Maxime 182

905 posts

This last few weeks have been incredibly hard, and I’m sure everyone here shares that.

It can also be very frustrating, I had buy back the $ADBE puts I sold yesterday only to watch the stock up 3% today. I gave up on shorting $PLTR only to see it down 25% since the start of the year.

But in all of this, it’s important not to get emotional and keep a level head, something much easier said than done…

Remember it’s ok to sell if it means you can get a chance to fight another day, and if you’re not sure whether to sell or not, ask yourself a simple question: would you buy today if you didn’t own any?

Lastly a little bit on what is going on: the same theme from last year of AI will make all software companies go away has really hit a new level, combined with the world is a really scary place right now.

But remember Mr. Market can be silly but also simple. So try to see where the baby is being swept away with the bath water.

We all know the story of $ADBE & $UBER but why is $SPOT down in this story? Things are bad with $PYPL but will that be the same for $XYZ?

Anyway, don’t mind me, just some silly kid thoughts.

Try to give everyone you love a big squeeze. 💜

English

@aleabitoreddit Are you still bullish on Reddit ? Don’t see any posts from your anymore ! Thanks

English

Yeah… I’m cooking super hard.

$AAOI +10.65%

People aren’t bullish enough after the new $LITE backlog report.

The demand visibility lasts past 2029 for optical companies…

Serenity@aleabitoreddit

I'm not sure people understand yet: $LITE backlog order fill into 2028 signals extreme demand. And a lack of capacity. Then by second order effect of hyperscaler demand spillover: Guess who is projected to have the largest 800G/1.6T capacity in America? $AAOI. They fab their own inp lasers, design their own transceivers, and assemble it. If $AAOI can execute on capacity ramp, that likely all translates into revenue due to everything being sold out. My $40B MC price target from $5B is starting to look more and more likely?

English

@aleabitoreddit Is Reddit the only larger cap you see asymmetric value at the moment ?

English

Well that was a fast 100%+ return with $IQE in 1 month.

Turns out when you map it to $LITE and the hyperscaler supply chain at the epiwafer level…

Markets start pricing it in with the new $LITE projections…

Serenity@aleabitoreddit

Was the first to talk about $AXTI in relation to photonics BOM/supply chains: $IQE is very interesting too as one of the only Western suppliers. Basically if you look at photonics flow on $GOOGL TPU/hyperscaler ASICs kinda looks like this (very likely, but undisclosed): Optical Transceivers (highest BOM): Lumentum/Cloud Light: ~ Vital / $AXTI-> $AXTI/Sumitomo/JX -> $IQE (Epi-Wafers) -> $LITE / Cloud Light -> $FN (Contract Manufacturing) -> $GOOGL TPU Merhcant optical supply chain: ~ Vital / $AXTI -> $AXTI / Sumitomo / JX -> → $LITE / $AVGO / $COHR (EML) + $MRVL / $MTSI / Semtech -> Innolight/Eoptolink -> $GOOGL So if you want moonshot-type photonics BOM / price-hikes stocks deeper upstream in the photonics BOM: $AXTI, $IQE and your way to go. $AXTI had terrible fundamentals before but the recent Northland fundraising round cemented its run. $IQE has terrible fundamentals now (Net debt £23.5 million) but is probably one of the most critical parts of the supply chain. If they manage to sell their Taiwan operations, wouldn't be surprised if it went up quite a bit just from their inp business. There's £18m convertible notes (which is basically nothing), then there's 120 to 154m new shares (~12% to 15%), which is also kinda nothing relative to current size. On the other hand, others $LITE and Innolight are probably more established. TLDR: $IQE -> seems critical to Western supply chains, $130MC. Net debt, if they sell Taiwan business -> strong re-rating or they might just dilute you anyway. But if the Taiwan business fails to be sold, probably expect to be diluted to oblivion like Wolfspeed. So huge, huge, risk ad do you own research into risks. But $AXTI and $IQE might are personally interesting to me (I do own $IQE).

English

@theonlywtf How soon now ! Lots of volatility would like to have your hindsight! Thanks and hope you passed all exams

English

@aleabitoreddit Can oracle pull the same thing with tomorrow earning ?

