any sora edits on my twitter timeline whereas veo and nano edits are everywhere.

Financially, Google can take on debt, issue equity, scale infra, and still print cash. OpenAI can’t. Its equity is already heavily diluted, its credit capacity is extremely limited, and the business model is far from mature.

So I don’t really see how OpenAI is supposed to aggressively damage Google’s ads business unless you respectfully ignore how competitive Gemini has already become.

Among the 5 frontiers models (Gemini , Grok, ChatGPT, Claude and llama), 3 are part of positive fcf business, 2 are still startups. Pic changes if apple/amazon annonces massive merger or one of the mag7 comes out with a better ai product than current LLMs.

I have been surprised by the resiliency in Google's ad business given ChatGPT is at 800M WAU

Yes, some of it is that ChatGPT is serving new use cases/workflows that weren't going to monetize via traditional Google ads, but I am not convinced by this theory. Anecdotally, me and people I know no longer start the information search process on Google at all. This is true for probably at least 10M affluent white collar workers who must have comprised a meaningful percent of Google's revenue given their high spend

My suspicion is that the cracks will begin to show in Google's business when OAI rolls out a real ad program.

Basically, my theory is that the problem is not the demand side, but the supply side. ChatGPT is eroding Google's demand growth, but the supply doesn't have anywhere to go

Once OAI rolls out a robust self-serve ad program, advertisers will re-allocate some amount of their budget away from Google to OAI, and this will become visible in Google's financials

Thoughts?

@laurashin@CryptoHayes I think people who didnot follow the bankruptcy are full of strong opinions but clueless about actual facts.

Time to talk with creditors properly…

THIS ^^^ SBF’s entire defense has rested on non-crypto people (including Michael Lewis) not knowing the difference between a fractional reserve bank and a crypto exchange.

If I’d done a pod with SBF after the fall of FTX, my first question for him was going to be, “Describe the cold storage setup at FTX.”

Are bankruptcy lawyers dodgy? Fuck yeah.

But y were u even in that situation? Bc you ran an exchange that couldnt meet customer withdrawals on demand. If FTX was a bank, ur criticism would be valid. Are you saying FTX was a bank or an exchange?

$WULF The company has quietly updated their guidance on Cayuga with 50 MW planned for delivery late 2026. They like to announce 12 months ahead of delivery so it is likely we hear about a third customer in Q4.

I did that back in Mid August if that helps

October 2024 Convertible Notes Offering (2.75% Notes due 2030)

Form 8-K Filed: October 24-25, 2024

Key Terms:

- Principal Amount: $500 million total (originally $350 million, upsized to $425 million, then $500 million with greenshoe)

- Interest Rate: 2.75% per annum, payable semi-annually on May 1 and November 1

- Maturity Date: February 1, 2030

- Initial Conversion Price: $8.48 per share (32.5% premium to the $6.40 closing price on October 23, 2024)

- Conversion Rate: 117.9245 shares per $1,000 principal amount

Capped Call Transactions:

- Cost: $60 million (approximately $51 million initially, increased with greenshoe)

- Cap Price: $12.80 per share (100% premium to the $6.40 closing price)

- Counterparties: Certain financial institutions (initial purchasers or their affiliates)

- Purpose: Reduce potential dilution and/or offset cash payments upon conversion

Use of Proceeds:

- $60 million for capped call transactions

- $115 million for share repurchases (17.97 million shares at $6.40)

- Remainder for general corporate purposes and HPC infrastructure expansion

August 2025 Convertible Notes Offering (1.00% Notes due 2031)

Form 8-K Filed: August 18-19, 2025

Key Terms:

- Principal Amount: $850 million (originally $400 million, upsized with $60 million greenshoe option)

- Interest Rate: 1.00% per annum

- Maturity Date: 2031

- Initial Conversion Price: $12.43 per share (32.5% premium to $9.38 closing price on August 18, 2025)

- Conversion Rate: 80.4602 shares per $1,000 principal amount

Capped Call Transactions:

- Cap Price: $18.76 per share (100% premium to the $9.38 closing price)

- Purpose: Same anti-dilution protection as October 2024 offering

Key Features of Capped Call Transactions:

- Structure: Private, over-the-counter derivative transactions separate from the convertible notes

- Function: Effectively increases the conversion price from the company's perspective to the cap price

- Anti-dilution: Provides protection against dilution up to the cap price

- Settlement: Can be settled in cash or shares at TeraWulf's election

- Hedge Activity: Counterparties may engage in hedging activities that could affect stock price

Redemption Features:

- Cannot redeem before November 6, 2027 (for 2030 notes)

- After that date, can redeem if stock trades at 130% of conversion price for 20 of 30 trading days

- Convertible only upon certain conditions before the final months before maturity

ON THE INTERPRETATION

- $850M convertible notes issued at 1.00% interest, maturing 2031

- Two batches of capped calls with different strike levels creating complex flow dynamics

- Current stock price: $9.38 (August 18, 2025)

Capped Call Structure - BEARISH PRESSURE:

- Batch 1: Cap at $12.80 - Market makers will sell heavily as price approaches

- Batch 2: Cap at $18.76 - Massive selling pressure near this level

=> Selling intensity increases exponentially the closer stock gets to each cap level

Convertible Notes Structure - BULLISH PRESSURE:

- Batch 1: Conversion price $8.48 (already breached - hedge funds buying)

- Batch 2: Conversion price $12.43 - Major buying pressure expected here

=> Hedge funds must cover short hedges by buying stock at conversion levels

Critical Price Levels & Flow Dynamics:

- $9.38 → $12.43: Net bullish (HF buying dominates, no cap pressure yet)

- $12.43: Massive bullish catalyst as 2nd batch conversion triggers HF buying

- $12.43 → $12.80: Battle zone - HF buyers vs. market maker sellers (1st cap)

- Above $12.80: Bears take control with accelerating selling from capped call hedges

Would make sense approaching $12 to witness a decent take profit.

@skol_abides There is nothing interesting in subnet pools as they are used to fund opex/capex without any mechanism to return back any from of value to token holders.

This statement stands for 99% of the subnets.

Next time someone asks what’s working on Bittensor, point them here

Chutes, Targon, and Lium have all built real AI businesses

Collectively already doing $20M ARR after flipping the fee switch just ~3 months ago