Aditya Kumar

19 posts

In money management, performance matters more than philosophy.

1] PPFAS became popular because of performance, not just philosophy. If performance slips, investors move fast.

2] Marcellus PMS gained AUM through strong marketing, but weak performance didn't sustain it.

3] Quantum Mutual Fund has a solid philosophy, but returns lagged, so AUM stayed small.

4] Quant Mutual Fund delivered strong returns from 2020-2024 and attracted big inflows. Now facing pressure.

5] Motilal Oswal saw strong performance in 2024-2025 and gained AUM. Now slowing.

Performance drives flows. Flows drive AUM.

English

𝗙𝗿𝗲𝗲 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝟭 𝗛𝗼𝘂𝗿 !

Ask any stock market query

Kindly 1 person - 1 query : )

Ask below 👇

English

Aditya Kumar がリツイート

@LokNiwasDelhi @LtGovDelhi @SandhuTaranjitS @ZakirHtabla Hon’ble LG Sir,@SandhuTaranjitS

The result for Post Assistant Teacher Nursery 817/23still pending @dsssbofficial

I also request transparency in the process

#DSSSB_Transparency

#DSSSB_Result_Delay

@dsssbofficial @gupta_rekha @SandhuTaranjitS @LtGovDelhi @LokNiwasDelhi

English

Aditya Kumar がリツイート

Aditya Kumar がリツイート

Aditya Kumar がリツイート

#KVS

Offline Exam

Advt Nov 2025

Exam Jan 2026

Result 28 Feb 2026

Meanwhile DSSSB 👇

Five year Plan

Online Exam

TGT Advt 2024

Exam Aug–Sep 2025

❌ Result: God's know

❌ No raw marks

❌ No response sheet

❌ No transparency

@LtGovDelhi @SandhuTaranjitS @dsssbofficial

English

Suzlon has been weak lately, so I’m sharing a few thoughts on why that might be and also why, at these levels, the risk-reward looks genuinely interesting.

The broader market has been soft and many stocks are down from their 52-week highs, so Suzlon isn’t unique. What intrigues me is that after this correction, it feels like downside fears are getting priced faster than the underlying wind demand.

The big fear: “Adani has entered WTG and that’s game over.”

Adani Wind (Adani New Industries) has already commercialized a 5.2 MW onshore platform with 160 m rotor diameter, ~200 m tip height, 91 meter blade. It was built with tech collaboration from W2E (Germany).

It is type certified by WindGuard under the IECRE system, referencing the IEC 61400 standards, which matters for bankability and international acceptance/export readiness.

Adani is also building an integrated manufacturing ecosystem near Mundra, and with the port advantage, exports are likely part of the long-term plan.

That said, Adani talking about ~5 GW WTG manufacturing capacity by 2027 doesn’t automatically “flood” the market. India’s wind demand is not a one-player story.

Government bidding trajectory mandates 50 GW/year RE bids through FY2028, with at least 10 GW/year reserved for wind. Hybrid (solar + wind) is also increasingly preferred because profiles complement each other, smoothing generation, reducing intermittency, lowering battery needs, and improving transmission utilisation. This makes supply more “firm-like” for DISCOMs.

Suzlon management also cited ~6.34 GW installations in 2025 and expects the industry to cross 10 GW annually within ~2 years, driven by bids plus C&I demand.

Also, GWEC estimates India could go from ~51 GW to ~107 GW by 2030, implying roughly ~11 GW/year average additions (path may vary).

So even at 5 GW capacity, Adani alone doesn’t dominate. Plus Adani’s own downstream plan is large (30 GW wind by 2030 within its broader 50 GW renewables push). This means internal absorption will likely be meaningful.

Now Suzlon. Its workhorse is the S144 (3 MW series) with 144 m rotor and ~70 m blade. Management has also said a 5 MW platform is in prototype stage and will come at the appropriate time.

On certifications, type certification is essentially the wind industry’s passport for safety + bankability under the IEC 61400 family. Adani highlights IECRE/WindGuard; Suzlon’s S144 references IEC testing standards (e.g., IEC 61400-12) and operates within the same global certification ecosystem.

What many miss is Suzlon’s export lever. In the Q3 FY26 call, management talked about India emerging as a global sourcing hub and highlighted export opportunities for WTGs and for SE Forge castings. So, Suzlon isn’t only a domestic OEM, it’s also a components/manufacturing base play via SE Forge.

But the point is that wind demand in US is just not there under Mr. Trump while other export markets are also facing uncertainty.