English

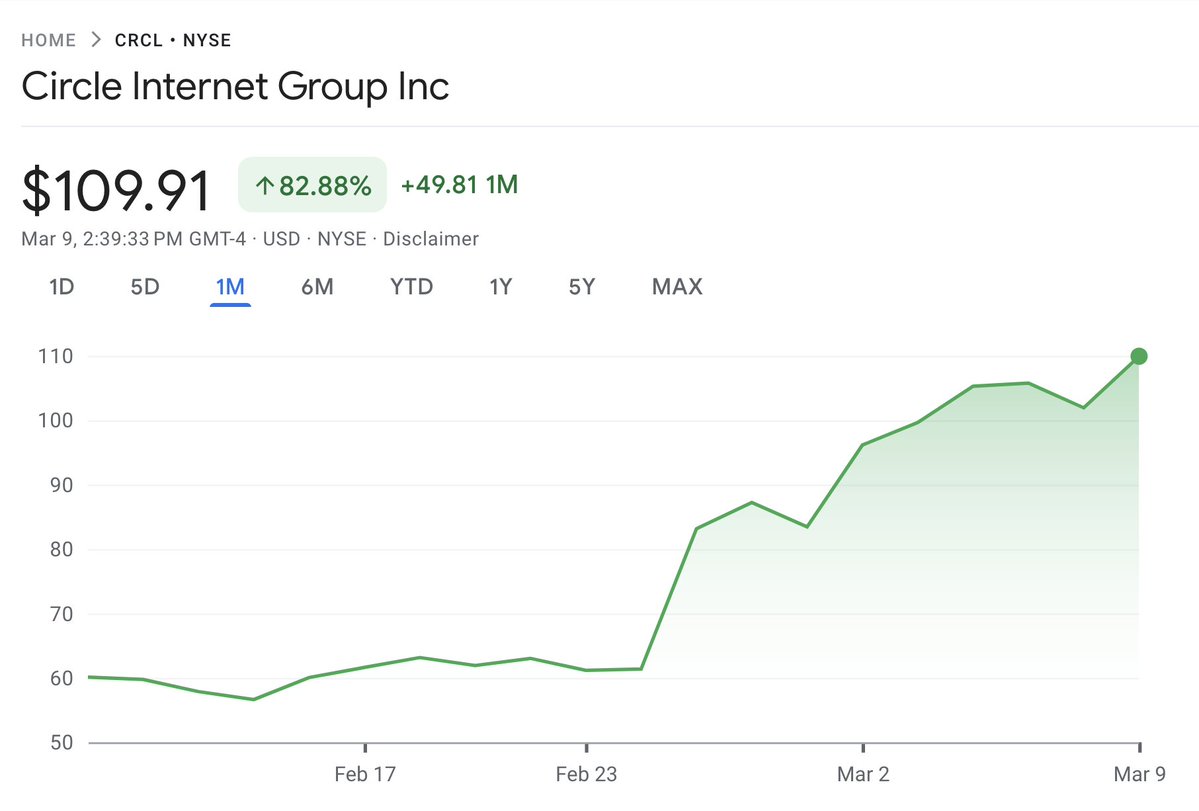

$CRCL is now at $109.

Circle has increased more than 100% to $109... Since my post at $54.

This was 1 month ago.

I really love going back and seeing all the bearish comments claiming it would

"Go down"50%" or "chart looks ugly" so it ends up at $20.

Everyone on X was bearish on $CRCL at $50, but now that it's back at $100, people are bullish again.

The market is the final arbiter of right and wrong.

But the biggest lesson: Look at underlying fundamentals, not the chart.

Serenity@aleabitoreddit

I really, really like $CRCL at $54. Valuation has been completely reset back to $12B MC. Everyone was rushing to buy it back at $150-200 but at $54, it's a ghost town. USDC supply still $70B+ and I expect stablecoins to continue growing in usage.

English

I honestly can’t stop thinking about how much $HIMS and $DUOL are going to win in the next 5 years.

English

@AustinTobitt Wow not a big position for so many great analysis your are doing ! Love your work

English

I've been combing through corporate job openings at #GameStop to figure out how they are positioning themselves. Some of these positions are no longer open, as they have been filled or cancelled. Regardless, the JDs give a lot of info that I found useful.

