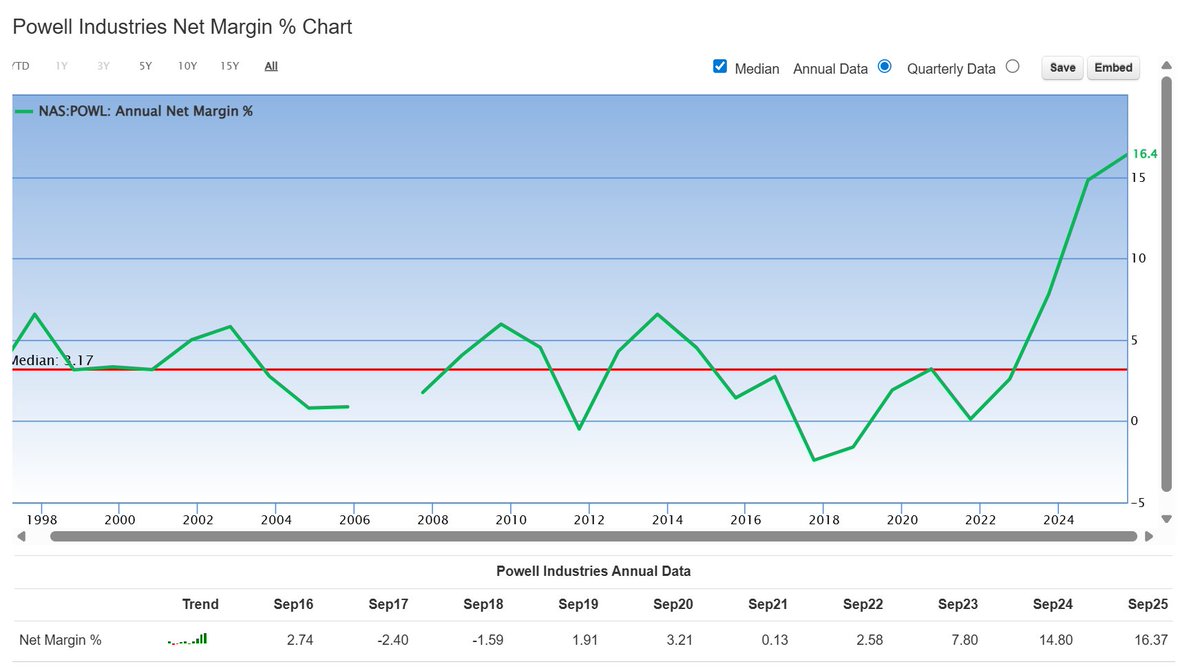

Narrow moat, revenue decelerating fast: : Q1’25 +9.2%, Q2’25 -0.7%, Q3’25 +8.3%, Q4’25 +4.0%.

Balance sheet is a fortress because the business needs it. Management carries that massive cash cushion specifically to survive the revenue troughs that have historically hit 40–50% peak-to-trough.

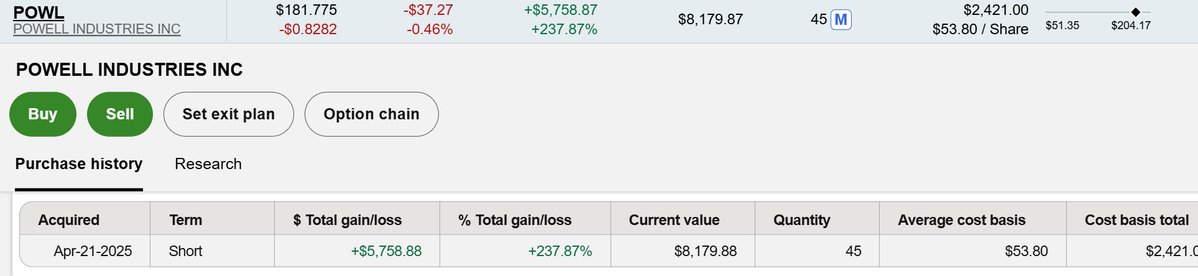

Revenue durability under stress won’t hold up well compared to $HUBB for example. $POWL is project based cyclical revenue. I would be interested in them at the right price but as of now I can deploy that cash elsewhere with more upside / different exposure.

Just not too keen on the business model doesn’t fit my portfolio style. Fortress cash, defensive with moat / monopoly.

English