Conclusion: Adani’s entry is real and technically credible. But India’s wind runway is also real (policy + C&I + hybrid/RTC) supports sustained wind additions. In that context, Adani’s 5 GW isn’t enough to saturate the industry, and Suzlon’s correction starts to look like a risk-reward setup worth tracking.

Key risk: the thesis still depends heavily on domestic wind demand/execution. Exports can grow, but India remains the bread-and-butter. If the wind build-out slows materially, the thesis breaks.

Also, Suzlon is diversifying itself into solar & BESS to become full stack, diversified renewable energy service provider. Some management restructuring already took place. This entails its own risks and rewards but more on that some other time when there is good clarity. You can read about it.

Tushar Pandey@equities_samjho

I feel Suzlon Energy is also at a favourable risk-reward ratio. Markets are overreacting on the risks and, therefore, underpricing the business. Will share a detailed take tomorrow.

English

@equities_samjho Can kpi green recover or not sir

Plz suggest ur view on kpi

If possible make a video either suggest ur view on kpi sir

Will they execute botswana project

English

Power EPC players might not again command the valuations that they did 2 years back.

They’re unlikely to go to 50-60-70 PE now.

KEC International seems one of the worst placed, constantly reducing margin guidance.

I’ve said this many times before, EPC players work in a very competitive landscape with a thousand moving risks. One should look at them only when there is immense tailwinds (which there is) and they’re at reasonable valuations (some are now reasonable).

That being said, at current valuations, I think Skipper can be looked at. It’s not a pure play EPC though and that’s not a bug.

Risk reward seems good. I wouldn’t expect crazy returns either. More like safe compounding at these levels.

Transrail can also be looked at. Similar risk reward.

English

@equities_samjho Kpi share holder will get the share of sun drop energia

Please suggest sir what benefits will get by share holder

English

KPI Green Energy plans to spin off Sun Drops Energia sometime in the next fiscal.

Sun Drops will be its BESS play.

For the whole company, they’re still guiding 50-60% growth in the coming years.

KPI has done good so far, at good valuations now. I think the price to mess up execution at this stage for KPI would be huge.

English

Some of the undervalued companies in your radar? Also write why in brief. Will try to cover them if helpful.

English

Answer is not "300"

Tell me the answer and win $1000

English

@kpgroupgujarat Sir jii I have invested my whole saving on kpi green

I waana see my company at 1 Lk Cr

What is the company target to reach at this target

English

Another milestone achieved!

KP Group’s H1FY26 results were announced at KP House, celebrating our collective efforts, performance, and progress toward a greener tomorrow.

Every number reflects the dedication of our people and the trust of our partners.

#KPGroup #H1FY26 #Performance #SustainableGrowth #TeamKP #ResultsAnnouncement

English

Name an underperforming stock in your #portfolio which you believe has immense value ?

English

#CarTrade now expects OLX to grow 15% YoY in Q2. One concern was slowing OLX sales but they seem to be turning it around too, a sign that I was personally looking at.

GST reduction to fuel demand among used cars (& other products) too.

Not sure how other two segments will perform in Q2. Also, if you’re doing press release, why just share one segment’s numbers :)

Anyway, still going good 👍

Tushar Pandey@equities_samjho

Made some good gains (almost 3x) in #CarTrade too. Was very lucky to enter at the right time (following this from its IPO aftermath). Booked some profits in the last few days. Will trail the rest. High base & slowing top line were the main reason. I can be wrong but this approach works for me so I’ll stick to it.

English

✅KPI Green Energy Receives charging approval for 76.22 MW solar and wind-solar hybrid power projects under CPP segment.

#KPIGREEN

English

Aditya Kumar がリツイート

हेलो राज ठाकरे।

क्या जावेद अख़्तर मराठी बोलता है।

क्या शाहरुख़ ख़ान मराठी बोलता है।

क्या सलमान ख़ान मराठी बोलता है।

क्या आमिर ख़ान मराठी बोलता है।

लेकिन राज ठाकरे के गुंडों को ग़रीब हिंदुओ को मारना है बस।

हिन्दी

Aditya Kumar がリツイート

Take a look at the Namalpur no. 1 Solar Site!

📍 Location: Namalpur no. 1

🏢 Site Owner: Varsha Dyeing & Printing Mills Pvt Ltd., Vineet Polyfab Pvt Ltd.

⚡ Capacity: 5.6 MW

Harnessing the power of the sun to drive sustainability and clean energy solutions. Stay tuned for more updates on our solar projects. This is a KP Group CPP site, contributing to KP Group's total renewable energy portfolio of 5.75+ GW, with 77+ solar, wind and hybrid sites across India.