The TLDR; is that GameStop isn't just building a new eCommerce platform: they're overhauling ALL of their platforms as they move into a new eCommerce business model. I don't think they intend to do all of this work just to sell used video games, trading cards, and Funko pops. I think GameStop is building a completely new type of exchange for token-based transactions or to compete with other eCommerce giants. What they will acquire is still up for grabs, but these are the building blocks for that expansion:

1. Legacy System Enhancements

GME is hiring several engineers and technical SMEs to overhaul legacy applications which place the customer at the center of everything. All of the legacy systems used by in-store associates are being completely redesigned and overhauled, as well as their HRIS (UKG Pro) platform for all matters related to Human Resources.

2. Expansion of platforms into eCommerce

They're hiring SEVERAL engineers and lead developers to create a new (yes, new) platform for customers to engage in eCommerce. There are several JDs that use consistent language such as "experience in payments, transactions, and customer rewards" and "experience with dynamic pricing engines with multiple pricing sources". To me, this indicates some sort of market-based exchange that updates in real-time by browsing competitor prices, like that of Amazon. It could also imply a customer-driven exchange where customers determine the prices. Think "EBay".

Maybe it's just me (because I really want this), but I can also see applications for a digital game exchange like I discussed a weeks ago where you purchase games from a publisher (GTA 6) and subsequently resell them to 2nd hand buyers. Again.. long shot.. But it would be really cool.

They're even hiring a SAP SD Retail Systems Engineer for the sole purpose of analyzing customer transactions and centralizing them within a Customer Activity Repository (CAR) data platform. The data within the CAR is then transformed for multiple consuming applications, including SAP FICO. Another engineer is being hired to do just this for financial reporting purposes.

Oh, and that crappy mobile app? yeah, it's being overhauled as well. There's a position open for Senior Manager, eCommerce & Mobile Engineering just for this purpose. The app will align with this new eCommerce framework and allow customers to quickly do.... whatever they're going to do?

3. Regulatory Adherence

There are several positions open for GRC (governance, risk, compliance) and other roles related to regulatory compliance. The goal is to make sure these new systems (built around consumer data) adhere to consumer privacy rights as they expand this new eCommerce platform.

With that being said, this model can be used for several purposes. I can see a case for purchasing $PYPL (or majority stake) which provides the transactional framework to buy and sell on this new type of eCommerce platform. I can also see the benefit of using this framework in a way that allows for a token-based exchange (like I discussed weeks ago).

There are limitless possibilities and I'm here for it.

💎🙌🚀

English

@michaeljburry @96Jldi GameStop today or a few years ago or both ! Thanks and really enjoying reading you

English

@96Jldi Avanti. Gamestop. Samsung Electronics at book value every time. Short Amazon 2000. Buy stocks in October 2028. I literally pounded the table in front of some investors on Nvidia in 2015 Shoulda held. Feel like I'm forgetting one.

English

If waving the American flag or chanting “USA!” turns you off right now, you're not alone. huffpost.com/entry/theres-a…

English

@182Maxime @WhiteHouse Geez, must be a Canadien…I’ll take that as a compliment seeing as how I’ve never had plastic surgery!

English

@sonofmanWar @WhiteHouse You need more cosmetic surgery you are one ugly guy wow

English

let me know what you think and what you'd like me to share on this channel

think would be fun to do a video on my best and worst investments

English

Launching a YouTube channel to share business stories, lessons I've learned, and important topics I’m actively exploring…

youtu.be/0-LAT4HjWPo

YouTube

English

@Mr_Derivatives @kevinxu Kevin stole his community with a shitcoin he pumped . His app is now dying lol

English

@kevinxu Oh Kevin.

I actually think Mike Alfred is more of a worthy adversary than you. I at least respect the guy.

But hey, more than happy to have a nice chat in DM’s on how we can help each other instead of shitposting time and time again.

Your call. Or not.

English

bros down $4k and begging to god already lmao

Heisenberg@Mr_Derivatives

Dear stock market Gods, Please let me breakeven from my $HIMS $24 position. I promise to pet every dog that walks by me and give them one of those expensive Whole Foods treats from my fanny pack. Because, you know, happy dog happy society. I promise I promise I promise. Please. #breakeven

English

@arny_trezzi @colin_gladman You are too Arny if you are honest with yourself . You are clout chasing

English