A step towards our ambitious target of 10 GW by 2030.

#KPEnergy #SolarPower #RenewableEnergy #Sustainability #SolarProjects #CleanEnergy #GreenFuture

English

@equities_samjho Sir ji plz make a informative video regarding kp green engineering ltd

No informative video available

I see a potential in this share ( M I wrong or not)

English

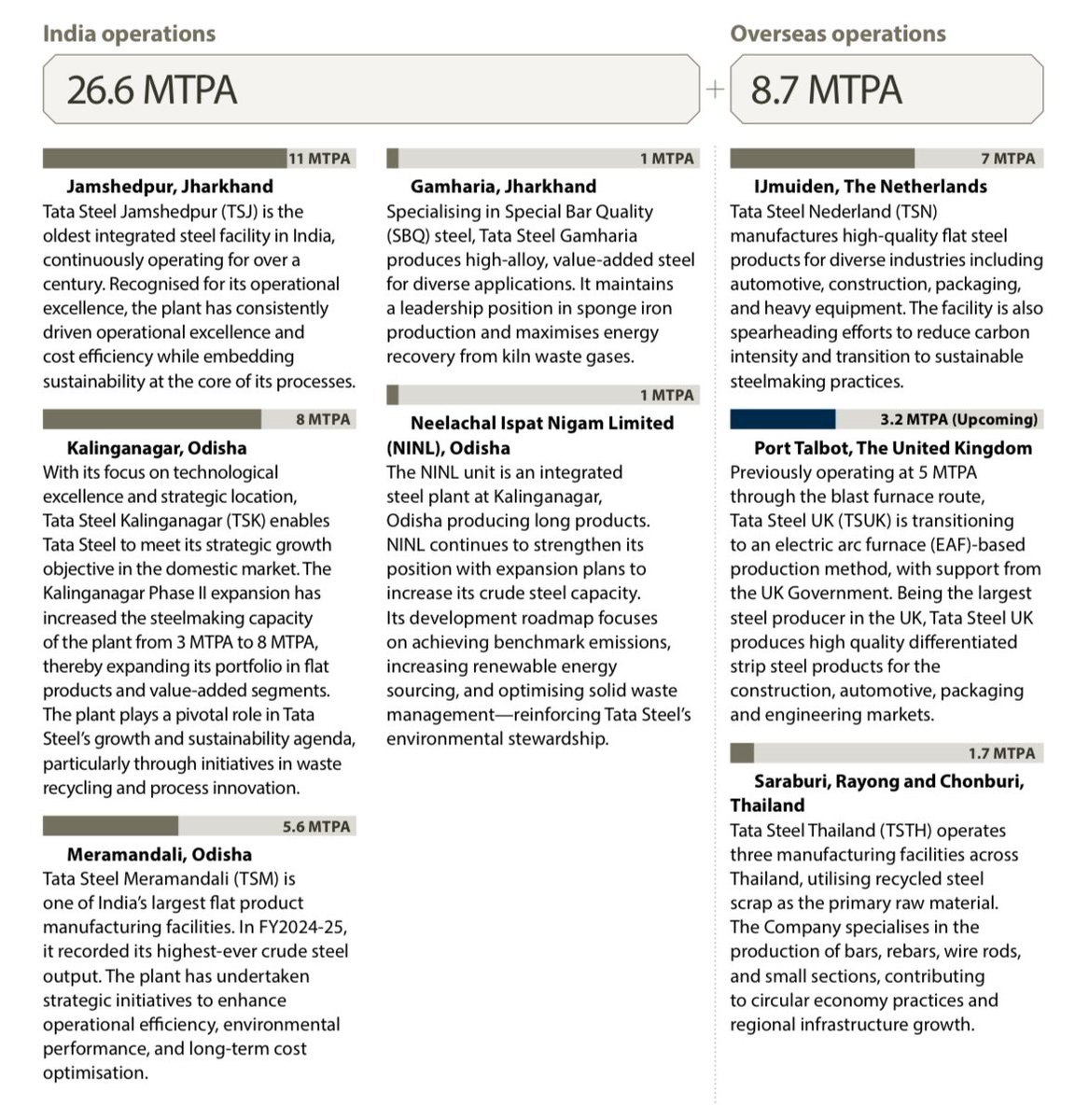

All Tata Steel Facilities & their respective downstream products

Tata Steel is cutting costs significantly so that they become sustainable at lesser EBITDA/ton

They reduced costs by 6,600 cr in FY25 & plan to reduce further by 11,500 cr in FY26

English